A lot of California buyers have the same problem. They earn solid income, they've kept their credit in shape, and the monthly payment might be manageable, but the upfront cash feels impossible.

That's especially true for nurses working long shifts, teachers trying to buy near the communities they serve, firefighters with reliable income, or law enforcement officers who are ready to stop renting. In California, the issue often isn't whether you can handle a mortgage. It's whether you can pull together enough money for the down payment, closing costs, and reserves without draining every account you have.

That's where a conventional loan with down payment assistance can become a real strategy instead of just a hopeful idea. Used the right way, it can help a buyer bridge the gap between stable income and limited liquid cash. Used the wrong way, it can create extra payment pressure, refinancing limits, or closing delays.

For California Heroes, that distinction matters. In a high-cost market, the answer isn't just “yes, you can combine them.” The better question is whether the specific structure fits your profession, your county, your timeline, and the way you plan to use the home over the next several years.

The California Homeownership Dream Meets Reality

A registered nurse in Southern California might make enough to qualify for a mortgage on paper. A teacher in the Central Valley might have steady employment and strong budgeting habits. A first responder in a coastal county might be fully capable of handling a house payment that's close to current rent. Yet all three can hit the same wall at the same moment. Cash to close.

That wall is higher in California because prices are higher, and higher prices magnify every upfront requirement. Even buyers who've done everything right can feel stuck. They're not reckless. They're not unqualified. They're just trying to buy in a market where saving for a down payment while also paying California living costs is hard.

Why this hits Heroes especially hard

Public service professionals often have dependable income, but that doesn't mean they have excess liquidity. Shift workers may have overtime income that helps them qualify, while student loans, child care, commuting costs, or family obligations slow down savings. The result is common. Good borrower. Thin cash position.

That's why this topic matters. A conventional loan with down payment assistance isn't a loophole. It's a financing strategy that can help buyers move sooner when the main obstacle is upfront funds, not long-term ability to pay.

Many buyers don't need a different career or a different goal. They need a financing structure that matches how their money actually flows.

What practical buyers need to know

The question isn't whether down payment assistance exists. It's whether the version available to you works with a conventional loan, fits the property, and leaves you with a payment you can still live with after closing.

For California Heroes, the strongest approach usually starts with four questions:

- How much cash are you short by relative to the total funds needed at closing?

- What does the assistance look like in your area, grant, forgivable second, deferred second, or repayable second?

- How will that structure affect flexibility if you refinance, move, or keep the home for only a few years?

- Are there profession-based programs that improve the fit beyond standard first-time-buyer options?

Those details determine whether this becomes a smart purchase strategy or just a rushed way to get into escrow.

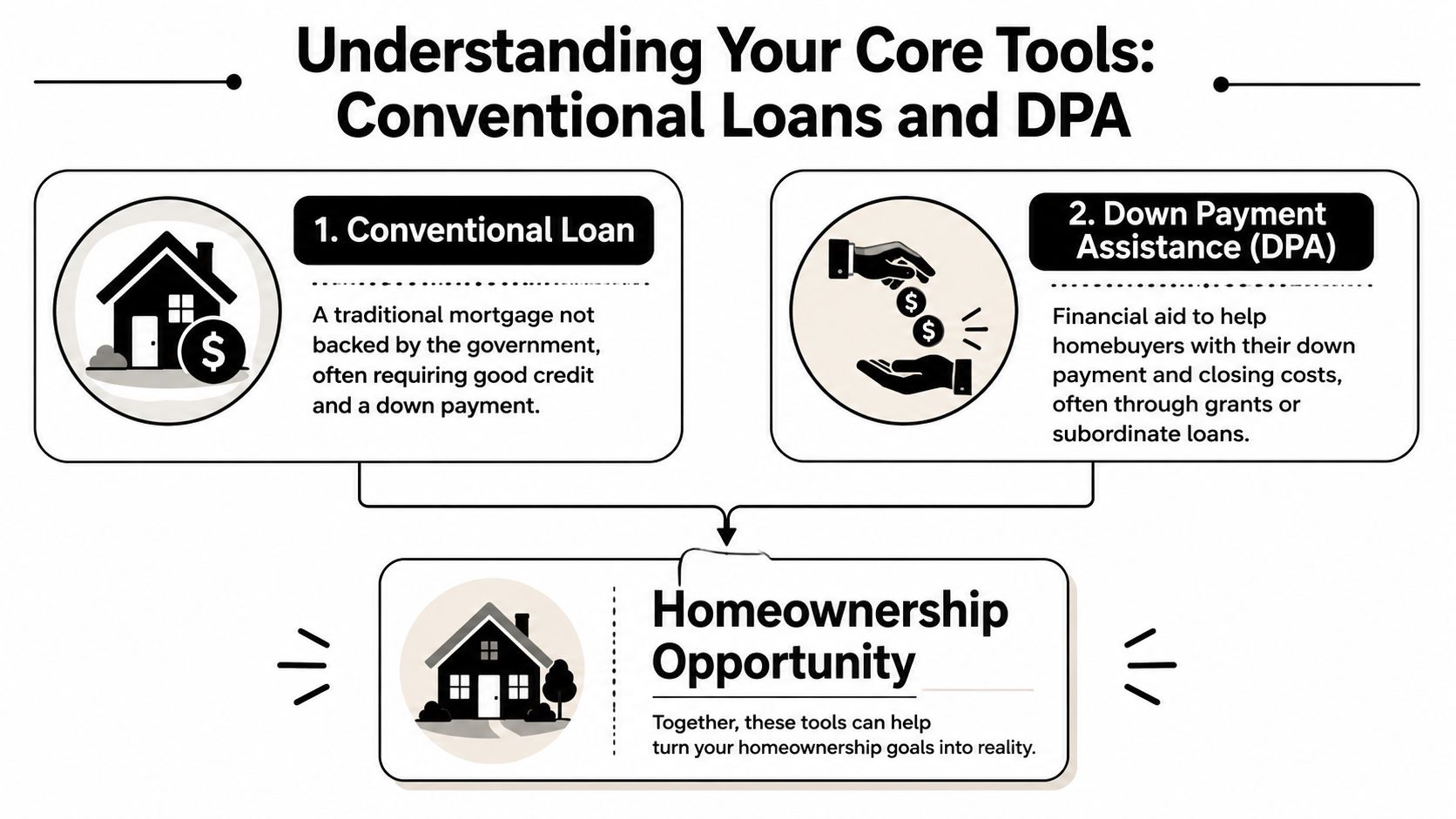

Understanding Your Core Tools Conventional Loans and DPA

A conventional mortgage is the main loan. Down payment assistance is the support layer. When they work together correctly, they can solve a very specific problem: you qualify for the house, but you don't want the upfront cash requirement to stop you.

What a conventional loan actually is

A conventional loan is a mortgage that isn't insured by a government program like FHA or VA. For many California buyers, it's attractive because it can pair well with owner-occupied purchases, and it often gives more flexibility than buyers expect.

The important baseline is simple. Conventional mortgages typically require at least 3% down, and buyers who put down less than 20% generally pay private mortgage insurance. That makes cash-to-close the central issue for many households, especially first-time buyers and buyers trying to preserve emergency reserves. A large homeowner survey found that 40% of homeowners said they received financial help with the down payment on their current home, up from 35% in 2023, with much higher shares among Gen Z homeowners at 78% and millennials at 56% than baby boomers at 12%. The same survey found that more than a third of recipients said they would not have been able to buy when they did without that help, according to LendingTree's down payment help survey.

What DPA does and what it does not do

Down payment assistance, or DPA, doesn't replace the first mortgage. It helps cover part of the upfront burden tied to buying the home. Depending on the program, it may also help with closing costs.

Think of it this way. The conventional loan is the car. DPA is what makes the purchase possible without waiting much longer to save.

But DPA isn't automatically free money. Sometimes it's a grant. Sometimes it's a second loan with no monthly payment. Sometimes it's forgivable after you stay in the home long enough. Sometimes it has to be repaid when you sell or refinance.

That's why buyers need to compare more than rates. They also need to compare structure. If you're still learning how lenders price and compare first mortgages, this guide on how to compare mortgage rates helps frame that part of the decision.

Why the combination matters in California

In a high-cost market, smaller down payment options can open the door sooner. The tradeoff is that lower upfront cash usually means a higher financed balance, PMI, or a layered assistance structure that affects future flexibility.

Practical rule: Don't judge a conventional loan with down payment assistance by the down payment alone. Judge it by total cash to close, monthly payment, and what happens if you refinance or move.

That's the level where good decisions get made.

The Rules of Engagement Combining DPA with a Conventional Loan

Yes, you can combine down payment assistance with a conventional loan. The important part is doing it in a way that satisfies the first mortgage rules, the assistance program rules, and the lender's own overlays all at the same time.

What the national guidelines allow

For a conventional loan, Fannie Mae permits eligible down payment and closing-cost funds to come from a variety of sources, and conventional programs can accept DPA when the assistance meets the investor's source-and-documentation rules. The main constraint is structural. The assistance has to be documented and set up in a way that still satisfies loan eligibility and mortgage insurance rules, especially when the borrower puts down less than twenty percent and PMI is involved, as outlined by Fannie Mae's guidance on down payment and closing cost assistance.

That means DPA is not some side arrangement that gets ignored during underwriting. It is part of the transaction file. Underwriters want to know where the money comes from, whether repayment is required, whether there's a lien, and how that affects qualification.

Where deals actually get complicated

Most buyers hear “allowed” and assume “easy.” Those aren't the same thing.

A conventional loan with down payment assistance can run into issues when:

- The DPA source isn't documented correctly and the lender can't use it.

- The assistance creates repayment terms that change how debt-to-income is evaluated.

- The second lien structure conflicts with what the investor or mortgage insurer will accept.

- The lender has overlays that are stricter than the baseline agency rule.

- The closing timeline is too tight for the first mortgage and DPA approval process to move together.

What experienced lenders do differently

A lender who handles these combinations regularly won't treat DPA as an afterthought. They'll review the full structure early, not after you're already in contract.

That usually means checking:

- Program compatibility with the conventional product.

- Lien position and repayment terms of the assistance.

- Income, property, and occupancy rules from both sides.

- Mortgage insurance treatment when the borrower is below the standard equity threshold.

- Timing risk so the escrow period doesn't become the problem.

If the lender can't explain how the assistance is documented and how it affects underwriting, the file is not ready.

That's why the right question isn't “Do you offer DPA?” The better question is “How often do you close conventional loans that include DPA, and how do you structure them before pre-approval goes out?”

Decoding the Different Types of Down Payment Assistance

Not all assistance lowers your stress the same way. Some options reduce upfront cash without hurting the monthly payment much. Others solve the cash problem today but create tradeoffs later if you refinance, sell, or need more flexibility.

The four structures buyers usually encounter

The common DPA forms are grants, forgivable second mortgages, deferred second mortgages, and repayable second mortgages. The names matter because the legal structure affects your payment, your future options, and your total cost.

A useful real-world example comes from New Jersey. Its statewide DPA offers up to $15,000 and can be combined with a 30-year fixed-rate conventional loan. The assistance is structured as an interest-free, five-year forgivable second loan with no monthly payment. First-generation buyers can receive an additional $7,000, bringing total aid to $17,000 to $22,000 depending on the county, according to state housing finance agency program details summarized here. That's one example of how a forgivable structure can preserve monthly affordability while still helping with upfront cash.

Down Payment Assistance Types Compared

| DPA Type | Repayment Required? | Impact on Monthly Payment | Best For… |

|---|---|---|---|

| Grant | Usually no | Often little to no direct impact from the assistance itself | Buyers who need upfront help and want the cleanest long-term structure |

| Forgivable second mortgage | Sometimes, if you sell, move, or don't meet the occupancy period | Often no monthly payment during the forgiveness period, depending on structure | Buyers who expect to stay put long enough to satisfy forgiveness rules |

| Deferred second mortgage | Usually yes, but often later rather than monthly | Can preserve current cash flow because payment may be delayed | Buyers who need cash-to-close relief now and can plan around future repayment |

| Repayable second mortgage | Yes | May increase monthly obligations if it amortizes | Buyers whose main goal is getting in now and who still qualify comfortably with the added debt |

How to choose the right structure

A California Hero buying in a high-cost area shouldn't focus only on how much assistance is available. The smarter move is to line up the assistance type with your expected timeline.

- If you may refinance soon, be careful with assistance that becomes due when the first loan changes.

- If your monthly budget is tight, a repayable second can solve one problem and create another.

- If you're likely to stay for years, forgivable assistance can be very efficient.

- If you want simplicity, a grant is usually the easiest version to live with.

For buyers comparing programs, this overview of down payment assistance options is a useful starting point before you narrow it down with a lender.

The best DPA structure isn't the one with the biggest headline amount. It's the one that still makes sense on the day you buy, the year you refinance, and the day you eventually sell.

Exclusive Programs for California Heroes

California buyers often search for broad first-time-buyer programs and stop there. That misses a big part of the opportunity. Many state and local DPA programs are aimed at selected occupations, and that matters for nurses, teachers, law enforcement personnel, firefighters, veterans, military borrowers, and other public service professionals.

Why profession-based targeting matters

A generic buyer may qualify for one layer of help. A California Hero may qualify for a more customized combination because occupation, county, city, and local housing priorities can all affect what's available.

The National Housing Conference notes that many state and local DPA programs are specifically targeted at certain occupations, and that program design has become more specialized. It also points out a common gap. Borrowers rarely get a clear explanation of how conventional DPA interacts with occupation-based benefits, county or city overlays, and local underwriting rules, as described in this policy overview on down payment assistance and homebuyer support.

In practice, that means a teacher and a firefighter shopping in different California counties may face very different program combinations even if their income and credit look similar.

What Heroes should look for first

Instead of searching for one magic program, start with eligibility buckets:

- Occupation-targeted help tied to public service roles.

- Local agency support based on county or city.

- First-time-buyer frameworks that can sometimes be paired with conventional financing.

- Assistance structure that fits your timeline, especially if you expect transfers, promotions, or future refinancing.

Local interpretation is key. The published rules are only part of the story. The primary work is figuring out what can be layered without breaking the underwriting file or delaying the closing.

A practical California approach

For California Heroes, the strongest plan is usually built around the first mortgage first, then matched to the most workable assistance rather than the most eye-catching headline. That means confirming property type, occupancy, reserves, and monthly payment tolerance before chasing every available program.

One option in this space is California Loans for Heroes, which works with homebuyer assistance and down payment assistance options for eligible public service professionals across California. What matters most is not the brand name. It's whether the lender or advisor can sort through profession-based benefits, local overlays, and conventional underwriting at the same time.

If that work isn't done upfront, buyers often end up with a pre-approval that looks fine until the assistance layer is added. That's when timelines slip.

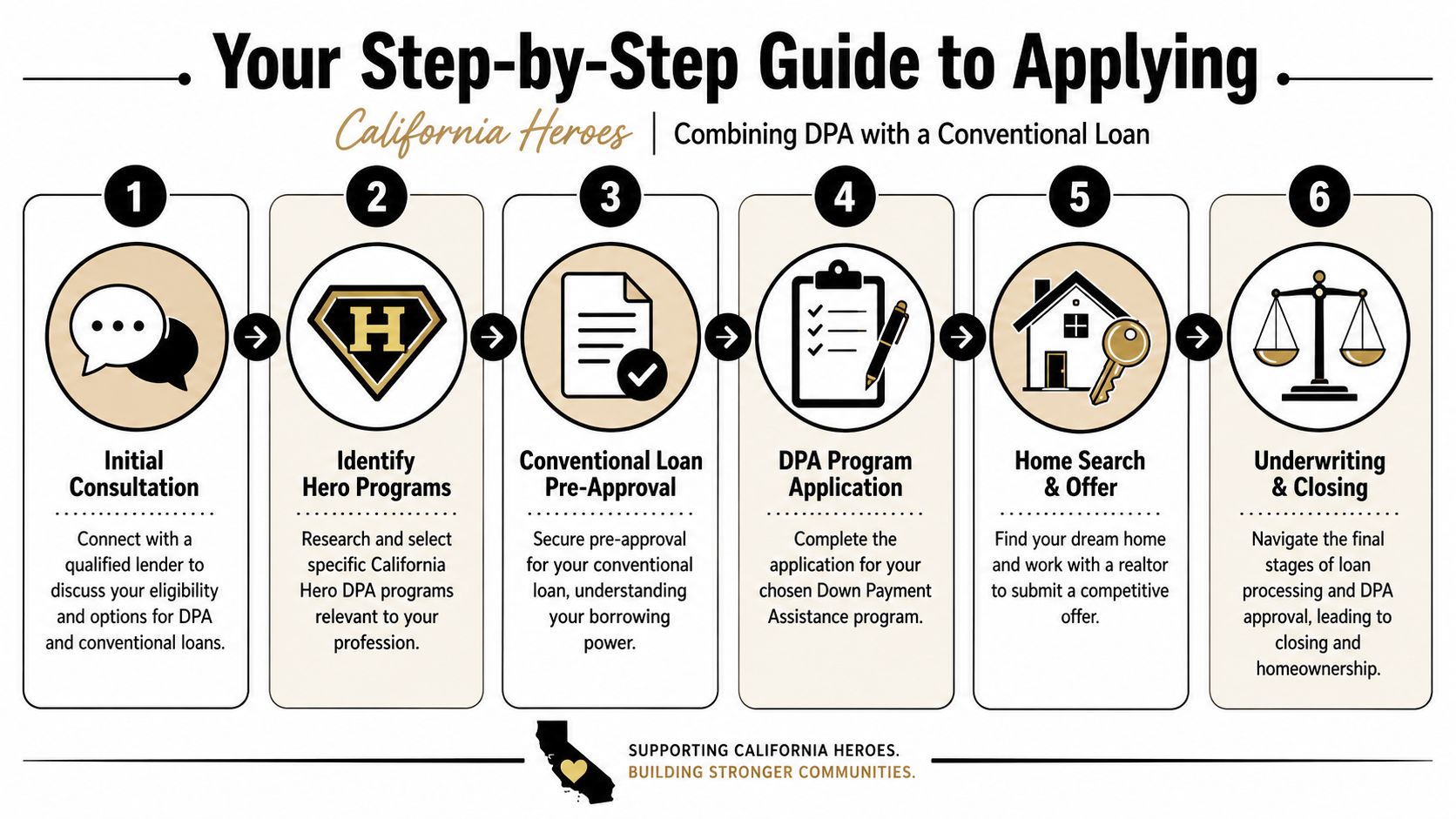

Your Step-by-Step Guide to Applying

A good application process reduces surprises. That matters because there are 2,600+ programs nationwide, and down payment programs make up 74% of all available programs, according to Down Payment Resource's program overview. Availability isn't the hard part. Fit is.

Start with pre-approval that includes the assistance strategy

Too many buyers get pre-approved for the first mortgage only. Then they try to bolt on assistance later. That's backward.

For a conventional loan with down payment assistance, your starting point should be a lender who looks at the full structure before you shop. If you're early in the process, this walkthrough on the steps to buying your first home is helpful for organizing the larger timeline.

The six steps that keep the file clean

Initial review

The lender reviews income, assets, credit, employment, and the likely first mortgage structure. During this review, realistic payment comfort should be discussed, not just maximum qualification.Program matching

The buyer's profession, location, occupancy plans, and available cash are used to narrow the DPA list. The right question is which program fits, not which one sounds biggest.Conventional pre-approval

The pre-approval should reflect the likely final structure, including any assistance that affects funds-to-close or underwriting treatment.Documentation gathering

DPA programs often need their own paperwork. Delays happen when buyers underestimate this step or submit incomplete files.Home search and offer strategy

Your agent and lender should know the transaction includes assistance. That helps set realistic timing and avoids contract terms that are too aggressive.Underwriting and closing coordination

The first mortgage and the DPA layer must move in sync. If one side is ready and the other isn't, the whole transaction can stall.

What makes applications go smoother

Some files are clean from the beginning because the borrower acts early on a few basics:

- Keep asset paper trails clear. Large undocumented deposits can create avoidable questions.

- Don't change jobs or major debts casually. Even a positive life change can complicate timing during escrow.

- Tell the lender if your schedule or profession affects documentation. Overtime, shift income, and specialty pay often need careful presentation.

- Plan for education or counseling requirements. Some assistance programs require them, and waiting too long can hold up closing.

Watch this closely: the best-fitting DPA program is the one you can actually close on within your contract timeline.

Avoiding Pitfalls and Taking Your Next Step

The biggest mistake buyers make is chasing upfront help without studying the terms underneath it. A conventional loan with down payment assistance can be a smart move, but the structure matters more than the label.

The mistakes that create regret later

Some problems show up immediately. Others don't appear until a year or two after closing.

- Focusing only on cash to close and ignoring the monthly payment.

- Choosing assistance without understanding repayment triggers tied to sale, refinance, or occupancy changes.

- Assuming all second liens behave the same way when they don't.

- Using a lender who can close the first mortgage but doesn't regularly coordinate DPA.

- Shopping too early with a generic pre-approval that doesn't reflect the actual layered financing plan.

A second common mistake is treating DPA as the answer by itself. It isn't. It's one tool inside a broader affordability strategy that also includes rate, PMI, property taxes, insurance, reserves, and future plans.

What tends to work better

The strongest buyers usually take a narrower, more disciplined path. They choose a home price that leaves room in the monthly budget. They compare the DPA structure, not just the amount. They ask what happens if they refinance. They make sure their lender has already checked compatibility before offers go out.

That approach is especially important for California Heroes because local pricing pressure can tempt buyers into stretching too far just to get in. A better outcome is buying with a structure you can live with comfortably.

If you're a teacher, nurse, firefighter, law enforcement officer, veteran, service member, or other public service professional in California, the next practical step is a personalized review of your conventional options, your likely assistance matches, and the tradeoffs attached to each one.

If you want that kind of review, connect with California Loans for Heroes to discuss your profession, location, available funds, and whether a conventional loan with down payment assistance fits your plan. A focused conversation can quickly tell you whether you should move now, adjust the structure, or wait for a better combination.