You got pre-approved for a VA loan, you heard “zero down,” and you figured the hard part was over. Then the estimate shows cash needed for closing, prepaid taxes, insurance, and maybe a rate buydown. That's the moment a lot of California veterans get frustrated.

The problem usually isn't the VA loan. The problem is assuming zero down means zero cash to close.

That's where veteran down payment assistance matters. In practice, these programs often help cover the part of the transaction that still strains your savings, even when the first mortgage is a VA loan. In California, that gets more complicated because you may be looking at federal VA financing, state programs, local city or county assistance, and special eligibility rules that don't line up cleanly on their own.

My advice is simple. Don't shop for a VA loan and then separately look for assistance later. Build the financing strategy together from day one. That's how you avoid dead-end programs, missed funding windows, and contracts that fall apart because the lender and assistance provider weren't aligned.

Why Zero Down Payment on VA Loans Is Only Half the Story

A common situation goes like this. A veteran gets approved for a VA loan, starts touring homes in California, and feels confident because there's no down payment requirement. Then they get the first detailed cost breakdown and realize they still need money for closing costs, prepaid items, and whatever else the transaction requires.

That surprise is normal. It's also avoidable.

In Veterans United's 2023 Veteran Homebuyer Report, about 62% of service members and veterans said the ability to buy with no down payment was the top reason they use their VA home loan benefit. That tells you exactly why so many veteran assistance programs are built the way they are. They're often not trying to replace the down payment. They're trying to solve the leftover cash problem.

What catches buyers off guard

Most buyers focus on the headline benefit. No down payment. That part is real, and it's powerful.

But the transaction still has moving pieces:

- Closing costs: lender fees, title charges, escrow charges, and related settlement costs

- Prepaid items: homeowners insurance, property taxes, and daily interest

- Optional pricing choices: a rate buydown or credits structure that affects cash at closing

- Reserve pressure: some buyers want extra funds left after closing so they're not house-poor on day one

That's why veteran down payment assistance is often more useful than people expect. It can reduce the upfront strain enough to make the purchase workable.

Zero-down financing gets you in the door. Assistance is what often gets you across the finish line.

Why this matters more in California

California buyers don't need theory. They need a plan for high-cost markets, stricter local program rules, and timing issues that can kill a deal.

If you're comparing loan structures broadly, it helps to understand how assistance can work outside VA financing too, including a conventional loan with down payment assistance. But for eligible veterans, the smarter question is usually this: how do you preserve the advantage of VA zero-down while using assistance to shrink the rest of the cash needed?

That's the right framing. Not “Do I need help with the down payment?” but “What part of cash to close can I remove, reduce, or shift?”

Grants vs Forgivable Loans vs Deferred Payment Loans

Not all assistance is equal. Some money is effectively free. Some is free only if you stay in the home long enough. Some gets repaid later when you sell, refinance, or transfer title.

If you don't know which type you're using, you can make a bad decision even when the assistance amount looks attractive.

Down Payment Resource reported 61 programs specifically offering help to veterans and service members, with assistance amounts ranging from $2,000 to $120,000. That range tells you two things. First, there's real help out there. Second, the structure matters as much as the headline amount.

Down Payment Assistance Types Compared

| Assistance Type | Repayment Required? | Key Feature | Best For Veterans Who… |

|---|---|---|---|

| Grant | Usually no | Funds are provided without a repayment schedule | want the cleanest structure and qualify under strict program rules |

| Forgivable loan | Yes, unless forgiveness terms are met | Usually structured as a second mortgage that is forgiven over time | expect to keep the home long enough to satisfy the occupancy period |

| Deferred payment loan | Typically yes, later | Payment is postponed until a future trigger such as sale or refinance | need upfront help now and can plan for payoff later |

How I'd evaluate each option

Grants are the cleanest option. If you qualify, great. The issue is that grant programs can be narrow, competitive, and rule-heavy. Don't assume “grant” means easy.

Forgivable second mortgages can be excellent when you're planning to stay put. But read the forgiveness schedule carefully. If your military career, relocation plans, or family needs might force a move, that assistance may not stay free.

Deferred payment loans work well for buyers who need relief now and expect equity growth later. The catch is simple. A future refinance or sale may trigger repayment, so this isn't invisible money.

Practical rule: Don't chase the largest assistance amount first. Chase the structure that fits how long you'll own the home and whether you're likely to refinance.

What veterans should ask before choosing

Use these questions before you commit to any program:

- When does repayment happen: sale, refinance, payoff of first mortgage, transfer, or end of a term?

- Is there a forgiveness clock: if so, what actions reset it or violate it?

- Can it be used for closing costs: many veterans need that more than down payment funds

- Will the second lien affect future refinancing: this matters if you may lower your rate later

- Does the lender already know how to close it: if not, move on

If you want a broader breakdown of what these programs can pay for, review how much down payment assistance can cover. Then come back to the main decision. Not all help saves you money in the same way.

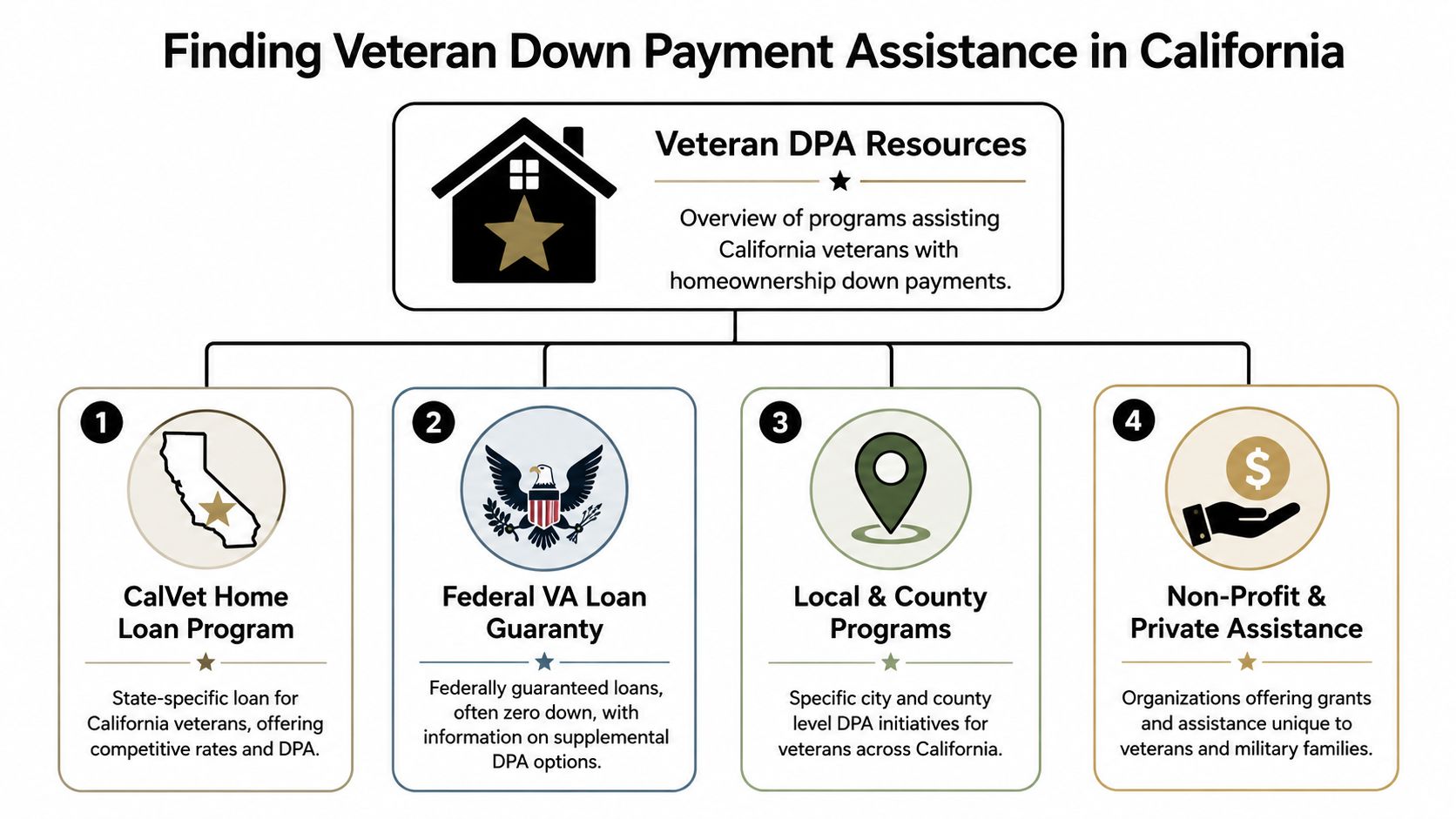

Finding Veteran Down Payment Assistance in California

California is where veteran down payment assistance gets interesting and messy fast. You may have a VA-eligible borrower, a statewide housing program, a county layer, a city layer, and a seller-credit strategy all interacting in one file. If the pieces don't fit, the deal stalls.

The biggest mistake is searching only for “veteran grants” and ignoring the larger map. In California, you need to look at four buckets: state-level options, federal VA financing, local city or county programs, and nonprofit or private assistance sources.

Start with the stack, not the program name

Veterans often ask, “What's the best program in California?” That's the wrong question.

The right question is: Which combination is allowed for my income, occupancy, property type, and lender?

A smart California search usually starts here:

Confirm your VA financing path

Make sure your first mortgage structure is solid before you chase assistance layers.Check statewide options

CalHFA and other state-connected channels may offer assistance, but availability and compatibility matter more than brand recognition.Search local housing agencies

County and city programs can be more useful than statewide ones, especially if they target specific neighborhoods or buyer profiles.Screen for veteran-specific overlays

Some programs care about disability status, surviving spouse status, first-time buyer definitions, or primary-residence occupancy.

The real reason files fail

The biggest issue usually isn't veteran eligibility. It's coordination.

The Virginia pilot guidelines are a good operational example because they show the core problem clearly: the main failure mode is often a mismatch between the lender, the DPA source, and the program rules. That same problem shows up in California all the time.

Here's what I tell buyers to verify before they write offers:

- Lender approval: Is your lender allowed to work with that assistance source?

- VA compatibility: Does the program explicitly permit a VA-financed first mortgage paired with its grant or second lien?

- Funding status: Is the money available right now?

- Property rules: Single-family, condo, multiunit, manufactured, or owner-occupied restrictions can all matter.

- Household income review: Program income doesn't always match what buyers assume from base pay alone.

If a program looks perfect on paper but your lender hasn't closed it before, treat that as a warning sign.

Where a California veteran should look first

I'd organize the search this way:

- State-level channels: check CalHFA-style offerings and veteran-oriented state resources.

- County housing departments: many buyers skip these, and that's a mistake.

- City homebuyer assistance offices: some local programs are more flexible than statewide alternatives.

- Mission-driven lenders and navigators: California Loans for Heroes works with California homebuyer assistance and hero-focused financing programs, which is useful when you need one party to line up the moving parts instead of handing you a list and sending you off.

That last point matters. A list of programs isn't a strategy. A workable stack is.

Your Application Roadmap From Pre-Approval to Closing

The cleanest veteran DPA files follow a sequence. The messy ones jump around, write offers too early, and try to fix eligibility problems after the contract is signed.

Step one through step three

Get your Certificate of Eligibility lined up early. The VA requires you to work through a private lender and obtain a COE. If you have full entitlement, VA loans generally require no down payment. If you have partial entitlement, you may need cash at closing. The VA process also requires the VA escape clause in the purchase contract and review of the Closing Disclosure at least 3 business days before closing, as explained in Veterans United's breakdown of why VA loans don't require a down payment.

Choose a lender who already understands stacked files. Many veteran DPA programs work as a VA-backed first mortgage plus a grant or second lien. That structure is normal. What changes is the amount of documentation and coordination.

Assemble your paperwork before you shop seriously. Most buyers should expect to provide income documentation, asset statements, identification, service-related eligibility records where required, and any paperwork tied to local assistance screening.

Step four through closing

The second half is where timing matters.

- Pre-qualification screening: some programs require this before reservation

- Homebuyer education: many assistance providers won't waive it

- Housing counseling: this can be mandatory, especially in more structured programs

- Contract review: assistance terms may affect what needs to appear in the file

- Final disclosure review: don't wait until the end to understand how the assistance shows up

A stacked VA plus DPA file usually closes fine when everyone starts early. It gets ugly when the buyer goes under contract first and asks questions later.

The practical benchmark is to use assistance for the costs that stop the transaction, such as closing costs, prepaid items, or a rate buydown. If you need more context on those expenses, review closing cost assistance for veterans.

Timeline expectations that save deals

Don't treat a DPA transaction like a plain vanilla mortgage.

A layered file often has extra approvals, extra signatures, and extra document review. If the assistance provider needs education completed, counseling certificates uploaded, or income reviewed under its own formula, your closing timeline can stretch. Build that into your offer strategy. A rushed escrow is one of the easiest ways to lose assistance you otherwise qualified for.

Pro Tips for Maximizing Your Veteran Homebuyer Benefits

Most buyers don't lose assistance because they're unqualified. They lose it because they assume the rules are simpler than they are.

The trend is toward more specialized programs, not broad easy money. HousingWire's coverage of veteran-focused assistance notes that many DPA programs have layered requirements beyond veteran status, such as income caps, first-time buyer rules, primary-residence rules, and more specialized eligibility categories. That's exactly what I see in real files.

The mistakes I'd avoid immediately

- Don't assume veteran status alone qualifies you. Some programs add income limits, occupancy requirements, or household composition rules.

- Don't count on funding until it's reserved. Assistance availability can change while you're shopping.

- Don't switch lenders casually midstream. The new lender may not be approved for the same assistance channel.

- Don't ignore property restrictions. The home itself can disqualify the program even if you qualify personally.

The best veteran down payment assistance program isn't the one with the biggest headline. It's the one you can actually close without breaking your long-term plan.

How to think like a disciplined buyer

Use this checklist before you make an offer:

Check the AMI rule carefully. If a program uses an Area Median Income threshold, ask how your household income is calculated. Don't guess.

Ask whether first-time buyer rules are waived or enforced. Veterans often hear blanket statements on this topic. Get the answer tied to the exact program.

Confirm owner-occupancy requirements. If you plan to move later, rent the home, or buy a multiunit property, that can matter right away.

Review the second-lien terms. If the assistance is structured as a deferred or forgivable loan, ask what happens when you refinance, sell, or transfer title.

My strongest opinion on this process

You should be skeptical of any lender who says, “We'll figure out the assistance later.”

That approach burns time and creates false confidence. The loan, the assistance source, the property type, and the timeline need to fit together before you write an offer. If they don't, you're not being aggressive. You're being careless.

Take the Next Step Toward Homeownership

California veterans have a real advantage in the market. The VA loan is one of the strongest home financing tools available. But if you stop at “zero down,” you leave money on the table and risk walking into escrow underprepared.

Veteran down payment assistance works best when it's treated as part of the original financing design. Not an afterthought. Not a last-minute add-on. A real strategy.

That strategy needs to answer a few hard questions. Which costs are you trying to reduce? Which assistance structure fits your timeline? Which state or local programs can legally and practically stack with your VA loan? Which lender can coordinate the file without creating delays?

Those are the questions that matter in California.

A lot of buyers spend weeks browsing program lists and still don't know what applies to them. That's because eligibility on paper and eligibility in a live transaction aren't the same thing. The right move is to narrow the search quickly, verify the rules upfront, and build an offer plan around the programs that are workable.

This visual gives you a sense of the homebuyer support framework available through the publisher's platform.

If you're serious about buying, don't wait until you've found the perfect house to ask how the assistance works. By then, you may be too late for education requirements, approvals, or reservation timing.

Start with the financing stack. Confirm the rules. Then shop with confidence.

If you want help sorting through veteran down payment assistance in California, talk with California Loans for Heroes. They can help you review VA financing, identify assistance options that may fit your household, and see whether your loan can be structured to reduce cash to close before you start making offers.