You've found a house in California, your VA eligibility is solid, and then the lender sends over an estimate with closing costs that feel a lot bigger than expected. That's a common moment. Many veteran buyers assume “VA means zero out of pocket,” then realize zero down payment and zero cash to close are not the same thing.

The good news is that closing cost assistance for veterans is real, and in California, it often works best when you treat it like a stack instead of a single benefit. The VA loan gives you the base layer. State and local programs may add another layer. A bank grant, nonprofit program, gift funds, or a lender credit can close the remaining gap if the file is structured correctly.

I work with VA buyers in California, and the difference between a smooth low-cash closing and a stressful one usually comes down to timing, documentation, and negotiation strategy. Buyers who wait until escrow to ask about assistance usually have fewer options. Buyers who build the stack before they write an offer usually have more room to reduce cash-to-close.

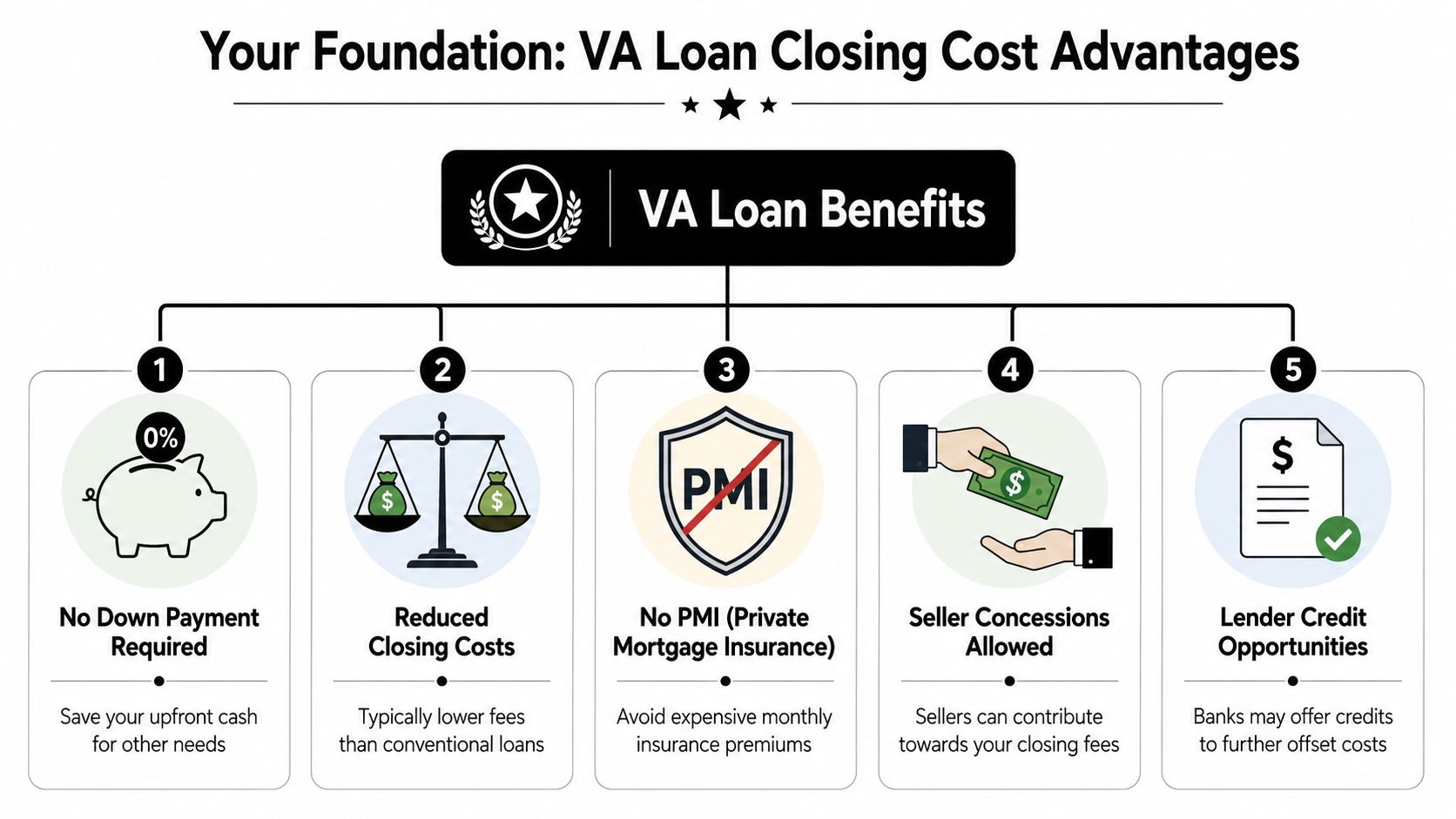

Your Foundation VA Loan Closing Cost Advantages

Most California veterans start in the right place without realizing it. The first source of closing cost assistance for veterans is the VA loan itself. Before you look at grants or local programs, you need to understand the protections and cost advantages already built into VA financing.

That matters because a lot of buyers focus only on down payment. In practice, closing costs, prepaid taxes, insurance, and the funding fee are what create the cash hurdle.

Start with the built-in VA protections

The VA doesn't eliminate all closing costs, but it does limit how expensive the loan structure can become. According to the VA funding fee and closing cost rules published by the U.S. Department of Veterans Affairs, sellers or builders may provide credits toward closing costs, and those credits are not capped the same way as seller concessions. The same VA guidance says seller concessions are limited to no more than 4% of the home's reasonable value, and the funding fee is 2.15% for first-use borrowers with less than 5% down and 3.3% for subsequent users with less than 5% down.

That distinction matters in negotiations. Many agents and buyers treat “seller paid costs” as one bucket. On a VA deal, that's not always how the file is analyzed.

Here are the practical advantages that usually matter most:

- No down payment requirement for many eligible buyers: That preserves cash for settlement charges instead of tying it up in equity on day one.

- Controlled lender fee structure: VA rules limit how lenders can structure certain charges, which helps reduce fee creep.

- Seller participation: A seller may help with approved costs, which can materially reduce what you bring to closing.

- Builder credits can help too: On new construction, builder-paid incentives may create a useful path if the contract is written correctly.

Practical rule: Don't ask, “Can the seller help?” Ask, “Which costs can the seller cover on this VA file, and which bucket does each item fall into?”

What works in California and what doesn't

In California, the market still drives how much room you have to negotiate. If a property has multiple offers, broad seller concessions can be harder to win. If the property has been sitting, or the seller is motivated, asking for cost help becomes more realistic.

What usually works:

- Comparing lender fee structures early: Don't assume every VA lender prices the same way.

- Reviewing the Loan Estimate line by line: You're looking for the avoidable costs, not just the total.

- Keeping offer strategy tied to market conditions: A strong offer with targeted requests often performs better than asking for every possible concession.

What usually doesn't work:

- Treating the VA loan as fully self-executing: It isn't. A VA loan can be affordable, but the deal still needs active structuring.

- Waiting until final disclosures to question fees: By then, your ability to negotiate is reduced.

- Ignoring lender credits: In some cases, a credit is the cleanest way to reduce cash due at closing.

If you're still at the shopping stage, a good next step is reviewing your options for California home loans for veterans and military buyers. The right loan structure often determines how much assistance you can successfully layer later.

Why this foundation matters before you chase grants

Some buyers spend weeks searching for outside assistance when they haven't cleaned up the base loan first. That's backwards. If the lender fees are too high, the seller concession request is vague, or the funding fee strategy isn't clear, a grant won't fix a poorly built transaction.

A clean VA structure gives you the platform to stack additional help. Without that foundation, you're just adding paperwork to a file that may still leave you short at closing.

California-Specific Veteran Homebuyer Programs

National VA benefits are only part of the picture. In California, veteran buyers should also look at state, county, and city-level assistance, because that's often where meaningful closing cost help shows up.

Some of these programs are widely advertised. Others are buried on housing agency sites, city program pages, or lender partner lists. The buyers who save the most usually cast a wider net than just “VA loan plus seller credit.”

Where California veterans should look first

California buyers should think in tiers:

| Search tier | What to check | Why it matters |

|---|---|---|

| State programs | Veteran-friendly or public housing assistance programs | These may offer broader availability |

| County programs | Local housing finance agencies | Rules often depend on property location |

| City programs | Municipal first-time buyer assistance | Some programs are highly localized |

| Approved lender channels | Lender-accessed assistance options | Availability can depend on who originates the loan |

The key is not assuming that a program labeled “first-time buyer” excludes veterans. Some do. Some don't. Some allow repeat buyers if they haven't owned recently or if they meet another exception. You have to read the actual eligibility rules and then confirm that the lender can use the assistance with a VA-backed transaction.

The trade-off most buyers miss

Program money can be significant, but availability is never the whole story. The structure matters just as much as the amount. Some assistance is a grant. Some is a forgivable second. Some requires repayment when you sell or refinance. Some works only in certain ZIP codes or for homes under program rules.

According to the overview of veteran homebuyer assistance programs published by VA Loan Network, some state programs offer grants covering up to 2% of the purchase price with no repayment. The same source notes that many programs are stackable with VA financing, but often have income limits or purchase-location restrictions, and that documentation failure is a common reason deals run into trouble.

That's the part buyers often underestimate. They focus on approval and forget compliance.

The money is only useful if the lender, program administrator, and escrow timeline all line up before contingencies start expiring.

How to find the hyper-local programs

A California veteran should usually search in this order:

- Property location first: Start with the city and county where you plan to buy.

- Program rules second: Check occupancy, income, and first-time-buyer requirements.

- Lender compatibility third: Make sure the assistance can be paired with a VA loan.

- Reservation timing last: Some programs require approval or funds reservation before contract acceptance, while others can be layered after.

A practical mistake I see is buyers shopping all over California while trying to lock down local assistance at the same time. That makes the process harder. If the program is county-based, your target area needs to be narrow enough to screen eligibility accurately.

For broader homeownership support options designed for public service buyers in the state, review California home loan help for heroes and veterans. The value isn't just in finding a program. It's in finding one that survives underwriting.

Securing Grants from Banks and Veteran Nonprofits

Government programs get most of the attention, but private assistance can be just as important. When veterans ask me where overlooked closing cost help exists, I usually point them toward bank-connected grant channels and veteran-focused nonprofit programs.

These funds often come with two catches. First, they may only be available through participating institutions. Second, they don't stay open forever.

Bank-channel grants versus nonprofit assistance

The simplest way to think about private assistance is by distribution channel.

Bank-channel programs usually require the mortgage to go through an approved lender or member institution. That means the grant might be excellent, but inaccessible if your lender isn't connected to the program.

Nonprofit and mission-driven programs may be more flexible in intent, but they still tend to have narrow documentation standards. Military status, occupancy requirements, and timing still matter. So does the exact use of funds.

Here's the practical split:

- Bank-routed grant funds: Strong option when you already know the lender can deliver the program.

- Veteran nonprofit support: Useful when the organization focuses on military families, disability-related needs, or hardship relief.

- Targeted family categories: Some of the strongest benefits are reserved for narrower groups, not the entire veteran market.

Why disabled veterans and Gold Star families should look separately

This is one of the most under-covered areas in veteran mortgage guidance. Not all assistance is meant for all veterans. Some of the more meaningful aid is reserved for borrowers with a service-related disability or for Gold Star Families.

The FHLB Dallas HAVEN program page states that the program provides up to $25,000 for eligible veterans, service members with a service-related disability, and Gold Star Families for down payment and/or closing costs. The same page notes that funds are available only through member institutions and end when funds are exhausted or on December 31, 2026, whichever comes first.

That combination of rules changes how you plan:

- Eligibility isn't broad: You need to fit the program category exactly.

- Access depends on lender channel: If the institution isn't a participating member, the program may be irrelevant to your file.

- Timing matters: A strong program with depleted funds is no program at all.

Limited-fund assistance should be treated like inventory. Check access first, then build the loan around it if it fits.

What usually goes wrong

Most failures happen before underwriting ever reviews the grant. The borrower or agent hears about a program late, assumes it can be dropped into escrow, and then learns the lender can't use it, the funds are gone, or the documentation doesn't match the property and borrower profile.

The solution is simple, even if the execution takes work. Verify the grant source, verify the lender channel, and verify the deadline before you rely on the money in your cash-to-close plan.

Your Application Roadmap and Document Checklist

Veterans lose assistance money in boring ways. Missing statements. Unclear gift documentation. Program approval started too late. Property location checked after the offer instead of before it.

A workable roadmap keeps that from happening.

The order that keeps files moving

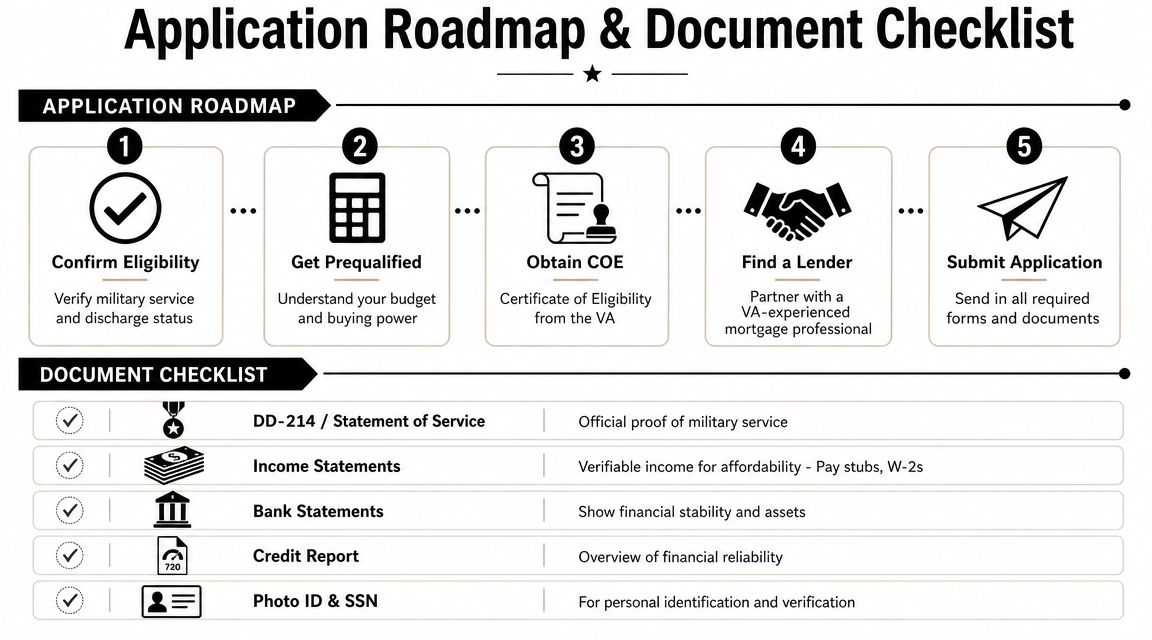

Start with eligibility, but don't stop there. The file needs to be built in the same order underwriters and assistance administrators will review it.

Confirm VA eligibility

Get your Certificate of Eligibility lined up as early as possible. If there's any service record issue, deal with it before shopping seriously.Get prequalified with a VA-experienced lender

This tells you whether the deal is limited by payment, cash-to-close, or both. Those are different problems.Screen assistance before writing offers

If the program has location restrictions, income limits, or a required approval path, you need that answer before you're in contract.Collect documents for all funding sources

The base mortgage file and the assistance file often overlap, but they are not always identical.Keep every party on the same timeline

Lender, escrow, agent, and program administrator need the same closing target and the same source-of-funds story.

The documents that matter most

Many buyers think the challenge is finding closing cost assistance for veterans. Often, the harder part is proving the funds are acceptable to all parties in the transaction.

Build your file with these items ready:

- Military eligibility records: COE, DD-214, or statement of service if needed.

- Income documentation: Pay stubs, W-2s, and any other income records the lender requests.

- Asset statements: Recent bank statements for reserves, earnest money, and sourcing.

- Identification documents: Government-issued ID and Social Security verification.

- Assistance paperwork: Grant approval letters, reservation documents, and program disclosures.

- Gift documentation if applicable: Signed gift letter and evidence of the donor's funds when required.

A strong checklist doesn't just help you get approved. It also helps you avoid last-minute conditions that can delay escrow.

Why early prep gives you more options

The broader assistance market is larger than many buyers realize. The Down Payment Resource summary on veteran assistance programs reports 61 programs specifically developed for veterans, service members, and surviving spouses, with assistance ranging from $2,000 to $120,000. That same source says 74% of first-time VA loan users put 0% down.

Those figures are useful, but they don't mean every buyer can access every program. In practice, the borrowers who benefit are the ones who organize first and shop second.

Checklist mindset: If the money has rules, treat it like underwriting from day one.

Stacking Your Benefits with The HERO Loan Advantage

Most real savings happen not from one giant grant or a single generous seller, but from combining smaller and larger pieces in the right order.

For VA buyers, the most effective approach is usually to build a stack that reduces cash-to-close from multiple directions at once. One source handles part of the closing costs. Another offsets prepaids. Another fills the remaining gap.

What a strong stack looks like

A useful stack often includes some combination of these:

| Layer | Role in the transaction |

|---|---|

| VA loan structure | Reduces the upfront burden compared with many other loan types |

| Seller contributions | Helps cover allowed costs when negotiated well |

| Lender credit | Can offset fees in exchange for rate pricing trade-offs |

| Grant or DPA funds | Covers residual closing costs or prepaids |

| Gift funds | Fills remaining gaps when program rules allow |

The key isn't using every source. The key is using the right sources without violating program compatibility rules.

The Neighbors Bank explanation of VA closing costs notes that the most effective way to reduce cash-to-close is by stacking benefits. That same guide states that VA rules allow sellers to contribute up to 4% of the loan amount for concessions, and that this cap is separate from other seller-paid costs. It also describes a high-probability savings path as combining lender credits with seller concessions and then using grant funds to cover remaining items like the VA funding fee or prepaids.

Where California buyers make mistakes

In California, buyers usually miss on stacking for one of three reasons:

- They treat all seller help as one category: On VA files, category matters.

- They chase the biggest advertised grant first: The best fit is often the program that your lender can close with.

- They ignore pricing trade-offs on lender credits: A credit can help preserve cash, but it needs to be weighed against the long-term payment.

That last point is especially important. Lender credits are not free money. They're a pricing decision. Sometimes that decision makes sense. Sometimes it doesn't.

How the HERO angle fits the stack

For California buyers who want an additional lender-side option, the California Loans for Heroes buyer assistance program is one example of a program built around homebuyer assistance and lender-credit style support for eligible hero groups, including military and veterans. In a stacking strategy, that type of option can serve as the final layer when the base VA structure, seller participation, and any grant funds still leave a residual amount due at closing.

That's the practical use case. Not replacing the VA loan. Not replacing state or local aid. Filling the gap.

The strongest VA transactions are usually engineered, not discovered. Someone has to line up the concessions, the credit strategy, and the assistance timing before the file gets tight.

Frequently Asked Questions on Veteran Closing Cost Help

Can closing cost assistance for veterans be used for anything besides settlement charges

Sometimes yes, sometimes no. It depends on the program rules and the lender's approval. Some assistance can be applied toward closing costs and prepaid items. Other programs are narrower and only allow specific uses. Before relying on funds for taxes, insurance, or the funding fee, ask for the written use-of-funds rules and make sure the lender signs off on that structure.

What happens if my purchase contract falls through after I'm approved for assistance

It depends on how the program reserves funds. Some approvals follow the borrower for a period of time. Others are tied to the property, the contract, or the closing timeline. If the deal dies, the money may need to be re-reserved, re-approved, or it may be lost if funds are limited. That's why it's smart to ask two questions early: “Is the approval borrower-based or property-based?” and “What happens to the reservation if escrow cancels?”

Can I use assistance to improve my approval odds by paying off debt

Usually, assistance for veteran homebuyers is intended for down payment, closing costs, or approved prepaids, not general debt reduction. If debt is the main issue in your file, that has to be addressed separately through your qualification strategy. A buyer who is payment-constrained needs a different plan than a buyer who qualifies easily but doesn't want to bring much cash to closing.

Is gift money treated the same as grant money

No. Underwriting and documentation are usually different. Gift funds normally require a gift letter and source-of-funds documentation, while grants often require their own approval package and compatibility review. Both can help, but they move through the file differently.

Should I wait until I find a house to ask about assistance

No. That's one of the most expensive mistakes buyers make. Assistance works better when it's screened before you write an offer. If a program has location limits, income caps, or lender participation rules, you want those answers before the negotiation starts.

If you're buying in California and want help sorting out which combinations of VA benefits, grants, seller concessions, and lender credits may work on your file, California Loans for Heroes can help you review the options and structure a realistic cash-to-close plan before you go under contract.