You work hard in California, you serve other people, and you still look at home prices and think, “How am I supposed to come up with all that cash?”

This is true for a lot of nurses, teachers, firefighters, police officers, veterans, and other public service professionals. The monthly payment may look manageable. The upfront money is what stops the deal before it starts.

That's exactly why down payment assistance matters.

If you're asking how much does down payment assistance cover, the short answer is this: it can cover a meaningful part of your upfront costs, and sometimes it can cover most of the minimum cash needed to buy. But the specific answer depends on the program, the loan type, and whether the assistance can be used only for the down payment or also for closing costs.

Your Path to Homeownership in California

A lot of first-time buyers in California hit the same wall.

You find a home price that feels barely within reach. You run the mortgage estimate. You adjust expectations. Then the cash-to-close number shows up and everything changes. Suddenly you're not just thinking about the house. You're thinking about savings, emergency reserves, rent due before closing, and whether buying now is even realistic.

That's especially common for California heroes. You may have stable income, strong work history, and a career built on service, but that doesn't automatically create a large savings account.

Why the upfront cash feels so hard

The biggest mistake buyers make is assuming they need to solve the whole problem alone.

They think the down payment has to come entirely from personal savings. In reality, many buyers use a mix of tools, including assistance programs, family support, and structured mortgage options. LendingTree found that 40% of homeowners received some form of financial help in 2023, up from 35% in 2022, and 16% of all homeowners received a portion of their down payment help from parents. That rises to 27% among Gen Z homeowners and 26% among parents of young children. Half of homeowners who got help said at least 40% of their total down payment came from that assistance, according to LendingTree's survey on down payment help.

What this means for you

You don't need perfect savings to buy. You need a workable strategy.

Practical rule: Stop asking whether you can save everything yourself. Start asking what assistance you qualify for, what costs it can cover, and how little you may actually need to bring from your own account.

That shift is what gets people into homes.

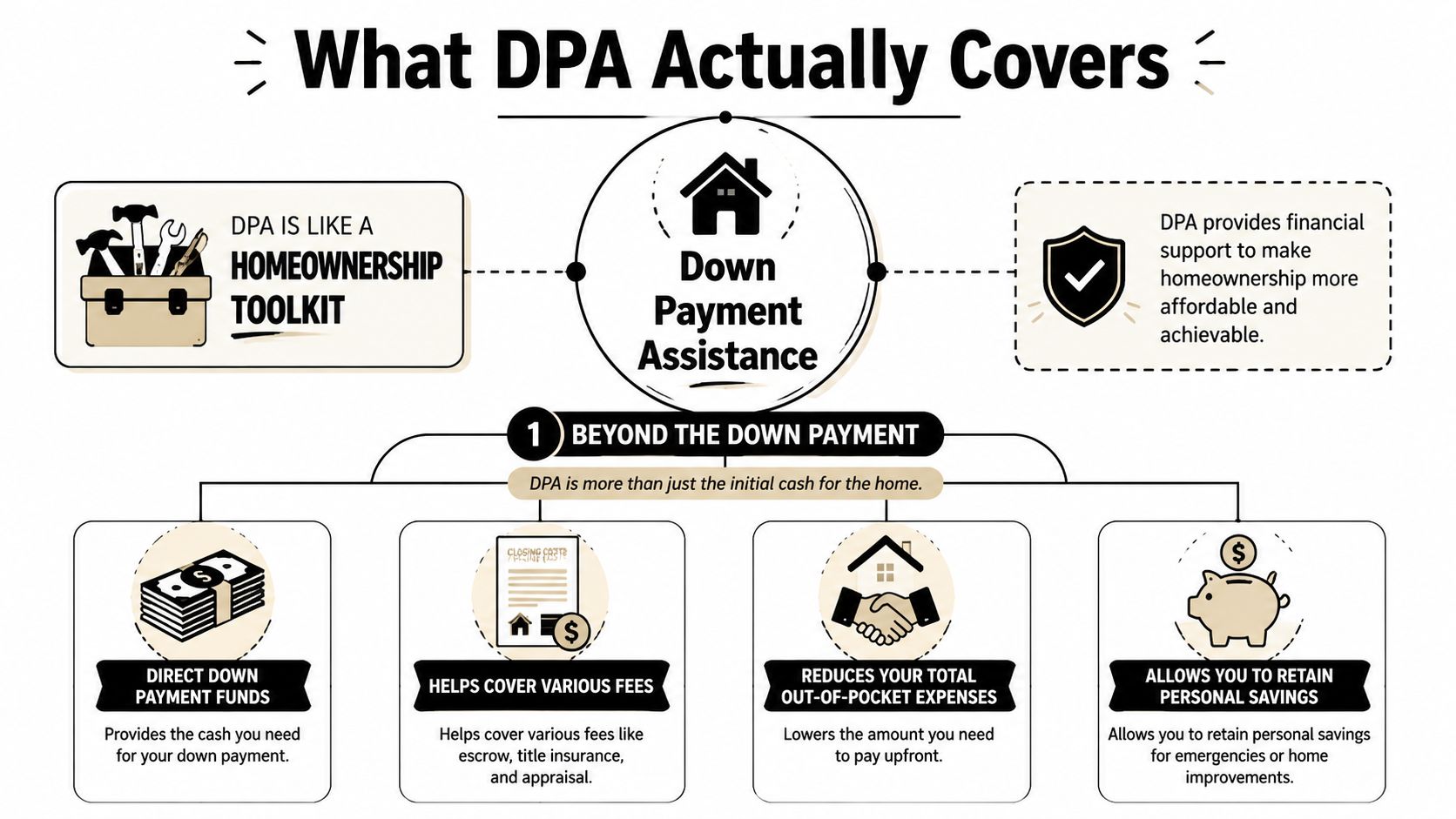

What Down Payment Assistance Actually Covers

Most buyers hear “down payment assistance” and assume it covers one thing only. That's too narrow.

Think of DPA as a homebuying toolkit, not just a check for one line item. Some programs only help with the down payment. Many others can also help with closing costs, prepaid expenses, or even rate-related costs that reduce the pressure on your cash at closing.

The better question to ask

Instead of asking only, “How much do I get?”

Ask this: What can I use it for?

That's the smarter question because the same assistance amount can stretch much further when program rules allow more flexibility. Down Payment Resource notes that some programs are limited to the down payment, while many can also be applied to closing costs, prepaid expenses, or even rate buydowns, which gives the same dollar amount very different real-world value in high-cost markets like California. That point comes from Down Payment Resource's explanation of what lenders get wrong about DPA.

What costs may be covered

Here's how I explain it to first-time buyers.

- Down payment funds: This is the obvious one. Assistance may help you meet the minimum required investment to get the loan.

- Closing costs: Depending on the program, funds may go toward the fees tied to finalizing the purchase.

- Prepaid housing expenses: Some programs also allow funds to help with items paid upfront at closing.

- Cash preservation: Even when the assistance doesn't wipe out every cost, it can let you keep more of your own savings for repairs, moving, and emergencies.

That last point matters more than people realize. Buying a home with every dollar drained out of your account is not a smart win.

A buyer with a smaller personal contribution and healthy reserves is often in a stronger position than a buyer who empties savings just to say they brought more cash.

If you're comparing assistance options with military benefits or veteran-specific support, it also helps to understand how these costs interact. A good starting point is this guide to closing cost assistance for veterans.

Why this matters in California

In California, purchase prices can make even a low-down-payment loan feel expensive upfront. That's why flexibility matters.

A program that covers only one piece of the puzzle may still help. A program that can be applied across multiple upfront costs can change the deal completely. Don't judge DPA by the headline number alone. Judge it by what line items it removes from your cash-to-close.

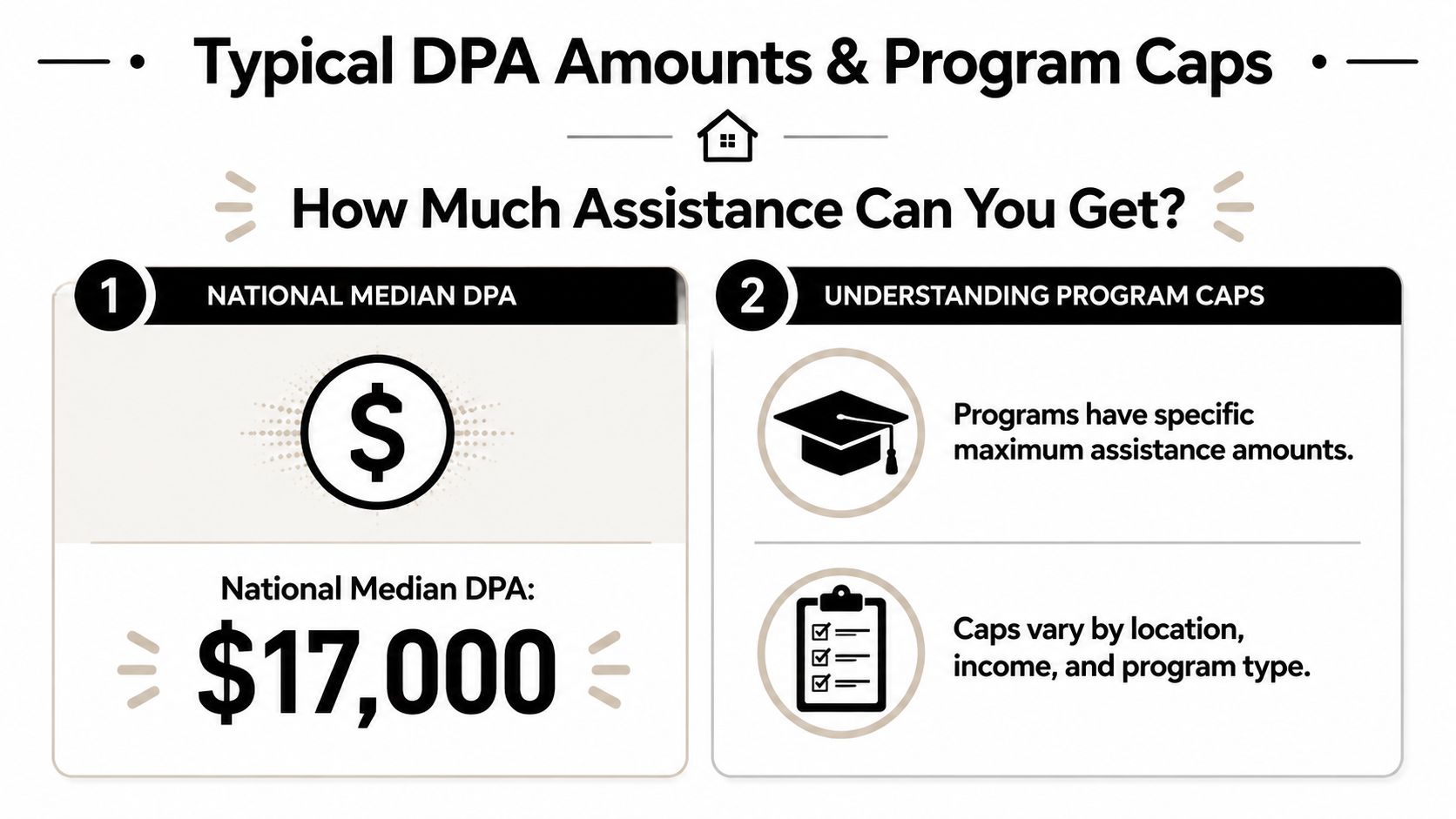

Typical DPA Amounts and Program Caps

Now for the direct answer.

If you want to know how much down payment assistance covers, start with this benchmark: the median contribution from DPA programs reached $16,862 in 2023, according to Urban Institute's review of expanding down payment assistance awareness.

That's a real number. It's also only a starting point.

What buyers typically see

Most DPA programs don't function like an unlimited subsidy. They usually follow one of a few structures:

- Fixed-dollar assistance: 60.7% of DPA programs contributed a fixed dollar amount in 2022, with a median of $15,000.

- Percentage of sales price: 22.1% of programs covered a percentage of the sales price, with a median of 10%.

- Percentage of loan amount: 9.5% of programs covered a percentage of the loan amount, with a median of 5%.

That structure matters. Fixed-dollar programs are common, which means your benefit often has a cap built in from the start.

Why buyers get confused

A lot of people hear that assistance exists and assume it will cover whatever shortfall they have. That's not how most programs work.

The amount is usually tied to a formula, a maximum, or a program design. If your market is expensive, a fixed-dollar benefit may still help a lot, but it might not cover every upfront cost. It's meant to bridge the gap, not erase every dollar you need.

Rising home prices changed the stakes

Urban Institute also shows why this feels more urgent now. The median contribution from programs rose from $10,400 in 2010 to $16,862 in 2023, while the 5% down payment required for the median home purchase increased from $10,400 in 2010 to $22,240 in 2023. Assistance amounts have increased, but so has the cost of getting into a home.

Bottom line: DPA is stronger than it used to be in dollar terms, but California buyers still need to pay close attention to caps, loan structure, and what costs the program actually allows.

Real-world examples of caps

National medians are helpful, but buyers need concrete examples.

Some programs provide a percentage of the first mortgage amount or purchase price. Others set a hard ceiling. Here are a few examples from program guidance collected by Here to Home:

| Program example | How coverage is structured |

|---|---|

| Washington Home Advantage | 3%, 4%, or 5% of the first-mortgage loan amount |

| Bellingham program | Up to $40,000 in assistance, with a borrower contribution still required |

| Maryland MMP | Can match partner assistance up to $2,500 |

| Texas programs | Commonly range from $2,000 to $30,000 or up to 5% of the loan amount |

These examples come from Here to Home's overview of down payment assistance structures.

The lesson is simple. Expect a real benefit, not a blank check.

The Three Main Types of DPA Programs

The amount matters. The terms matter just as much.

Misconceptions arise for buyers. They hear “assistance” and assume “free money.” Sometimes it is. Often it isn't. The structure determines whether you keep the full benefit with no strings attached or repay it later.

Grants

A grant is the cleanest version of assistance.

You receive funds that help you buy, and there's no repayment requirement if the program is a true grant. That's the easiest type to understand and the easiest one to like. The catch is that grant-style programs are less common than buyers think.

Forgivable loans

A forgivable loan is not automatically free money on day one. It becomes free if you meet the program's conditions.

Those conditions often involve staying in the home for a required period or meeting occupancy rules. If you sell, refinance, or move too early, part or all of the assistance may need to be repaid. This can still be a strong option. You just need to know the timeline before you commit.

Deferred-payment loans

This is the version many California buyers will run into.

A deferred loan usually doesn't require monthly payments right away, but repayment is delayed until a later event, often when you sell, refinance, or pay off the first mortgage. This can help you buy now without increasing your monthly pressure, but it still creates a lien that matters later.

The Philadelphia Fed notes that DPA can be structured as a grant, forgivable loan, deferred loan, low-interest second mortgage, or shared-appreciation loan, and that nearly 90% of DPA is structured as a second mortgage. The same source also notes that some programs require repayment only upon sale, while others are forgiven over time, and found no statistical or substantive difference in mortgage performance between borrowers with and without DPA in the research discussed by the Philadelphia Fed's spotlight on down payment assistance.

Down Payment Assistance Types Compared

| DPA Type | What It Is | Repayment Required? | Best For |

|---|---|---|---|

| Grant | Funds provided without a loan structure | Usually no | Buyers who qualify for limited grant programs and want the simplest option |

| Forgivable loan | Assistance that is forgiven if you meet program rules | Sometimes, if you don't meet conditions | Buyers who plan to stay put and can follow occupancy rules |

| Deferred loan | Assistance repaid later, often at sale or refinance | Yes, typically later rather than monthly | Buyers who need upfront help now and expect future equity or refinance options |

My advice as a loan advisor

Don't choose based on the biggest advertised number.

Choose based on net benefit after terms. A smaller amount with clean forgiveness may beat a larger amount that has repayment hooks you don't understand. If you don't ask when repayment happens, you're not really comparing programs.

Ask two questions every time: “Is this a grant or a lien?” and “What event triggers repayment?”

That will save you from surprises later.

California DPA Programs for Heroes and First-Time Buyers

California buyers need California answers.

Generic national articles don't help much when you're trying to buy in a state where price pressure is high and local programs matter. If you're a teacher, nurse, firefighter, law enforcement officer, veteran, or other public service professional, the practical move is to look at programs that work inside California's lending framework first.

CalHFA MyHome is the clearest example

For first-time buyers in California, CalHFA MyHome is one of the most useful programs to understand because it gives you a concrete coverage model.

According to CalHFA's MyHome program details, the program offers a deferred-payment junior loan of up to 3.5% of the purchase price or appraised value for FHA loans and up to 3% for conventional loans. CalHFA states that this assistance is designed to help meet minimum down payment and/or closing cost requirements.

That matters because it lines up directly with the pain point most first-time buyers have. Not monthly affordability. Upfront cash.

Why this works well for hero professions

Many California hero buyers have solid employment, predictable income, and a clear long-term reason to stay in the area. What they don't always have is a huge liquid reserve.

That's where California-focused planning helps. A deferred junior loan can make sense if it gets you into a home sooner without adding immediate monthly strain. For many buyers, that's a better move than waiting years to build a larger cash cushion while prices and rents continue to move around them.

Local guidance matters more than broad advice

Statewide and local programs can differ on income rules, first-time-buyer definitions, property limits, occupancy requirements, and whether funds can be layered. You don't want to guess your way through that.

If you want to look at hero-focused options in one place, review the available California down payment assistance programs for heroes. California Loans for Heroes works with buyers in professions such as military, veterans, first responders, healthcare, education, and public service, and that kind of niche focus is useful when your eligibility may depend on both profession and loan structure.

My recommendation for California buyers

Start with the state-specific programs first. Then compare them against any city, county, employer, or profession-based options that may apply to you.

Use this priority order:

- Check CalHFA-type statewide options that match your loan program.

- Look for local or profession-based programs tied to your county, city, or occupation.

- Ask whether assistance can be layered with other eligible benefits.

- Confirm whether the funds are deferred, forgivable, or grant-based before you rely on them.

That's how you turn “maybe I can buy” into an actual plan.

How Your Mortgage Type Affects DPA Coverage

Your first mortgage changes how useful DPA becomes.

The same assistance amount can solve very different problems depending on whether you're using an FHA loan, a conventional loan, or a VA loan. In these situations, strategy proves superior to guesswork.

FHA buyers

FHA is often a strong fit for first-time buyers who need a lower upfront requirement and flexible qualification.

If your DPA program is designed to work with FHA, the assistance may cover most or all of the minimum borrower investment, depending on the program terms. That can dramatically reduce the money you need at closing. It's one of the most practical combinations for buyers who have income but limited savings.

Conventional buyers

Conventional financing can pair well with assistance too, but the coverage amount may be structured differently than with FHA.

Some programs cap assistance at a percentage level that works better with one loan type than another. If you're considering this route, compare the first mortgage and DPA side by side instead of treating them as separate decisions. This guide on a conventional loan with down payment assistance is useful if that's the lane you're exploring.

VA buyers and California heroes

If you're eligible for VA financing, your issue usually isn't the down payment itself. It's the other cash needed to close.

That's why DPA can still matter for veterans and active-duty buyers. It may help with closing costs or other eligible upfront items, depending on the program. In the right setup, that can sharply reduce what you need out of pocket even when the first mortgage doesn't require a down payment.

The smartest DPA strategy isn't always “cover my down payment.” Sometimes it's “reduce my total cash-to-close as much as possible.”

One caution that matters

Some buyers assume assistance means they can bring nothing at all. That's not always true.

Here to Home highlights that some programs still require the borrower to contribute $2,500 or 1% of the purchase price, whichever is greater, even when the program offers up to $40,000 in assistance. That borrower contribution requirement is common because programs want you to have some skin in the game, as noted in the earlier Here to Home source.

So don't build your plan around zero unless your lender confirms it in writing. Build your plan around the lowest realistic cash contribution for your exact loan and assistance combo.

Your Next Steps to Secure Down Payment Assistance

If you've made it this far, here's the simple takeaway.

Down payment assistance can cover a meaningful share of your upfront costs, but the headline amount is only part of the story. You need to know what the funds can be used for, whether the assistance is a grant or a second lien, and how your mortgage type changes the result.

For California heroes, this matters even more. State programs, local options, and profession-based eligibility can create opportunities that broad national articles miss.

Do this next:

- Get your loan type narrowed down first. FHA, conventional, and VA each interact with DPA differently.

- Ask for a true cash-to-close breakdown. Don't settle for a vague estimate.

- Review repayment terms line by line. “Assistance” and “free” are not the same thing.

- Focus on California-specific options. They're often the most relevant to your actual purchase.

You do not need to figure this out alone, and you shouldn't try to piece it together from generic advice. A personalized review is the fastest way to see what you may qualify for and what your real out-of-pocket number could look like.

If you're a veteran, nurse, teacher, firefighter, first responder, law enforcement officer, or other California public service professional, California Loans for Heroes can help you review your loan options, identify down payment assistance programs that may fit your situation, and build a practical homebuying plan with no-obligation guidance.