Closing costs in California typically land around 2% to 5% of the home's purchase price or loan amount, so on a $300,000 home, that can mean roughly $6,000 to $15,000 due at closing, separate from your down payment. If you're buying in California for the first time, that extra cash requirement can feel like the part nobody fully explained until you were already deep into the process.

A lot of buyers get to the Loan Estimate stage and have the same reaction. The monthly payment makes sense, the down payment is already stressful enough, and then a second bucket of money shows up with line items that sound technical, legal, and expensive.

That's normal.

As a California loan professional, I can tell you this is one of the most common points of confusion for first-time buyers, especially teachers, nurses, firefighters, veterans, law enforcement, and other public service professionals trying to plan carefully and avoid surprises. The good news is that closing costs aren't random. Once you understand what they are, who charges them, and which parts can sometimes be negotiated, the whole process gets much easier to manage.

Understanding Closing Costs in Simple Terms

When you buy a home, closing costs are the collection of fees required to complete the mortgage and transfer ownership properly. They're separate from your down payment. Your down payment builds equity. Closing costs pay for the work, documentation, verification, and setup required to get the loan funded and the property officially transferred to you.

A simple way to think about it is buying a car. The sticker price isn't the only number you pay. There are registration fees, taxes, documentation charges, and related costs that come with finalizing the purchase. A home works the same way, just with more moving parts and more people involved.

In major U.S. mortgage markets, buyers typically pay about 2% to 5% of the purchase price or loan amount in closing costs, according to Zillow's closing costs guide. That same guide notes that a $300,000 home can create about $6,000 to $15,000 in cash due at closing, separate from the down payment.

The three buckets most buyers see

Most closing costs fit into three broad categories:

- Lender fees. These are charges tied directly to your mortgage company's work. That can include origination-related costs, underwriting-related charges, and any lender-specific processing items.

- Third-party service fees. These go to other companies involved in the transaction, such as the appraiser, title company, escrow company, or recording office.

- Prepaids and escrow setup. These aren't always “fees” in the usual sense. Some of this money is collected upfront to start your property tax and homeowners insurance payments or to cover interest due before your first full mortgage payment.

Why buyers get tripped up

The confusion usually comes from one simple fact. Not every dollar at closing is the same kind of dollar.

Some charges pay for a service. Some are deposits. Some are tied to your loan. Some are tied to the property. Some may change a bit before closing, while others are more stable.

Practical rule: If a line item looks confusing, first ask which bucket it belongs to. Lender fee, third-party fee, or prepaid item. That one question usually makes the rest of the explanation much clearer.

What matters most at the start

You do not need to memorize every fee name on day one. You just need to know what you're looking at and why it exists.

That alone changes the experience. Instead of seeing a page full of mystery charges, you start seeing a checklist of services and deposits tied to a real purchase.

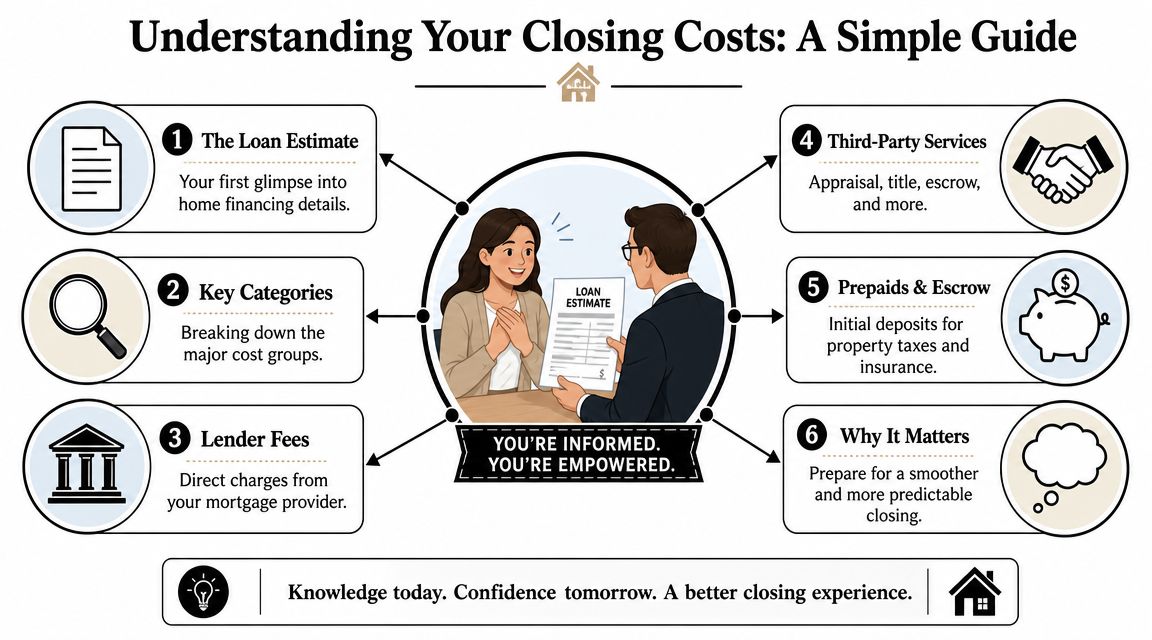

A Detailed Line-by-Line Breakdown of Common Costs

Buyers usually want a true closing costs breakdown, not just a definition. They want to know what those line items mean when they show up on a Loan Estimate.

The easiest way to read them is by category, not by document order. That helps you figure out which costs come from the lender, which come from outside vendors, and which ones are collected upfront for future bills.

Lender fees

These are the charges connected to creating and approving your mortgage.

Origination-related charges are what many buyers notice first. This is the lender's compensation for structuring and processing the loan. If you're comparing lenders, this is one area worth reviewing carefully because fee structures can differ.

Discount points, if offered and chosen, are different. They're not automatic. A buyer may decide to pay points to get a lower interest rate, but that tradeoff only makes sense in certain situations.

Underwriting, processing, or application-style fees may appear as separate items or be grouped differently depending on the lender. The wording can vary, which is why comparing one lender's worksheet to another isn't always apples to apples unless someone walks you through it.

Third-party fees

These are charges for outside services required to move the transaction forward.

Here are the ones buyers most often see:

- Appraisal fee. This pays for an independent opinion of the property's value so the lender can confirm the home supports the loan.

- Credit report fee. This covers the lender pulling your credit information.

- Title search and title-related fees. These help confirm legal ownership and identify any recorded issues tied to the property.

- Escrow or settlement fees. These cover the neutral party handling documents, money movement, and final coordination.

- Recording and government fees. These are tied to filing documents with the appropriate local office.

- Inspection-related costs. Some inspections are outside the formal lender closing worksheet, but they still affect your total cash needed during the transaction.

An Urban Institute analysis found that for mortgages between $400,000 and $500,000, lender title fees, title insurance, transfer taxes, and origination fees alone account for 57% of average closing costs, excluding prepaids, according to the Urban Institute's review of closing cost components. That's a helpful reminder that a few major items often drive a large share of the total.

When buyers feel overwhelmed, I usually suggest this shortcut: find the title-related charges, transfer-related charges, and origination-related charges first. Those often explain a big portion of the total.

Prepaids and escrow items

This category often surprises first-time buyers because these charges don't always feel like “fees.”

They may include prepaid interest, homeowners insurance collected upfront, and property tax funds set aside in escrow. The lender may collect these amounts at closing so future bills can be paid when due.

That matters because a buyer might look at the final cash-to-close number and assume every dollar is a transaction charge. It isn't. Some of that money is being collected in advance for homeownership expenses that were coming anyway.

Who usually pays each kind of item

California customs vary by area, lender, and contract terms, but this general reference helps:

| Cost type | Usually tied to | Often paid by |

|---|---|---|

| Origination-related charges | Loan setup | Buyer |

| Appraisal | Loan approval | Buyer |

| Credit report | Loan approval | Buyer |

| Escrow or settlement charges | Transaction handling | Can vary |

| Title-related items | Ownership and lien review | Can vary |

| Prepaid taxes and insurance | Future housing expenses | Buyer |

The key is not assuming a fee is fixed just because it appears on a form. Some items are standard. Some are negotiable. Some depend on local custom. Some can be offset through credits.

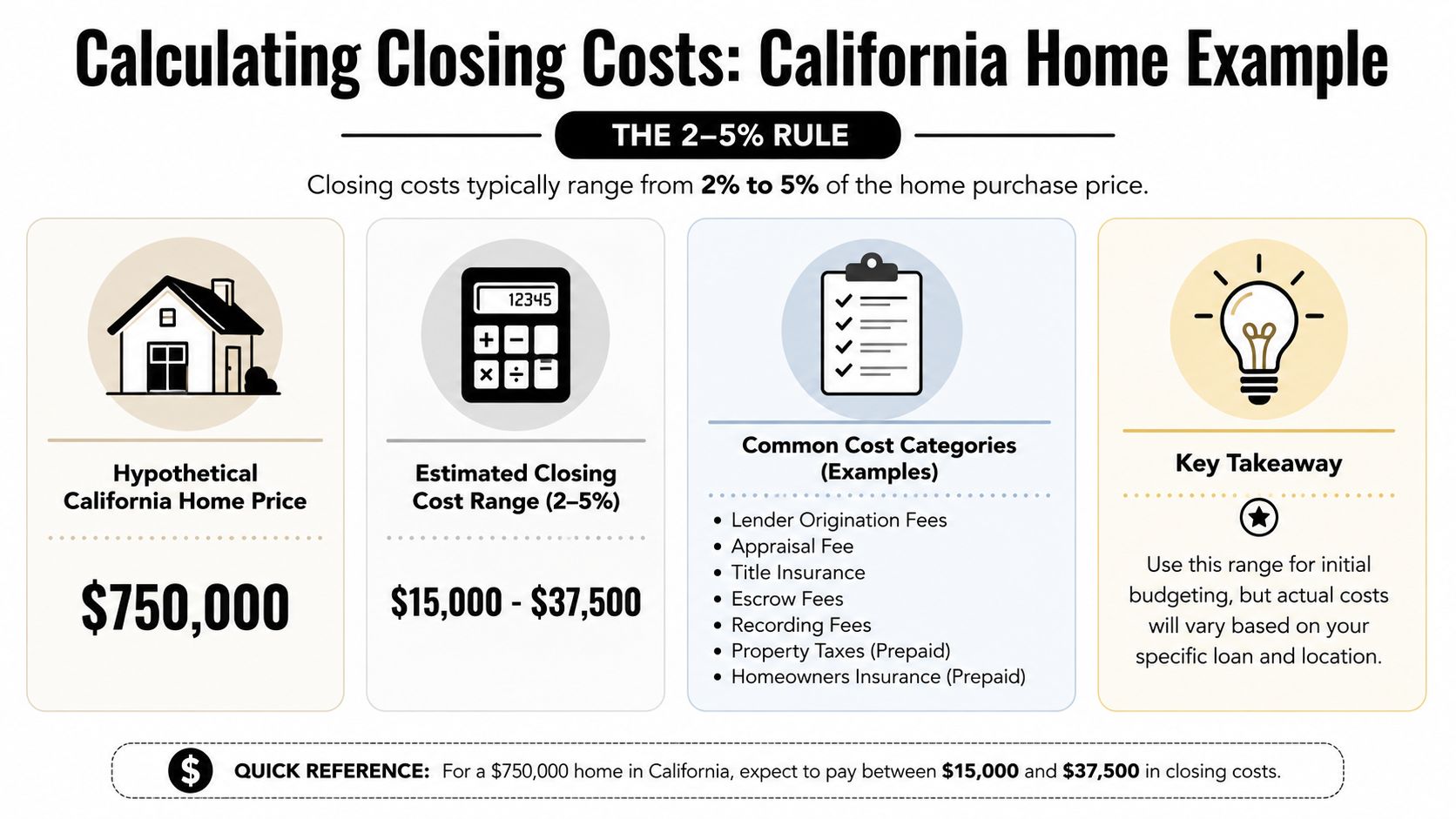

How to Calculate Your Estimated Closing Costs in California

If you want a practical way to estimate your numbers before your final paperwork arrives, start with a simple budgeting rule.

Take the home price or loan amount and apply a 2% to 5% range for your early estimate. That won't replace an official Loan Estimate, but it gives you a realistic planning range so you're not caught off guard.

A California home example

Let's use a $750,000 California home purchase.

- 2% estimate: $15,000

- 5% estimate: $37,500

That gives you an early closing cost budget range of $15,000 to $37,500.

That range is broad on purpose. Actual costs can shift based on location, loan structure, title and escrow charges, prepaid items, and whether any seller or lender credits reduce your out-of-pocket amount.

The two documents that matter most

Two mortgage documents help you track this process clearly.

Loan Estimate

This is your early quote. After you apply, your lender provides a Loan Estimate that outlines projected loan terms, monthly payment, and estimated closing costs. Think of it as the first serious map of the transaction.

Closing Disclosure

This is the final version. It shows the numbers you're expected to pay at closing based on the near-final terms of the transaction.

For many first-time buyers, the stress comes from treating these documents like legal forms that shouldn't be questioned. That's the wrong mindset. These are working documents. You're supposed to read them closely.

How to use them without getting overwhelmed

Use this simple review process:

- Start with the total cash to close so you know the bottom-line amount.

- Scan for lender charges first because those are often easiest to compare.

- Check title, escrow, and recording items next.

- Separate out prepaid items so you understand what's a fee versus what's a future expense collected upfront.

- Ask about any new or unfamiliar line item before signing.

A good lender won't rush you through these numbers. If something looks unfamiliar, ask for a plain-English explanation until it makes sense.

That's especially important in California, where buyers often already feel stretched by home prices. A careful review helps you protect your budget and avoid last-minute surprises.

Who Pays for What Buyer vs Seller Responsibilities

One of the biggest misunderstandings in a California purchase is assuming every closing cost belongs to the buyer. That's not how real transactions work.

Some costs are commonly paid by the buyer because they're tied directly to the buyer's loan. Other costs may fall on the seller, or they may be split depending on local custom and the purchase contract.

What the buyer commonly pays

In many transactions, the buyer often covers items such as:

- Loan-related charges tied to the mortgage application, approval, and funding

- Appraisal and credit-related items required by the lender

- Prepaid homeowners insurance, property tax reserves, and interest collected at closing

- Home inspection and other buyer-elected inspections, when those are ordered separately during the transaction

These are usually viewed as buyer responsibilities because they connect directly to the buyer's financing or decision-making.

What the seller often handles

Sellers commonly take responsibility for expenses tied more directly to selling the property, local transfer practices, or negotiated contract terms. Depending on the area and agreement, this can include certain title-related charges, transfer-related charges, or negotiated credits to the buyer.

Why California custom matters

California isn't one-size-fits-all. County practices and local market habits can influence who typically pays specific items. The contract always matters more than general advice.

That's why two buyers can purchase homes in different parts of California and see a different split of costs even if the home prices are similar.

Local custom matters, but contract terms rule. If your purchase agreement says a cost is paid a certain way, that written agreement is what controls the transaction.

Seller credits can change the picture

A seller credit or seller concession is when the seller agrees to cover some of the buyer's closing costs as part of the negotiation. That can be especially helpful if a buyer has enough income to support the mortgage but wants to preserve more cash for moving, repairs, reserves, or day-one home expenses.

In a softer market, credits can become a useful negotiating tool. In a highly competitive market, they may be harder to get. Either way, they're worth discussing with your real estate agent and lender early, not after the numbers are already finalized.

Actionable Strategies to Lower Your Closing Costs

Most buyers can't erase closing costs. They can often reduce the burden with the right strategy.

The key is being active early. Closing costs reward buyers who ask questions, compare offers, and negotiate before the file reaches the final signing stage.

Shop lenders by total cost, not just rate

A low interest rate can look great in a headline quote while the lender fees tell a different story. When you compare lenders, review the full estimated cost picture, especially origination-related charges and lender credits.

Ask each lender to explain the tradeoff between rate and upfront cost in plain terms. That's how you learn whether you're saving money or moving costs from one column to another.

Negotiate for seller credits

If the market and the property support it, ask whether the seller can contribute toward your closing costs. This won't always be possible, but when it is, it can ease the amount of cash you need to bring in.

This is especially useful for first-time buyers trying to keep some savings in reserve after closing.

Ask about lender credits

A lender credit can reduce your out-of-pocket costs at closing. The tradeoff is often a higher interest rate. That doesn't automatically make it a bad deal. It depends on your goals.

If keeping more cash on hand matters more than securing the lowest possible rate, a lender credit may be worth exploring.

Consider timing and prepaids

Closing later in the month can sometimes reduce the amount of prepaid interest collected at closing. It won't transform the whole transaction, but it can make a difference around the edges.

You should also ask which items are true fees and which are prepaid housing expenses. Buyers sometimes think they need to “cut” a number that is only being collected in advance for taxes or insurance.

Use assistance programs strategically

Assistance can make the biggest difference when it's paired with smart planning. If you qualify for buyer support, down payment help, or specialized programs for community professionals, you may be able to free up cash for closing instead of draining every dollar into the down payment.

You can review one option through the California Loans for Heroes buyer assistance program.

A strong plan often combines several moves at once: compare lenders, ask about credits, negotiate contract terms, and preserve your own cash wherever possible.

How California Loans for Heroes Helps You Save

For many California buyers, the problem isn't just qualifying for a mortgage. It's getting all the way to the closing table with enough cash left for closing costs, reserves, moving expenses, and the realities of settling into a new home.

That pressure can be even more noticeable for the people who keep California running. Teachers, nurses, firefighters, EMS professionals, law enforcement, military families, veterans, pilots, and public service employees often have solid income and stable careers, but that doesn't mean they want to empty their savings just to cross the finish line.

Support built around real cash-to-close pressure

California Loans for Heroes is built around a practical reality. Many homebuyers don't need more jargon. They need real options that can reduce upfront strain.

That can include access to lender credits, guidance on available assistance paths, and one-on-one support from professionals who understand how to structure a purchase so the buyer's cash position stays manageable.

For a first-time buyer, that matters because closing costs rarely show up as one simple charge. They come in layers. When a program helps offset some of that burden, the buyer may have more flexibility to handle escrow deposits, prepaid items, and the rest of the closing process without feeling squeezed.

Why this matters for California hero professions

Hero professions often serve their communities on demanding schedules. They don't always have time to decode every mortgage detail on their own, and they shouldn't have to.

Programs designed for these buyers can help by:

- Reducing upfront strain through lender-credit opportunities when available

- Improving planning so buyers understand cash to close before the final rush

- Connecting buyers with assistance options that may complement their financing strategy

- Creating a more guided process for professions that already carry high day-to-day responsibility

That's especially important for buyers trying to balance homeownership goals with family obligations, commuting realities, and career demands.

A more workable path for veterans and service professionals

Some buyers also need options that align with military or veteran homeownership goals. California Loans for Heroes offers information specifically geared toward that need through its closing cost assistance for veterans.

The right mortgage strategy isn't just about approval. It's about getting the keys without putting yourself in a financial bind the very first month you own the home.

For buyers in hero professions, that kind of support can turn homeownership from “maybe later” into something more realistic now.

Your Borrower Checklist for a Smooth Closing

A smooth closing usually comes down to preparation, not luck. Buyers who stay organized, ask questions early, and review documents carefully tend to feel much more confident by signing day.

Use this checklist as your final pass before closing.

The essentials to handle before signing

- Review your Loan Estimate carefully and make sure you understand the major categories of charges.

- Compare your Closing Disclosure to earlier numbers so you can spot changes and ask about them.

- Confirm your exact cash-to-close amount with your lender and escrow team before moving money.

- Keep closing funds separate so you're not scrambling at the last minute.

- Secure homeowners insurance early because your lender will need proof before closing.

- Finish your final walk-through and confirm the property condition matches the agreement.

- Ask for plain-English answers to any fee or document you don't understand.

Habits that help first-time buyers most

A few simple habits make a real difference:

- Stay responsive when your lender asks for documents

- Avoid major financial changes during the loan process

- Save every updated estimate and disclosure in one place

- Loop in your agent and loan officer quickly if something feels off

- Use a trusted homebuying roadmap, such as these steps to buying your first home

The goal isn't to become an expert in mortgage paperwork overnight. It's to stay informed enough that nothing on closing day feels mysterious.

If you're prepared, a closing costs breakdown stops being scary. It becomes a set of numbers you understand, verify, and handle with confidence.

If you're a California veteran, teacher, nurse, firefighter, law enforcement professional, pilot, or public service employee, California Loans for Heroes can help you explore home loan options designed to make buying a home more manageable. Their team understands the cash-to-close challenges California buyers face and offers guidance on lender credits, assistance options, and personalized support so you can move forward with more clarity and less stress.