You finished school. You survived training. You've got the license, the job offer, or the schedule that barely leaves room to breathe. And now you're trying to buy a home in California while carrying student debt that makes a standard mortgage application look worse than your actual financial future.

That's where most generic mortgage advice falls apart.

A conventional lender often sees debt, short employment history, and limited cash reserves. A mortgage advisor who works specifically with healthcare borrowers sees something else: a high-skill professional with strong income potential, a defined career path, and financing options built for exactly that profile. If you're searching for a home loan for medical professional borrowers in California, you need guidance that matches California prices, California timelines, and California underwriting pressure.

Your Path to Homeownership as a California Healthcare Hero

A lot of California healthcare buyers come to me at the same point. They're working long shifts, paying rent that feels absurd, and wondering if buying a home is even realistic yet. The answer is often yes, but not with the loan advice they've been getting.

A nurse in Orange County, a pharmacist in Sacramento, a resident relocating to Los Angeles, and a new attending in San Diego don't all fit into the same financing box. That's the mistake most articles make. They talk about “doctor loans” in broad terms and stop there, without answering the specific issue.

What matters in California is whether the program works at your price point, with your contract timing, in your county, and under your reserve requirements. Regions puts that problem plainly in its physicians and emerging professional mortgage overview. That's the right question to ask.

Why California changes the conversation

In lower-cost markets, a specialized medical mortgage can be a nice perk.

In California, it can be the difference between buying now and sitting out the market longer than you want to. High prices expose every weak point in a standard mortgage approval. Appraised value matters more. Cash to close matters more. Reserve rules matter more. Timing your purchase around a new contract matters more.

That's also why healthcare workers beyond physicians need a real seat at the table. Programs for nurses and healthcare professionals in California exist because this isn't only a physician issue. It's a healthcare workforce issue.

Buying in California isn't just about qualifying on paper. It's about matching the right loan structure to a very expensive market before the wrong one wastes your time.

Who this is really for

If any of this sounds familiar, this guide is for you:

- Early-career buyers: You've got a signed contract, but not months of pay stubs.

- High-debt, high-income-potential professionals: Your student loans are real, but so is your earning trajectory.

- Healthcare workers outside the usual doctor-loan stereotype: Nurses, pharmacists, dentists, physician assistants, and other licensed professionals often get overlooked.

- Buyers targeting expensive areas: You need a loan that still makes sense once California prices enter the conversation.

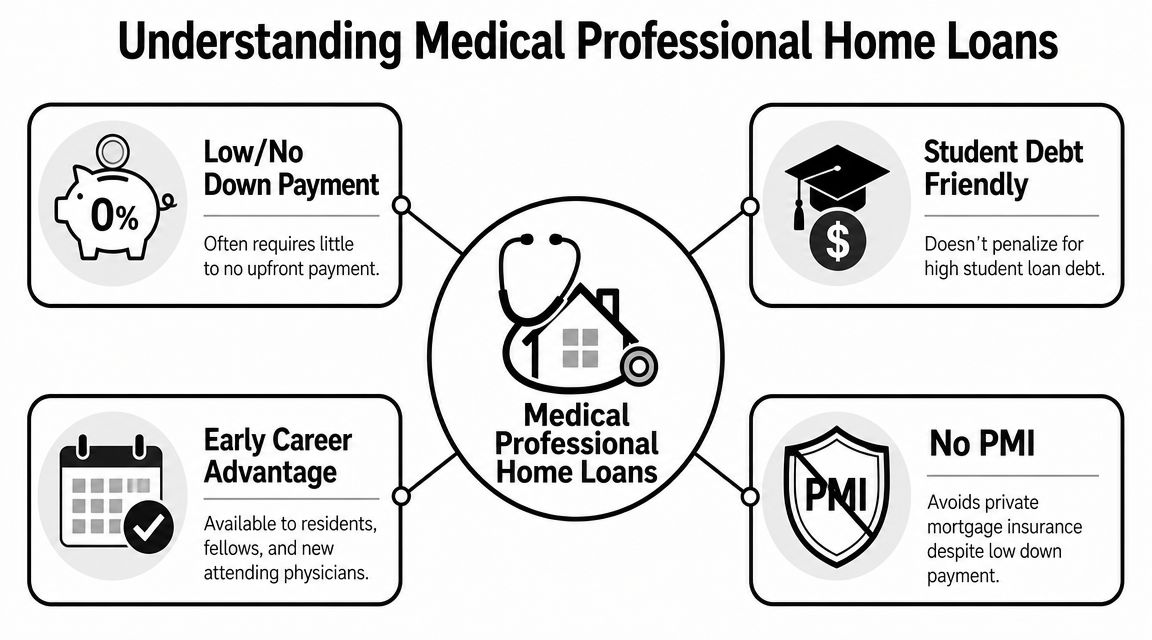

Understanding Medical Professional Home Loans

A medical professional home loan is a mortgage designed around the way healthcare careers work. I tell clients to think of it as a VIP pass for underwriting. Not a free pass. Not an easy pass. A smarter pass.

Traditional underwriting rewards borrowers who've had stable income for years, low debt, and plenty of cash sitting in the bank. Healthcare professionals often have the opposite pattern at the start. They've spent years building a career first, then income catches up later. Specialized medical loans exist because lenders know that pattern isn't a warning sign by itself.

What makes these loans different

The core idea is simple. The lender adjusts the rules to fit the profession.

That can mean low down payment options, no borrower-paid mortgage insurance, more flexibility around student debt, and approval paths for buyers who haven't even started their new job yet. These aren't gimmicks. They're underwriting choices built for medical careers.

Here's the practical version:

- Career timing matters: Some programs work for residents, fellows, and new hires before the first paycheck lands.

- Debt is viewed with more context: Student debt doesn't always get treated the same way it would under a standard conventional file.

- Cash isn't the only measure of strength: A borrower can be financially solid even without years of savings.

- Primary residence focus stays central: These programs usually target owner-occupied homes, not investment plays.

It's not just for physicians

Many articles miss the mark.

Yes, “physician loan” is the common label. But many lenders broaden eligibility to include healthcare roles beyond MDs and DOs. In California, that matters because the buyer pool is broader than the doctor-only framing suggests. Depending on the lender, the eligible group may include dentists, pharmacists, nurse practitioners, physician assistants, and other licensed medical professionals.

Practical rule: Don't assume you're excluded because you're not a physician. Ask about your exact license, degree, and employment status.

What these loans are meant to solve

These loans aren't meant to make a bad purchase affordable. They're meant to remove the artificial obstacles that hit qualified healthcare borrowers early in their careers.

They can help when:

- You're relocating for a new role: Contract-based approval can matter.

- You have strong future income but limited liquid savings: A lower cash requirement can preserve reserves.

- You need a primary home near work: Commute pressure in California is real.

- You want to avoid forcing a conventional loan to do a job it wasn't designed to do: That usually ends in frustration.

A good advisor should explain the limits just as clearly as the benefits. These are specialized programs, not universal ones. Eligibility can be tighter, and the wrong lender can still underwrite your file poorly.

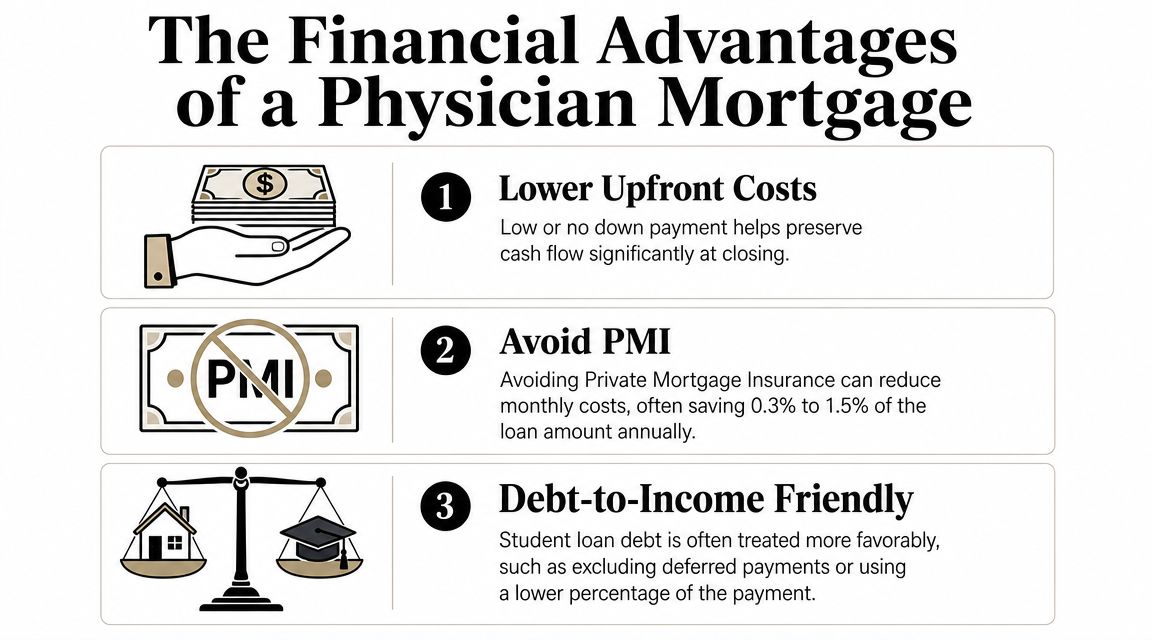

The Financial Advantages of a Physician Mortgage

A California medical buyer can have a strong income trajectory, excellent credit, and a signed job contract, yet still get boxed in by a standard mortgage. The problem usually comes down to two pressure points. You need a manageable cash requirement up front, and you need enough qualifying room to buy close to work in an expensive market.

That is why physician mortgage programs deserve a serious look.

Lower down payment pressure

The down payment structure is the first major advantage. Many physician loan programs allow far less cash down than borrowers expect, which can make a real difference in California, where even a modest starter home can require a painful amount of cash if you go conventional.

Keeping more money in reserve is usually the smarter move for healthcare professionals early in their careers. You may be covering a move, furnishing a new home, paying licensing costs, or trying to avoid emptying your savings account right after closing. A low-down-payment option helps you buy without putting yourself in a weak cash position.

That matters more in California than in lower-cost states.

No borrower-paid PMI

This is the monthly payment advantage that gets overlooked. Many physician mortgage programs do not charge borrower-paid private mortgage insurance, even with a smaller down payment.

I tell clients to pay attention to total payment, not just rate quotes. A conventional loan with PMI can look competitive at first glance and still cost more every month once you compare the full housing expense. If you are buying in Los Angeles, San Diego, the Bay Area, Sacramento, or Orange County, that difference can affect what you can comfortably afford.

A loan with no borrower-paid PMI can put you in a stronger monthly position than a “lower-rate” loan that adds PMI on top.

Higher loan amounts can matter more than rate shopping

In California, loan size is often the primary issue. Specialized medical professional programs may go higher than standard conforming paths, which gives qualified borrowers another lane to buy a primary residence in high-cost areas.

That does not mean you should stretch just because a lender allows it. It means you should not rule yourself out based on conventional limits before you review the medical-specific options available to your profession. This is especially important for healthcare buyers whose income supports the payment but whose file does not fit a standard box cleanly.

Here is the practical comparison:

| Financial pressure point | Standard borrower problem | Why a medical mortgage can help |

|---|---|---|

| Upfront cash | Large down payment drains savings | Lower down payment options may preserve reserves |

| Monthly carrying cost | PMI adds cost | No borrower-paid PMI can lower total payment structure |

| Purchase price range | Conforming limits can box in options | Specialized programs may reach larger loan amounts |

California buyers should also look beyond physician-only branding. Some lenders extend these benefits to dentists, pharmacists, veterinarians, nurse practitioners, physician assistants, and other licensed healthcare professionals. California Loans for Heroes may also be worth reviewing if you want to check eligibility for California healthcare home loan programs built for a broader group of medical borrowers.

Program examples discussed above, including low down payment ranges, no-PMI structures, and higher physician loan amounts, are reflected in lender and industry guidance from Truss Financial Group's doctor mortgage overview.

Eligibility and Documentation for Your California Loan

Most borrowers ask the wrong first question. They ask, “Can I qualify?” The better question is, “Which underwriting lane fits me?”

A California medical borrower may be fully mortgage-worthy and still get a weak answer from the wrong lender. Eligibility for a home loan for medical professional borrowers usually depends on your occupation, license, credit profile, occupancy plans, and income documentation. But the two issues that matter most are often student debt treatment and how your employment is documented.

Student debt doesn't always sink the file

One of the strongest underwriting advantages in this niche is debt-to-income treatment. Some lenders exclude or discount deferred student debt from the DTI calculation if it has been deferred for at least 12 months, which can improve qualifying capacity, as described in Harvard FCU's medical professionals home loan guidance.

That matters because a standard DTI review can punish borrowers whose income is solid but whose education debt distorts the file. If the lender can exclude qualifying deferred debt, your approval picture may look much closer to financial reality.

Here's the practical takeaway:

- Deferred student debt can help, if documented correctly: Timing matters.

- Not every lender handles this the same way: Program guidelines vary.

- You need the file reviewed by someone who knows where to look: This is not a “submit and hope” situation.

A signed contract can be enough

This is another feature that changes the game for residents, fellows, and new hires.

Some medical professional programs allow borrowers to qualify using a signed employment contract rather than current pay stubs. If you're moving to California for a hospital, clinic, or practice role, that can make the difference between buying before your start date and waiting until after you've already settled into expensive temporary housing.

If you're starting a new healthcare job soon, don't assume you must wait for several pay cycles before applying. Ask whether your contract can support approval.

Basic checklist to prepare your file

Every lender will have its own documentation standards, but a strong application usually starts with a clean package. Use this as your working checklist:

- License and professional credentials: Your lender may want proof of your healthcare designation.

- Employment documentation: Offer letter, signed contract, or employer verification can be central.

- Income documents: If you're already working, expect the usual income paperwork.

- Asset statements: Show what you have available for down payment, closing costs, and reserves.

- Debt documentation: Especially student loan statements and deferment details where relevant.

- Occupancy plan: These programs usually focus on a primary residence.

A lot of uncertainty disappears once the right lender reviews the actual file. If you want a quick gut check before gathering everything, start with the California HERO eligibility review. It helps you sort out whether your profile fits before you waste time chasing the wrong loan.

My blunt advice on eligibility

Don't self-reject.

I've seen too many healthcare professionals assume they won't qualify because they have student debt, a pending job start, or not enough saved for the version of home buying they imagine is required. Specialized lending exists because your financial path isn't standard. Judge your options based on the actual program, not on conventional loan myths.

Comparing Your California Home Loan Options

Buyers need clarity, not marketing. A medical professional mortgage can be a strong fit, but it's not the only option. In California, you should compare it against conventional financing, FHA, and hero-focused programs that may offer different forms of support.

One option in that mix is the California HERO home loan program, which serves eligible California heroes including healthcare professionals and can be part of the broader decision set when you're weighing purchase financing.

What changes from one loan type to another

The biggest differences usually show up in four places:

- Cash needed up front

- Mortgage insurance structure

- How student debt affects approval

- How forgiving the program is for early-career borrowers

Academy Bank notes that physician and broader medical-professional loans often use high loan-to-value financing, commonly 90% to 100%, with no borrower-paid mortgage insurance, though the tradeoff can be tighter eligibility rules, as described in its doctor mortgage program overview.

That's the lens you should use. Not “Which loan sounds familiar?” Ask, “Which loan matches my actual file and my California target price?”

Home Loan Comparison for California Medical Professionals

| Loan Type | Minimum Down Payment | PMI Required? | Student Debt Treatment | Best For… |

|---|---|---|---|---|

| Medical professional loan | Often low down payment, with some programs offering high loan-to-value financing | Often no borrower-paid mortgage insurance | May be more flexible, especially for qualifying healthcare borrowers | Licensed medical professionals with strong career trajectory and limited cash |

| HERO Program | Varies by loan structure and borrower profile | Varies by loan type | Depends on the underlying mortgage and qualification path | California healthcare workers who want hero-focused support and to explore assistance options |

| FHA loan | Lower down payment structure than many standard loans | Mortgage insurance typically applies | Standard FHA treatment | Buyers who need a more broadly accessible option |

| Conventional loan | Depends on program and price point | Often required when down payment is below the usual threshold | Standard conventional treatment | Borrowers with stronger reserves, straightforward income, and fewer underwriting complications |

My recommendation

Don't choose based on brand familiarity. Choose based on fit.

If you're a healthcare professional with heavy student debt, a new contract, or a need to conserve cash, start by testing the medical professional route. If your profession or file doesn't line up cleanly with that path, compare it against hero-focused options and standard agency products.

The wrong move is forcing yourself into a conventional loan just because it's the one everyone has heard of.

Your Next Steps to Secure Your Home Loan

The mortgage process feels complicated when you look at it all at once. It gets manageable when you handle it in sequence.

In California, speed matters, but sloppy speed kills deals. The right approach is organized, fast, and realistic. If you're buying as a healthcare professional, here's the order I recommend.

Step one, get pre-approved before you shop

Don't browse listings first.

A real pre-approval tells you which loan structure fits, what documentation the lender needs, and whether your price range is workable in your target area. For medical borrowers, this step is where contract income, reserves, and student debt treatment start getting evaluated properly.

Step two, build a clean document file

You want your application to move like a professional file, not a patchwork file.

Gather the basics early:

- Identity and license documents

- Employment contract or income records

- Asset statements

- Student loan documentation

- Any explanation needed for career transitions or relocation

A complete file gives your lender fewer excuses to slow down.

Step three, match the home search to the loan

This part gets overlooked.

A loan may work beautifully at one price point and become much less attractive at another. In California, that shift can happen fast depending on county, property type, reserves, and appraisal reality. Shop with your actual approved structure in mind, not with broad internet estimates.

The cleanest transactions happen when the loan strategy comes first and the house hunt follows it.

Step four, stay responsive through escrow

Once you're in contract, your job is simple. Be easy to underwrite.

Answer conditions quickly. Send updated documents fast. Don't open new debt unless your lender says it's fine. Don't change jobs mid-transaction unless the lender has already signed off. Most purchase delays aren't mysterious. They come from avoidable borrower-side timing problems.

Step five, close with a payment you actually want to live with

Don't focus only on getting approved.

Focus on whether the final payment fits your life, your schedule, and your post-closing liquidity. California homeownership is expensive enough. You want a structure that leaves room for the rest of your financial life, not one that drains every reserve just to get the keys.

Get Your Medical Professional Home Loan Questions Answered

Most final questions come down to edge cases. Not whether these programs exist, but whether they fit your exact situation.

The short answer is this: sometimes yes, sometimes no, and the details matter more in California than in cheaper markets.

Common questions I hear from healthcare buyers

Can I use a medical professional loan for an investment property?

Usually, these programs are aimed at primary residences. If you're trying to house hack or buy purely as an investment, expect tighter limits or a different loan path altogether.

Do non-physician healthcare professionals qualify?

Often, yes. But don't assume all lenders treat all professions the same way. One lender may include certain licensed roles that another lender excludes.

Can I buy before I start my new job?

In some cases, yes. Contract-based underwriting can help if your offer is solid and timed correctly.

What if I'm self-employed in a medical field?

That gets more nuanced. Strong income can still qualify, but self-employment adds another layer of documentation and review.

Will this automatically be better than a conventional loan?

No. It needs to be compared side by side. A specialized program is useful when it solves your actual bottleneck.

The California reality

California punishes vague planning. The state is too expensive for guesswork, and healthcare schedules are too demanding to spend weeks talking to lenders who don't understand your file.

If you're serious about buying, get your scenario reviewed by someone who understands healthcare income, contract timing, student debt complications, and high-cost California transactions. A generic online lender may give you an answer. That doesn't mean it's the right one.

The right mortgage strategy should fit your profession, your market, and your next move. If it doesn't, it's not a strategy. It's a guess.

If you're a nurse, physician, pharmacist, dentist, PA, or other California healthcare professional trying to make sense of your options, California Loans for Heroes can help you review programs that fit your role, your timeline, and your target market in California.