Buying a home in California while working in public service can feel like a math problem that never balances. You know your income is steady. You know homeownership matters for your family and your future. But between down payment requirements, closing costs, and home prices that move fast, it's easy to assume you need far more cash than is needed.

That assumption keeps a lot of qualified buyers on the sidelines.

Teachers, firefighters, police officers, city staff, county employees, state workers, and federal employees often have access to loan structures and assistance programs that the average buyer never asks about. The key is understanding that government employee home loans usually aren't one special mortgage with one simple label. In practice, they're a combination of the right base loan, the right assistance layer, and the right lender strategy for California.

Your Path to Homeownership in Public Service

A California public employee can do a lot right and still feel priced out. The paycheck is steady. The debt load is reasonable. The problem usually shows up at the same point. Coming up with enough cash for the down payment, closing costs, and reserves without wiping out savings.

That is the actual starting point.

Government employee home loans are usually most useful when they reduce that upfront strain and make the purchase sustainable after closing. In California, that matters more than in many other states because even buyers with solid income can get squeezed by high prices, fast-moving listings, and out-of-pocket costs that stack up quickly.

Public service income often helps on the approval side. A documented salary history, stable employment, and predictable pay structure are all positives in underwriting. The bigger opportunity, though, is strategic. Many teachers, firefighters, police officers, county workers, state employees, city staff, and federal employees can pair a standard mortgage with assistance that lowers the cash needed at closing.

That changes the question. The goal is not to find a single branded “government employee loan.” The goal is to build the right structure for your situation in California, based on your job, credit, savings, monthly budget, and target price range.

I tell clients to start there because the trade-offs are real. A lower-down-payment option can preserve cash, but it may come with mortgage insurance or a higher monthly payment. Assistance can help you buy sooner, but some programs have income limits, location rules, or repayment terms that need a careful review. The right answer depends on whether your biggest constraint is cash to close, monthly payment, credit profile, or all three.

A practical approach is simple. Choose the base loan that fits. Add assistance only if it improves the outcome. Keep enough money in reserve so the home still feels affordable after the keys are in your hand.

That is how public servants buy successfully in California. Not by chasing one special product, but by using a California-specific plan that combines the right financing and the right assistance in the right order.

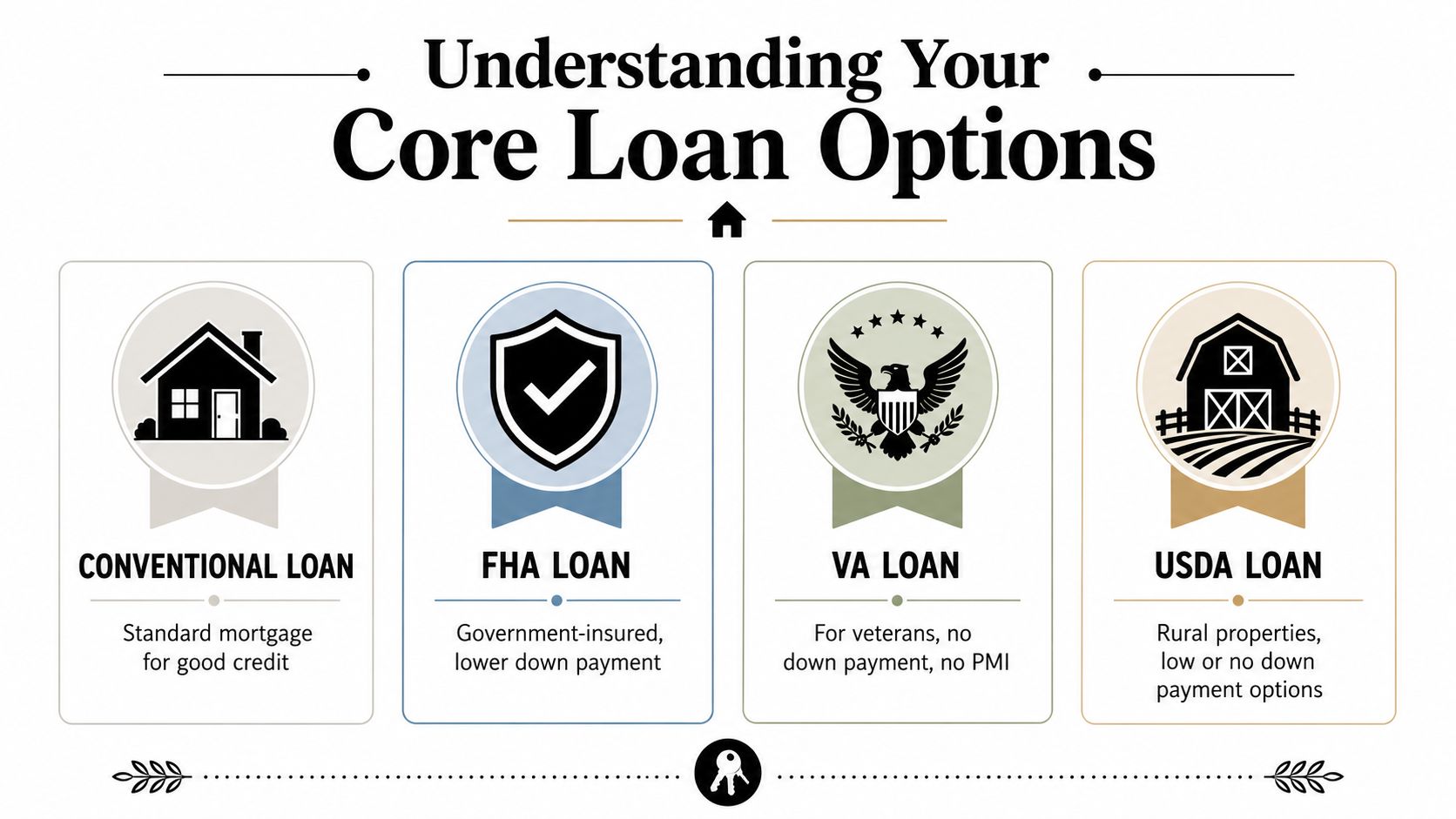

Understanding Your Core Loan Options

A school counselor in Sacramento, a firefighter in Riverside, and a county analyst in San Diego can all ask for a "government employee home loan" and end up needing three very different mortgage structures. The job title may help with stability in underwriting. The base loan still drives the rate, mortgage insurance, cash to close, and how much flexibility you have later.

In California, that choice carries more weight because home prices magnify every financing decision. A slightly higher payment, a mortgage insurance premium that lasts longer, or a larger cash requirement at closing can change what is realistic in your target county.

Conventional loans

Conventional financing is often the strongest fit for public employees with solid credit, stable income, and enough savings to cover down payment, closing costs, and reserves. It usually gives borrowers more room on property type and fewer program-specific restrictions than government-backed options.

The main advantage is long-term cost control. If the credit profile is strong, conventional pricing can be competitive, and private mortgage insurance may be removable later. That matters for California buyers who plan to stay put and want the payment to improve over time.

The trade-off is straightforward. Conventional loans tend to be less forgiving when credit, debt ratios, or available cash are tight.

FHA loans

FHA is often the entry point for first-time buyers in public service, especially when savings are limited or credit has a few rough edges. It allows a lower down payment than many buyers expect and can approve borrowers who would struggle to qualify conventionally.

That flexibility comes at a cost. FHA includes mortgage insurance, and in many cases that cost lasts much longer than borrowers realize. I often recommend FHA when it solves a real access problem now, not because it looks familiar on a rate sheet.

For buyers who need help with upfront funds, FHA can also pair well with certain California down payment assistance options for public servants, if the program guidelines line up.

VA and USDA loans

VA and USDA are niche programs, but for the right borrower they can be the strongest option on the board.

- VA loans deserve a close look for eligible veterans, active-duty service members, and some surviving spouses working in public service. The biggest advantage is often the ability to buy with no down payment and no monthly mortgage insurance.

- USDA loans can work for buyers purchasing in eligible rural areas. In California, that usually means looking beyond the highest-cost urban cores and checking address eligibility carefully.

- Overlap matters. A city employee may also have VA eligibility. A teacher commuting from an outlying area may find a USDA-eligible property. The best loan is the one that fits both the borrower and the address.

How to compare the base loan the right way

Start with the question the loan needs to solve. Is the pressure point cash to close, monthly payment, credit flexibility, or eligibility for a specific property?

| Loan type | Often fits best when | Main consideration |

|---|---|---|

| Conventional | Credit, income, and savings are relatively strong | Often attractive for long-term cost and future flexibility |

| FHA | Lower down payment and more flexible underwriting matter most | Mortgage insurance can raise total housing cost |

| VA | Buyer has eligible military status | Funding fee, entitlement, and occupancy rules need review |

| USDA | Buyer and property meet program rules | Location and income limits drive eligibility |

The most common mistake is choosing a loan based on the headline feature alone. Zero down, low down, or easier approval can all sound right at first. In practice, the best result usually comes from comparing total monthly cost, cash needed at closing, and how the loan will hold up if you refinance, move, or keep the property for years.

Unlocking Grants and Down Payment Assistance

The phrase “government employee home loans” can be misleading because it sounds like one packaged product. Most of the time, it isn't. What helps buyers is layered financing. That means a first mortgage does the heavy lifting, then grants, credits, or subordinate assistance reduce what you need to bring in cash.

That structure matters in California because the upfront hurdle is often more painful than the monthly payment.

How the stack works

A public employee might use an FHA, VA, USDA, or conventional first mortgage and then add separate assistance if a program allows it. Public Servant Next Door is one example of that model. It states that eligible federal, state, county, and city employees may access grants up to $9,000 and down payment assistance up to $24,000, depending on income, location, and available funds, through its government employee mortgage program page.

The idea is simple. Your first mortgage buys the home. The assistance lowers the amount of cash you need to complete the purchase.

What works well and what needs caution

Some assistance is structured to help without immediately increasing the monthly payment. Other forms of help come with second liens, deferred repayment, occupancy rules, or conditions triggered by sale or refinance.

That doesn't make assistance bad. It means you should read it as a financing tool, not free money by default.

A disciplined review should answer these questions:

- Repayment terms: Is the assistance a grant, a deferred loan, or another lien that must be repaid later?

- Occupancy rules: Must you live in the property as your primary residence for a set period?

- Refinance impact: Will refinancing trigger repayment or reduce flexibility later?

- Cash preservation: Does the assistance meaningfully protect your reserves after closing?

If you're comparing options in California, it helps to review available down payment assistance programs for hero buyers alongside your first-mortgage choices. The right stack can reduce stress at closing. The wrong stack can make a transaction look affordable upfront while constraining your next move.

The real goal

The goal isn't to collect the most assistance. The goal is to build the most durable purchase. For some buyers, that means layering every eligible benefit. For others, it means using less assistance so they keep more flexibility later.

California Government Employee Home Loan Programs

A county employee in Sacramento and a school administrator in Orange County can both qualify for strong financing, yet the right structure may look very different for each one. California prices, local assistance rules, condo standards, and seller expectations change the decision fast. That is why a national list of programs rarely gives public servants enough to act on.

California buyers need a plan that fits this market.

Why local guidance matters in California

In this state, loan selection affects more than the interest rate. It affects how much cash you need to keep in reserve, how clean your offer looks to a seller, and whether your file can close on schedule once underwriting starts.

I regularly see buyers focus on a program headline and miss the practical pressure points. Some options add extra approval steps. Some limit the types of properties that work. Some pair well with California assistance programs, while others create conflicts that show up late in escrow.

What to look for in a California-specific program

The strongest California government employee home loan programs usually solve a specific problem. They may reduce the cash needed at closing, improve the monthly payment, or give the borrower more room to compete in a tight market. A good fit does not need to do everything. It needs to improve the parts of the transaction that matter most for that buyer.

Here is what I check first:

- Cash-to-close impact. Lower upfront cash can help, but only if the added financing does not create strain after closing.

- Offer strength. Programs that require extra layers of review can weaken a purchase offer in a fast-moving market.

- Compatibility with California assistance. The first mortgage and the assistance piece need to work together cleanly.

- Property fit. Condo rules, occupancy standards, and local underwriting overlays can eliminate an otherwise appealing option.

- Profession-specific eligibility. Public servants should confirm whether their role fits a targeted program before building the rest of the strategy. Buyers can review California home loan options for government and public service employees to see how profession-based support is typically structured.

The California approach that tends to work

The most effective files are built in sequence, not assembled from scattered benefits.

Start with the base loan. Then test whether any assistance improves the transaction or just makes it more complicated. Review the property early, especially if the target is a condo or a home in a market where sellers expect quick closings. After that, run the numbers with real taxes, insurance, and reserve expectations, not just an online payment estimate.

A program can look attractive on paper and still be the wrong choice if it weakens the offer or limits refinance flexibility later.

That is the California difference. Public servants here usually do better with a coordinated loan strategy than with a generic checklist of national programs.

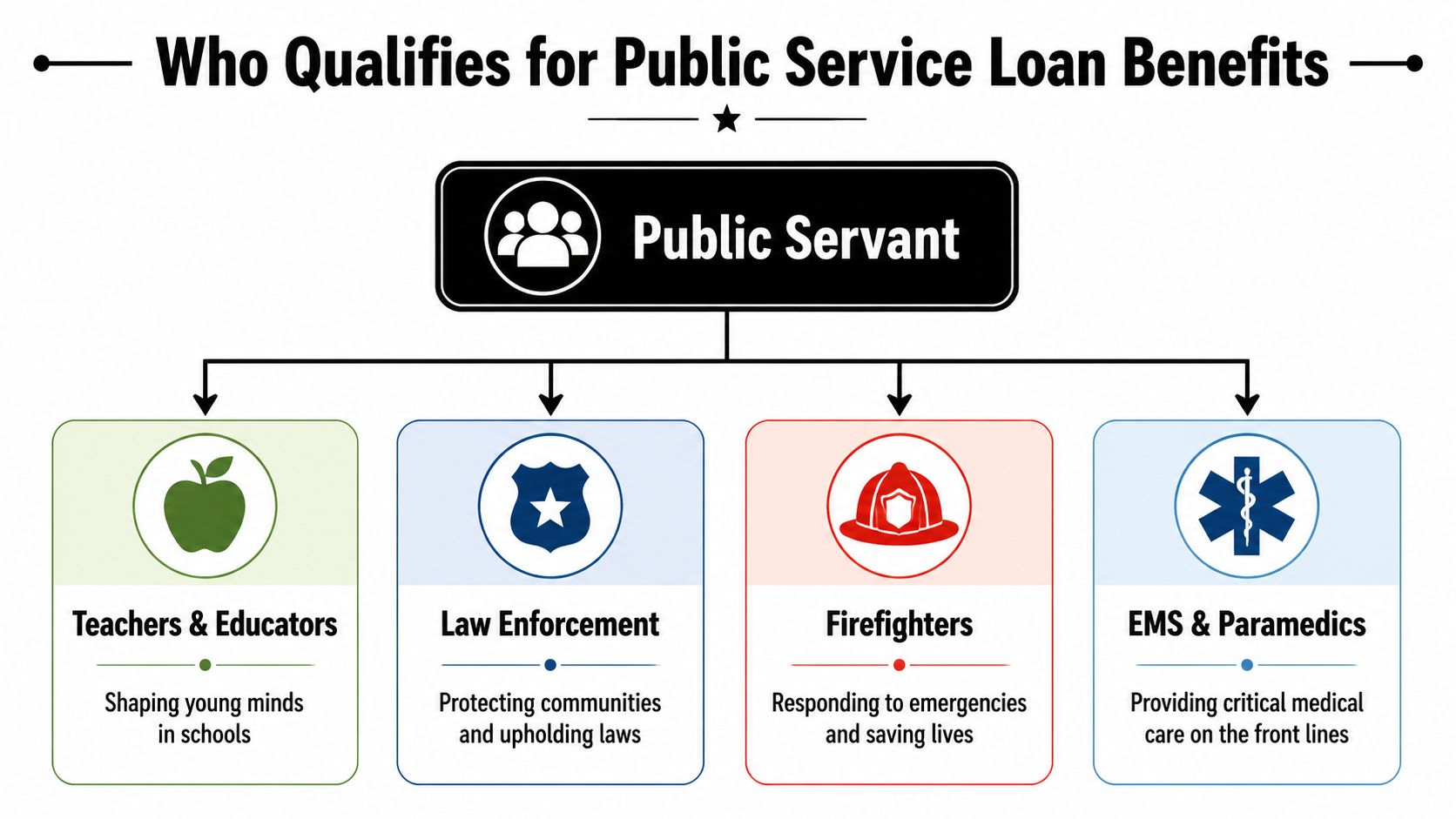

Who Qualifies for Public Service Loan Benefits

Eligibility is broader than many buyers expect. Government employee home loans can apply to more than one narrow job title, but every program defines its own boundaries. Some focus on direct government employment. Others include public-facing professions such as educators, law enforcement, firefighters, EMS staff, and healthcare workers.

The roles that commonly qualify

The most common eligible groups include:

- Federal employees

- State employees

- County and city employees

- Teachers and school staff

- Law enforcement personnel

- Firefighters and EMS professionals

- Public service workers in qualifying agencies or departments

For California buyers who want a profession-specific reference point, public service employee home loan information for hero professions can help narrow where to start.

The common threads lenders and programs check

Eligibility usually depends on more than your job title. Programs often look at a combination of employment status, occupancy intent, and borrower profile.

A lender or assistance administrator may ask for:

| Eligibility factor | Why it matters |

|---|---|

| Current employment | Confirms you're actively working in a qualifying role |

| Primary residence intent | Many benefits are for owner-occupied homes, not rentals |

| Income position | Some assistance programs cap income or target moderate-income buyers |

| First-time buyer status | Certain benefits are limited to first-time homebuyers |

| Location | Program rules can change by city, county, or property area |

Why public-sector employment is viewed favorably

There's a long history of stable homeownership among federal workers. According to the National Association of Realtors, nearly two-thirds of federal employees own their homes, with ownership rates reaching 75% to 90% in counties near government hubs, based on NAR's analysis of federal employee homeownership.

That doesn't mean every public employee automatically qualifies. It does show that public-sector work has long aligned with stable borrowing capacity and sustained homeownership.

The practical takeaway is simple. If you work in public service, don't assume you're outside the box because your title doesn't sound specialized enough. Ask how the program defines your role, then verify the employment and occupancy rules before you shop.

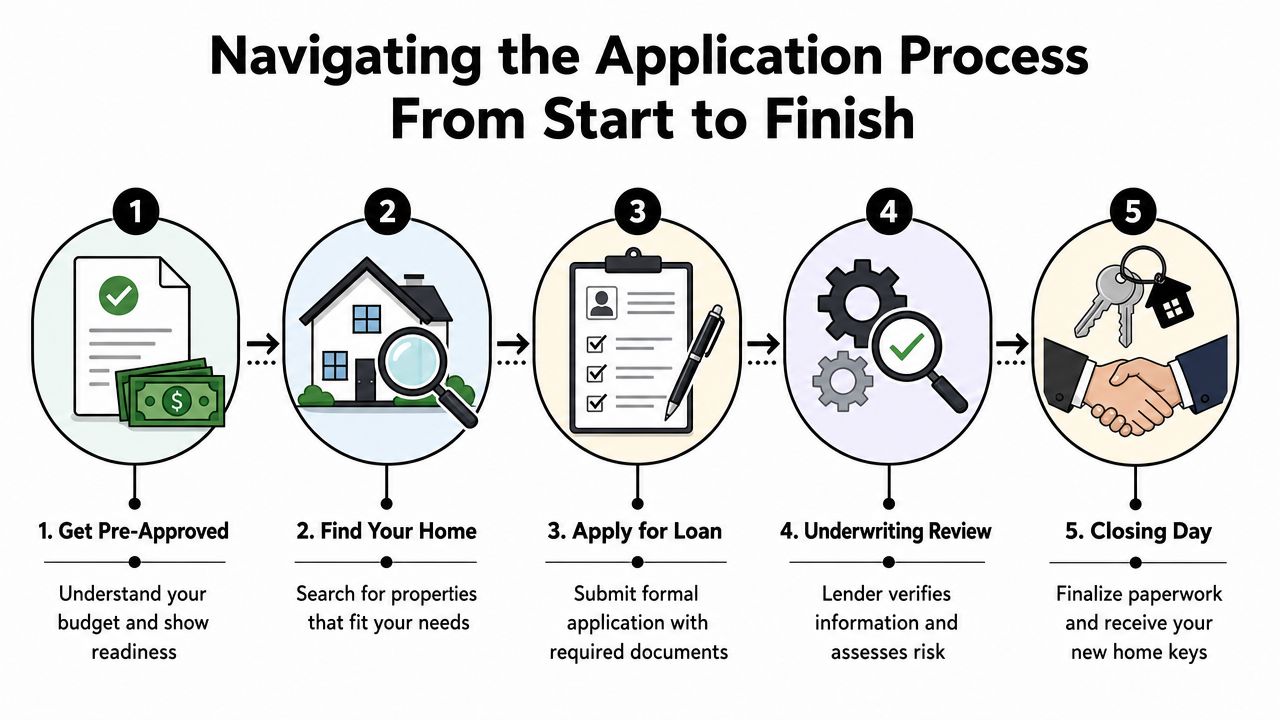

Navigating the Application Process From Start to Finish

Most buyers don't struggle because they're unqualified. They struggle because the process gets messy once the loan, the assistance program, and the purchase contract all start moving at once.

A clean file solves a lot of problems before underwriting ever sees it.

Step one through step three

Start with pre-approval, not home tours. That gives you a budget range grounded in your actual income, debts, and available cash. It also tells you whether your best first move is FHA, conventional, VA, USDA, or a layered structure.

Then gather documents early. Most public employees should expect to provide pay stubs, W-2s, identification, bank statements, and proof of current employment. If assistance is involved, there may be extra forms tied to education, eligibility, occupancy, or program-specific approvals.

If you're buying your first place, a practical prep guide like these steps to buying your first home can help you organize the moving pieces before you're under contract.

Why layered financing needs extra care

Assistance often adds paperwork, timing requirements, and approval checkpoints. Maryland's House Keys 4 Employees program is a clear example of how layered financing works. It provides a $2,500 zero-percent deferred loan on top of an existing $6,000 benefit, lowering cash-to-close without increasing the monthly payment, according to Maryland Mortgage Program details for employee down payment assistance.

That's a Maryland example, not a California rule. But it shows the kind of structure borrowers can run into. One transaction can involve a first mortgage, a separate assistance lien, and multiple sets of disclosures and program conditions.

Underwriting insight: The more layers in the file, the more important it is to verify timelines, signatures, and program compatibility before escrow gets tight.

Step four and step five

Once you're in underwriting, the lender verifies income, assets, employment, and property details. If something changes during this period, tell your loan officer immediately. New debt, unexplained deposits, job changes, or missing paperwork can create avoidable delays.

Before closing, review these items carefully:

- Cash to close: Make sure final figures match the assistance and credits you expected.

- Occupancy certifications: Many public-service benefits require owner occupancy.

- Repayment triggers: Know whether refinancing or selling later could affect assistance.

The buyers who move through this well usually do one thing consistently. They respond fast and keep their file boring. In mortgage lending, boring is good.

Frequently Asked Questions About Hero Loans

Is using assistance always the smartest move

No. Assistance can reduce the upfront cash burden, which is often the biggest barrier in California. But that doesn't automatically make it the lowest-cost option over the life of the mortgage.

Some program materials note that for government employees with stronger credit, a conventional loan may offer a lower long-term cost, even when assistance looks appealing upfront, as explained on this guide to home loans for government employees. That's the right question to ask before you commit. Not just “How much do I save at closing?” but “What does this structure cost me over time?”

What happens if I leave my public service job after closing

That depends on the program documents, not the marketing summary. Some benefits are tied mainly to your status at application and closing. Others may include ongoing occupancy or repayment conditions that become relevant if you move, sell, or refinance.

The safe approach is to ask for the exact rule in writing. If a benefit is structured as a grant, deferred loan, or second lien, you need to know what events trigger repayment.

Can I use these programs for an investment property

Usually, the focus is primary residence financing. Public-service benefits and assistance are commonly tied to owner occupancy because their purpose is expanding access to homeownership, not subsidizing investment purchases.

If your plan is to buy a rental or a second home, say that early. A loan officer can tell you whether the program is incompatible before you waste time building the wrong file.

What's the biggest mistake public employees make

They chase the biggest advertised benefit instead of the best total structure.

A large assistance figure can be useful. It can also distract from a weaker base loan, a slower closing path, or conditions that reduce flexibility later. The stronger move is to compare full outcomes: cash to close, monthly payment, long-term cost, and future options.

How should I prepare before talking to a lender

Bring three things mentally organized before anything else:

- Your employment picture: who you work for, how you're paid, and whether your role qualifies under any public-service category

- Your cash picture: how much you want to keep in reserves after closing

- Your property picture: where in California you want to buy and whether it will be your primary residence

Those answers usually shape the strategy faster than a generic online prequalification tool ever will.

If you're a California public servant trying to make sense of government employee home loans, California Loans for Heroes is one place to review profession-based options, lender credits, and assistance pathways built for eligible hero buyers across the state.