If you're a teacher in Riverside, a nurse in Orange County, a firefighter in the Central Valley, or a veteran trying to buy anywhere near the coast, you've probably had the same thought: the monthly payment might be manageable, but the cash needed upfront feels impossible. That's where most California buyers get stuck. Not on income. Not on motivation. On the down payment, closing costs, and the belief that they need years more to save.

That belief is often wrong.

Down payment assistance isn't some obscure side program for a tiny group of buyers. It's a real part of the mortgage market. As of Q3 2024, the U.S. had 2,444 homebuyer assistance programs, 81% of them were currently funded, and the average benefit was about $17,000, according to this housing-assistance market report. That's enough to materially change your cash-to-close.

Making Homeownership a Reality with Down Payment Assistance

California public service workers get hit from both sides. Home prices are high, and your job doesn't always fit a cookie-cutter mortgage file. Teachers may rely on contract timing. Nurses may have shift differentials. Firefighters and law enforcement often earn overtime that needs to be documented correctly. Veterans may qualify for one set of benefits and still miss another because nobody layered the financing properly.

That doesn't mean you're priced out. It usually means your plan is incomplete.

The practical question isn't whether help exists. It's how to get down payment assistance without wasting weeks on the wrong program, the wrong lender, or the wrong assumption about eligibility. If you want a useful starting point on what assistance may cover, review this breakdown of how much down payment assistance can cover.

Why DPA matters in California

The biggest mistake I see is buyers treating down payment assistance like a bonus. It isn't. In California, it can be the tool that moves you from “almost ready” to “offer-ready.”

Here's the shift you need to make:

- Stop thinking only about the down payment. You need to look at total cash to close.

- Stop assuming assistance is only for low-income buyers. Many programs are targeted by location, occupation, buyer type, or financing structure.

- Stop waiting to save blindly. If a program fits your file today, waiting may cost you more than it saves.

Practical rule: If you can support the monthly payment but the upfront cash is the barrier, you should screen for DPA before you decide homeownership is out of reach.

What this means for service professionals

Public-service buyers often have an advantage that generic homebuyer content ignores. Many assistance programs are built around stable employment, public-service occupations, local residency goals, or community workforce needs. That matters in California, where cities and counties often want teachers, healthcare workers, first responders, and veterans to live in the communities they serve.

You don't need more generic advice. You need a mortgage strategy that starts with your job profile, your city, and your actual buying timeline.

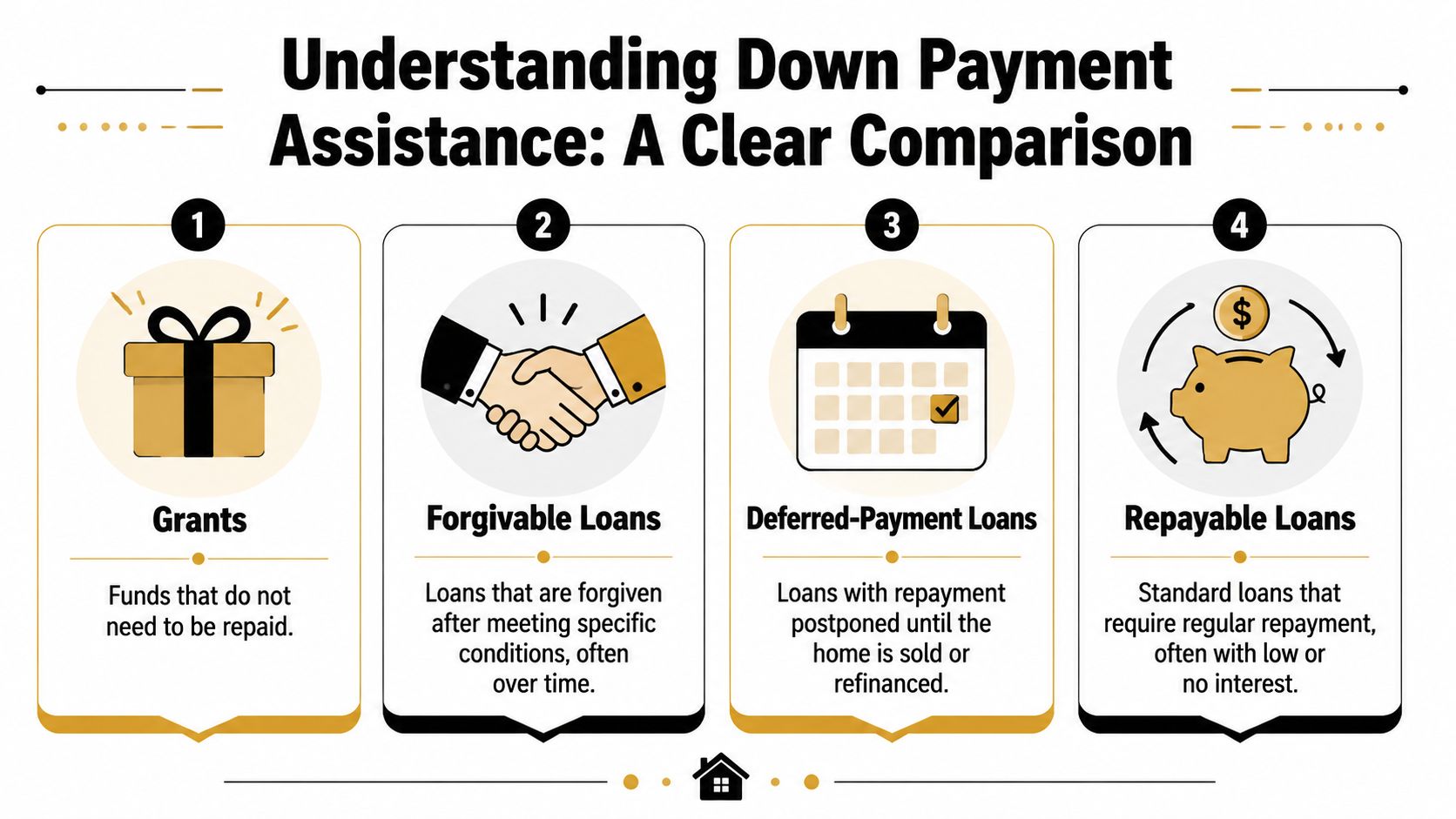

Decoding the Types of Down Payment Assistance Available

Most buyers hear “assistance” and assume free money. That's the wrong starting point. In real-world lending, most DPA is structured financing.

By June 2023, the U.S. had 1,676 funded DPA programs, and nearly 90% were structured as second mortgages rather than grants. The same analysis found 62.1% required borrowers to be first-time homebuyers and 72.7% imposed income caps, often with 45% limited to households below 80% of area median income, according to Urban Institute's review of funded DPA programs.

The four structures that matter most

You should compare DPA the same way you'd compare mortgages. Not by the headline, but by the terms.

| Assistance Type | How It Works | Repayment | Best For |

|---|---|---|---|

| Grants | Funds are applied to down payment or closing costs and don't require repayment under the program terms | None, if the program is a true grant | Buyers who want the cleanest structure and qualify for limited grant inventory |

| Forgivable loans | Assistance starts as a loan, then gets forgiven if you meet occupancy or time requirements | Repaid only if you trigger a sale, refinance, transfer, or fail a program rule before forgiveness | Buyers who expect to stay in the home long enough to clear the forgiveness period |

| Deferred-payment loans | Payments are postponed while you own and occupy the home | Usually due later, often on sale, refinance, or maturity | Buyers who need low upfront cash pressure and can manage future trigger risk |

| Low-interest second mortgages | A separate junior lien helps fund the transaction | Repaid based on the note terms, sometimes monthly, sometimes on a trigger event | Buyers who qualify for layered financing and want predictable terms |

A lot of California buyers end up using assistance through a first mortgage plus a second-lien structure. If you're comparing loan options, this overview of a conventional loan with down payment assistance is worth reading because it shows how these layers often work together.

Which type should you choose

Don't chase the biggest advertised benefit. Chase the structure that fits your timeline.

If you expect to move in a few years, a forgivable loan can backfire if the forgiveness period is longer than your likely stay. If you're in a stable job, buying in a city where you expect to stay put, a forgivable structure can be excellent. If your career may require relocation, a cleaner grant or a more flexible second mortgage may be safer.

A DPA program only helps if it still makes sense when you factor in repayment triggers.

What to ask before you apply

Ask these questions before you spend time gathering documents:

- Is it a true grant or a second mortgage? The answer changes everything.

- What triggers repayment? Sale, refinance, transfer of title, or moving out can all matter.

- Is there a forgiveness period? If yes, how long do you realistically expect to own this home?

- Can it be layered with your first mortgage type? Some combinations work. Some don't.

A smart buyer reads the assistance note with the same care they read the mortgage note.

How to Find and Qualify for California DPA Programs

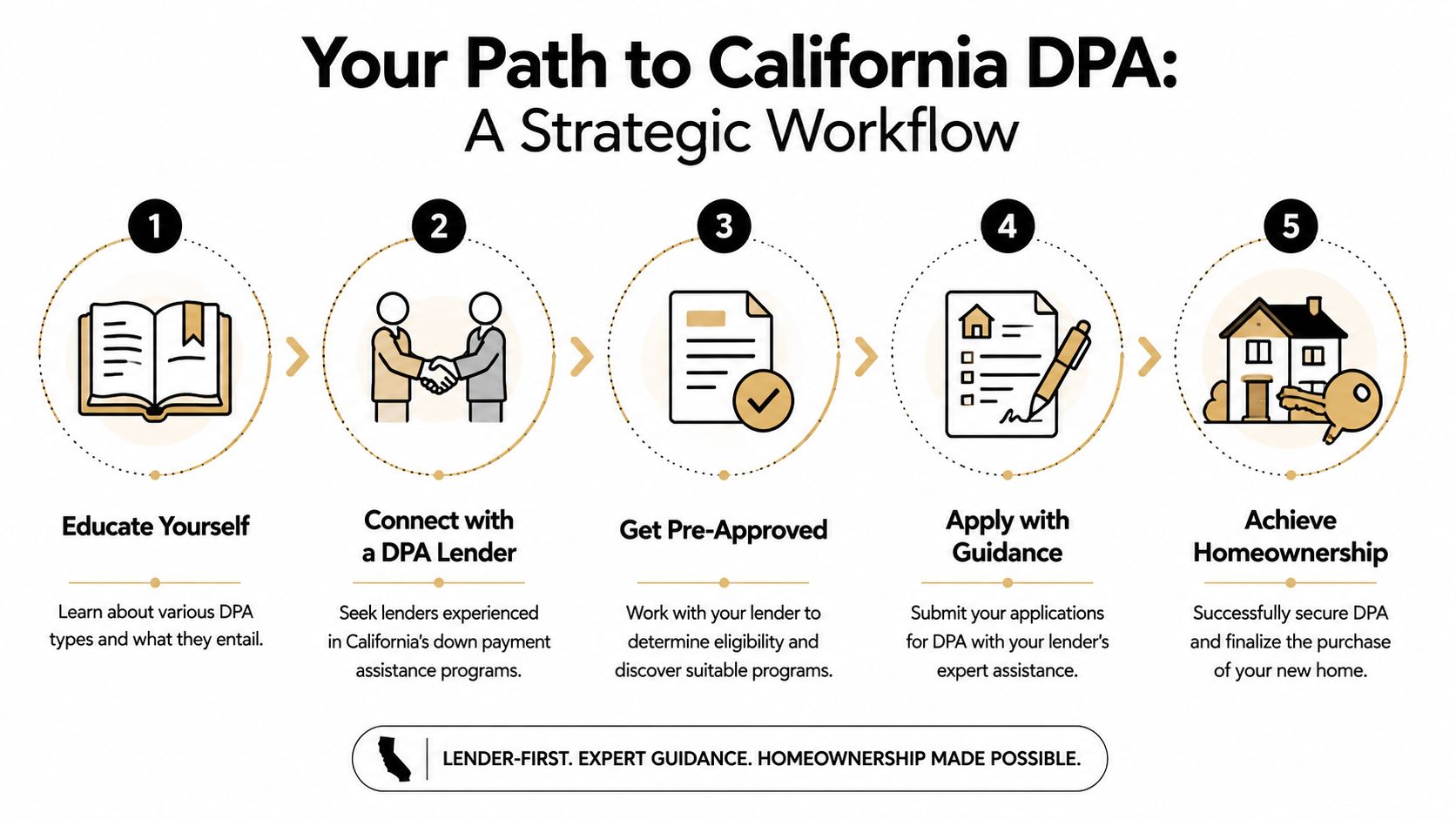

Many individuals start in the wrong place. They go searching for programs before they know whether their loan file can support them. That creates confusion fast.

The efficient path is lender first. Get pre-approved, then filter programs based on the financing you qualify for. Neutral program guidance consistently shows that many DPA products require at least a 620–640 credit score, debt-to-income caps around 45%–50%, and completion of a homebuyer education course. It also warns that the fastest way to get disqualified is applying before you confirm local eligibility and lender participation requirements, according to this practical guide to how DPA works.

Use a lender-first workflow

This is the process I recommend for California buyers:

Get pre-approved first.

You need a real payment range, not a guess. That includes your target sales price, estimated monthly payment, loan type, and usable cash.Screen for the hard limits.

Focus on income caps, minimum credit score, DTI limit, occupancy rules, property type, and whether the program only works with participating lenders.Check geography carefully.

In California, city, county, and local housing-authority boundaries matter. A property can qualify in one area and fail in another.Confirm education requirements early.

Many programs require a homebuyer education course. Don't leave that to the last minute.Build a shortlist, not a wish list.

You only need a few realistic options that fit your loan, your occupation, and your purchase area.

What lenders and programs usually look at

California DPA qualification often comes down to a handful of underwriting pillars:

- Income eligibility: Many programs use AMI, which means area median income. Your household income may qualify in one county and miss in another.

- Credit score: A thin file or recent late payments can knock you out even if your income is solid.

- DTI ratio: Student loans, car loans, and credit cards can squeeze your eligibility fast.

- Occupancy: Most assistance is for a primary residence. Renting it out later may trigger issues.

- Program compatibility: The first mortgage and the assistance layer must work together.

Buy the house and the assistance as one financing package. Don't treat them as separate decisions.

Where California buyers should actually look

Start with statewide and local sources, then verify lender participation. That usually means CalHFA, city housing departments, county housing agencies, local housing authorities, and occupation-focused programs. You can also work with lenders that specifically help hero professions understand these options, including California Loans for Heroes, if you want support identifying combinations that fit public-service buyers in California.

Documents to prepare before anyone asks

If you want speed, prepare your file like a serious borrower:

- Income records: Recent pay stubs, W-2s, and tax returns if needed.

- Asset records: Bank statements and any gift-fund documentation.

- Employment detail: Contact information, job status, and explanation of overtime or shift pay if applicable.

- ID and residence history: Standard identity and occupancy documentation.

- Education certificate: If your program requires a homebuyer course, complete it early.

The buyers who close faster are usually the ones who get organized before they fall in love with a property.

DPA Programs for California Veterans, First Responders, and Teachers

Generic DPA advice misses the point for hero professions. A veteran may not need a standard first-time-buyer path. A firefighter may have income that looks uneven on paper but is strong in practice. A teacher may buy on a school-year timeline. A nurse may qualify well, yet student debt complicates the file.

Those aren't edge cases. In California, they're common.

Many DPA articles fail to explain how assistance works for non-standard hero profiles such as repeat buyers or borrowers carrying higher debt. Program eligibility is nuanced, and some states maintain separate products for first-time and repeat buyers. Public-program information also shows that many local programs offer special funds for educators, protectors, firefighters, healthcare workers, and military homebuyers, as outlined on Maryland Mortgage Program's down payment assistance page.

Hero buyers should stop assuming they don't qualify

One bad assumption ruins more applications than bad credit. Buyers think, “I owned before, so I'm out,” or “My student loans kill this,” or “My VA benefit means I can't use any other assistance.”

That's not how this works.

Some programs separate first-time and repeat-buyer options. Some employer, municipal, or occupation-targeted funds can pair with other allowed sources. Some public-service buyers qualify not because they fit a generic buyer box, but because a local program wants workers in that profession living in that community.

If you're in law enforcement, EMS, education, healthcare, military service, or another public-service role, read what heroes should know about California home loan options before you assume your file is standard.

Where hero profiles often get mishandled

A lender who doesn't understand your profession can miss qualifying income or overlook better program matches.

Common examples include:

- Veterans and active-duty buyers: VA eligibility can reduce one barrier while DPA addresses another. The issue isn't either-or. It's whether the full stack is allowed.

- Firefighters and law enforcement: Overtime, specialty pay, and schedule patterns need to be documented correctly.

- Teachers and educators: Contract timing, district employment history, and local workforce-targeted programs may matter.

- Healthcare professionals: Shift differentials and higher debt from training can change how the file needs to be structured.

Hero profiles aren't harder. They just need a lender who knows what to look for.

Occupation-based aid is more common than buyers think

Occupation-specific support is not rare. In the Q3 2024 housing-assistance environment, special-purpose programs commonly targeted public-service roles, including educators, protectors, firefighters, healthcare workers, and military homebuyers, as noted earlier in the article from the national housing-assistance market review. That's exactly why California public-service workers shouldn't use generic search terms and hope for the best. They should search by profession, city, county, and mortgage type.

Navigating the DPA Application and Avoiding Common Mistakes

Most buyers focus on getting approved. Smarter buyers focus on staying approved and avoiding expensive surprises after closing.

The paperwork itself isn't the hard part. You'll usually need the standard mortgage file, plus program-specific documents, education certificates if required, and disclosures tied to the assistance lien. The main risk is signing up for terms you didn't fully understand.

The mistake that costs buyers later

A common pitfall is failing to understand the forgiveness clock and recapture risk. Some programs are fully forgiven after a set period, while others become repayable if you sell, refinance, or transfer title before that period ends. One public example is Invest Atlanta, which offers assistance that is fully forgiven after 5 years, while other programs can be much stricter, according to Atlanta Housing's down payment assistance program details.

That matters because many buyers choose the option with the lowest upfront cash requirement and never ask what happens if life changes.

Read the second lien like it matters

Because it does.

Before you sign, ask these questions in plain English:

- When does repayment start, if ever?

- What event triggers repayment?

- Can I refinance the first mortgage without creating a problem?

- What happens if I move for work?

- Is the assistance fully forgiven on a schedule, or all at once at the end?

If the lender or program rep can't explain the assistance note clearly, stop and get clarity before moving forward.

Think in layers, not line items

Your transaction is a capital stack. First mortgage, assistance layer, required buyer contribution, closing costs, reserves if needed. Every layer affects the next one.

That means a program that looks generous can still be a bad fit if it forces a larger buyer contribution, creates a resale issue, or blocks a future refinance. On the other hand, a smaller assistance amount can be the better move if it gives you cleaner terms and more flexibility later.

Cheap upfront money can become expensive money if the repayment trigger doesn't match your real life.

The avoidable delays I see most often

Some problems are simple and completely preventable:

- Buyers apply before checking participating lenders. Then they find out the program won't work with the lender they chose.

- They ignore occupancy rules. Assistance for a primary residence is not a shortcut to an investment property.

- They switch jobs, move funds around, or open new credit mid-transaction. That can affect both the first mortgage and the DPA approval.

- They wait too long on required education or disclosures. Bureaucracy moves slowly enough without self-inflicted delays.

DPA can save you real money. It can also create headaches if you treat it like free cash instead of a legal financing structure.

Your Next Step with California Loans for Heroes

If you've read this far, the path should be clear. Buying in California isn't just about qualifying for a mortgage. It's about building the right structure for your profession, your location, and your cash-to-close.

That matters even more for veterans, first responders, teachers, nurses, and other public-service buyers. Your file may be stronger than you think, but only if someone evaluates the income correctly, screens the right programs, and catches the restrictions before you're under contract.

Specialized guidance is vital. You need someone who understands DPA rules, California geography, public-service borrower profiles, and how to combine assistance with a workable first mortgage without wasting your time.

What a smart next move looks like

Don't start by browsing random programs for hours. Start by getting your numbers reviewed by a lender who works with California hero buyers every day. You want a clear answer to four things:

- What loan amount and payment range fit your file now

- Which assistance programs match your city, occupation, and income

- How the repayment or forgiveness terms affect your long-term plans

- What documents you need to move quickly when the right home appears

Why this approach saves time

Most buyers lose time in one of two ways. They either chase programs they were never eligible for, or they get pre-approved with someone who doesn't know how to layer assistance properly. Both mistakes cost time. In a competitive California market, time matters.

If you're serious about how to get down payment assistance, don't rely on broad national advice alone. Get your actual scenario reviewed. A public-service borrower in San Diego, Sacramento, Los Angeles, or the Inland Empire may have very different options even with similar income.

Homeownership isn't out of reach because you're a hero in California. It gets delayed because most buyers don't get the right strategy early enough.

If you're a veteran, first responder, teacher, healthcare professional, or other public-service worker in California, California Loans for Heroes can help you review your eligibility, identify down payment assistance options, and map out a purchase plan that fits your profession, budget, and location. Reach out to start with a real pre-approval strategy instead of guesswork.