Owning a home in California can feel out of reach even when you've done everything right. You work long shifts, serve your community, keep your finances in order, and still find yourself wondering how anyone comes up with enough cash to buy in this market.

That tension is especially real for California's HERO community. First responders, military families, teachers, nurses, and other public service professionals often have stable careers and strong motivation to put down roots, but the upfront cost of buying is where the plan gets stuck. The good news is that California first time home buyer assistance is built for exactly that gap. These programs can reduce cash needed at closing, make financing more workable, and open doors that many buyers assume are closed.

Your Path to Homeownership in the Golden State

California asks a lot from first-time buyers. A Bankrate overview of California home buyer programs reported a $784,900 median home price in January 2025, while also noting that some Los Angeles County programs can provide up to 20% of the purchase price and some San Diego programs can offer deferred-payment loans up to 19% plus up to $10,000 for closing costs. That matters because most buyers don't fail on monthly payment alone. They fail on cash to close.

For HERO buyers, the emotional side matters too. Stability isn't just a financial goal. It's the ability to stop moving from rental to rental, keep your kids in the same school, cut commute stress, and build something long-term in the state you serve.

Why assistance matters more than most buyers realize

Many people hear “assistance” and think small grant, long odds, or too many strings attached. In practice, California's homebuyer programs can be meaningful enough to change which homes are realistic and when you can buy.

That's why I tell HERO clients to stop treating assistance as a backup plan. Treat it as part of the financing strategy from day one.

Practical rule: If lack of down payment is the main obstacle, the right assistance program can matter as much as the interest rate.

What this means for HERO professionals

California first time home buyer assistance can be especially useful for buyers with strong employment history but limited liquid savings. That profile is common among public service households. Overtime can vary. Transfers happen. Family needs compete with savings goals. None of that means homeownership is off the table.

A smarter approach looks like this:

- Start with affordability, not listings. Get clear on the full structure of the deal, including first mortgage, assistance layer, occupancy rules, and repayment terms.

- Match the program to your career reality. Veterans, active-duty households, teachers, and first responders often need flexibility around timing, documentation, and prior housing history.

- Work the plan early. Assistance programs don't work well when they're added at the last minute.

The buyers who do best usually aren't the ones with perfect circumstances. They're the ones who understand the options early and move with a clear process.

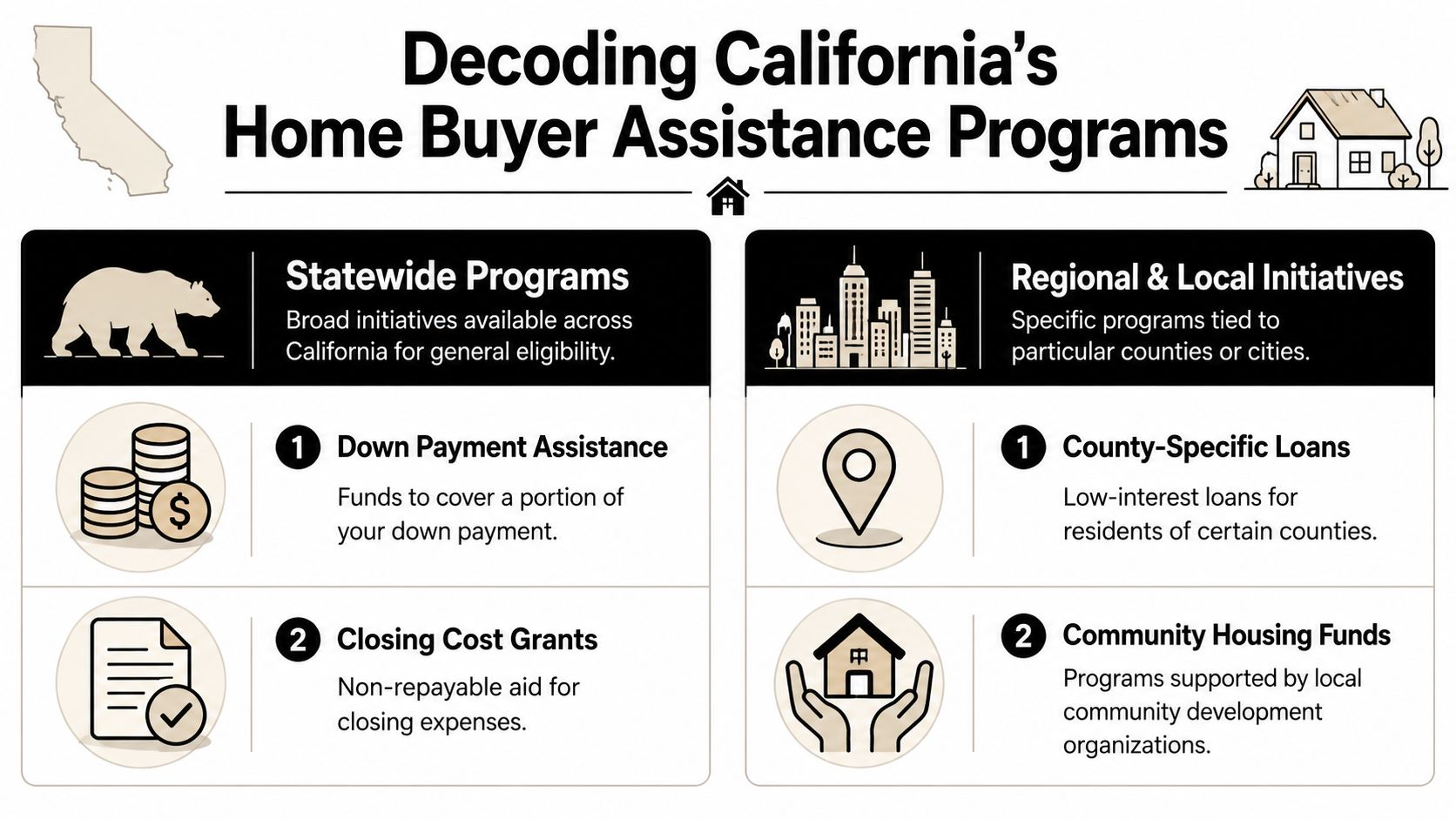

Decoding California's Assistance Programs

California's assistance options make more sense when you split them into two buckets. First, there are statewide programs, mainly through CalHFA. Second, there are local programs tied to a county, city, or housing authority. Think of statewide programs as the broad toolkit and local programs as specialized tools built for a specific area.

Statewide options and local options work differently

Statewide assistance is usually easier to recognize because the program names show up in mortgage conversations across California. These programs often pair with common first mortgages and follow a more standardized approval path.

Local programs are more specific. They can be powerful, but they come with geographic rules, local income rules, property rules, and their own funding timelines. In some counties, local assistance can be much more aggressive on upfront help than buyers expect.

If you're comparing structures, this simple view helps:

| Program type | Typical role in the deal | Best use case |

|---|---|---|

| Statewide program | Adds a more standardized assistance layer behind the first mortgage | Buyers who want broader availability and a familiar process |

| Local program | Targets a county or city with area-specific benefits | Buyers purchasing in a location with stronger local support |

Assistance is not all the same money

A lot of buyers use “down payment assistance” as a catch-all term. That's where confusion starts. The money can come in different forms, and the structure matters as much as the amount.

Common forms include:

- Deferred-payment second mortgages. These reduce cash needed today and usually don't require monthly payments while you own the home.

- Closing-cost help. This can ease one of the most underestimated parts of the transaction.

- Shared-equity loans. These can lower the upfront barrier sharply, but they change what happens later when you sell.

Los Angeles County's HOP80 and HOP120 programs show the tradeoff clearly. The Los Angeles County homeownership program page explains that these programs can provide up to 20% of the purchase price as a zero-interest deferred loan with a shared-equity component. That structure helps with upfront affordability, but the program shares in future appreciation when the property is sold.

Low payment today can mean less equity in your pocket later. That isn't good or bad by itself. It's a planning decision.

What works and what doesn't

What works is choosing assistance based on your expected time in the home, your cash reserves, and your career path. If you expect to stay put and need help getting in, a deeper assistance structure may make sense. If you want maximum future equity and already have enough funds to close, a lighter-touch option may fit better.

What doesn't work is treating all programs as interchangeable. They aren't. If you're looking at a conventional loan with down payment assistance, the right question isn't just “How much help do I get?” It's “What does this help cost me later, and does that tradeoff fit my plan?”

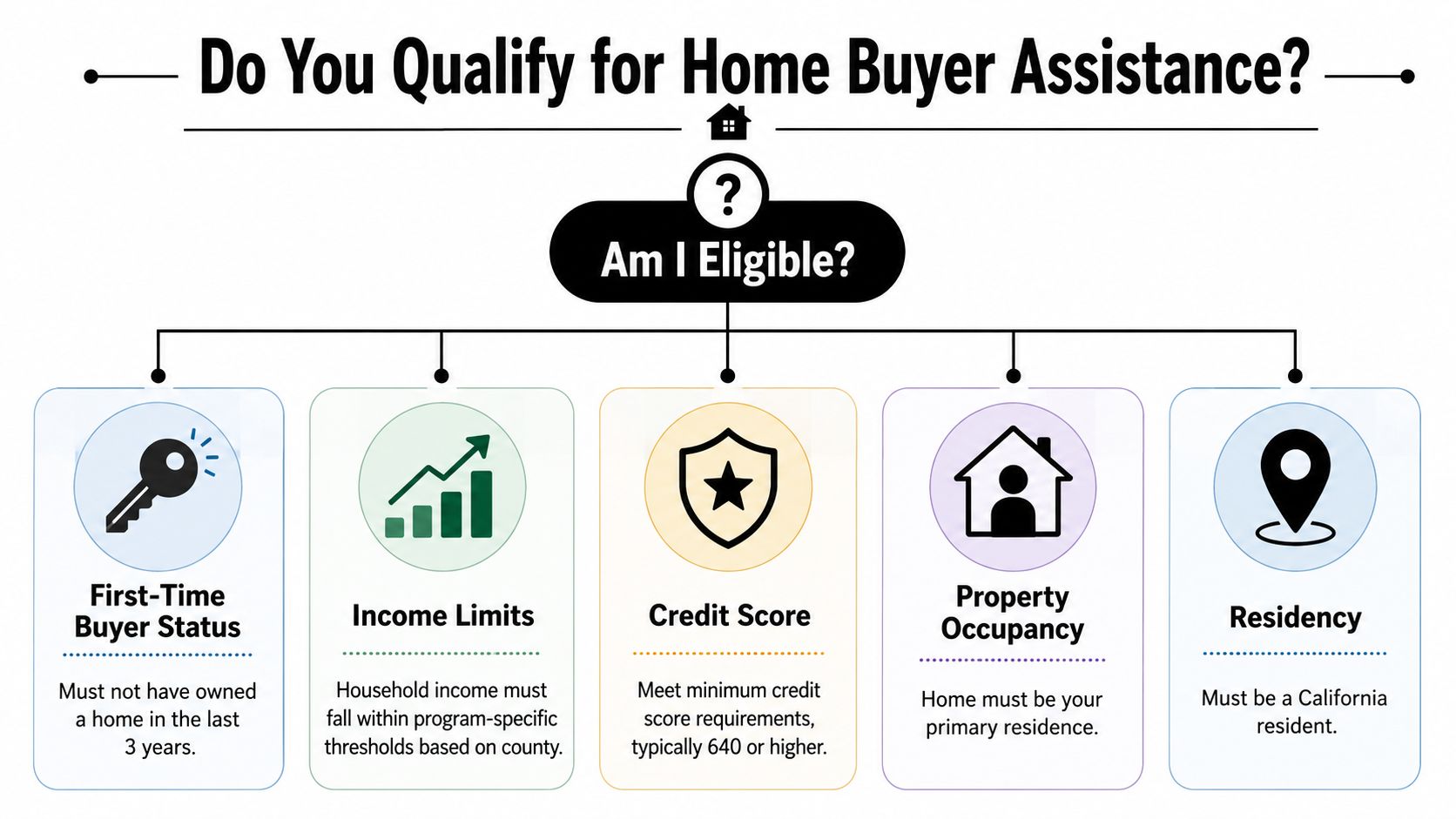

Do You Qualify for Home Buyer Assistance

Eligibility is where buyers either get momentum or talk themselves out of moving forward. Most assume they earn too much, waited too long, or don't count as first-time buyers anymore. In reality, many California assistance programs are aimed at moderate-income households, not only lower-income households.

A CalMatters review of California homebuyer assistance noted that participation was often limited to households earning less than 150% of area median income in their county, and the average first-time homebuyer loan was $112,000. That tells you two important things. First, the programs are substantial. Second, they're not designed only for the very lowest earners.

The checklist that matters most

Buyers usually need to look at qualification in layers, not as one yes-or-no question.

- Buyer status. Some programs treat you as a first-time buyer if you haven't owned and occupied a home within the prior 3 years, as noted in the earlier Bankrate reference.

- Income fit. The key is your county's income limit, not a statewide guess.

- Occupancy. These programs are built for primary residences, not investment property.

- Mortgage compatibility. The first loan and the assistance layer have to work together.

- Documentation. Income, assets, employment, and residency all have to line up clearly on paper.

Why HERO buyers misread eligibility

Public service households often have more moving parts than standard online checklists account for. Military relocation, overtime income, shift differentials, temporary duty assignments, and employment transitions can make buyers think their file is too unusual. Often, it just means the file needs to be reviewed by someone who understands how to present it properly.

Here's a practical perspective:

| Question | Better way to look at it |

|---|---|

| “Do I make too much?” | Compare your household income to the county program cap |

| “I owned before, so I'm out” | Check whether the program uses a lookback rule rather than a lifetime ban |

| “My income varies” | Variable income isn't automatic disqualification. It needs clean analysis |

| “I'm buying with special financing” | Many assistance programs can be layered with standard mortgage products |

Quick filter: If you're buying a primary residence, have stable income, and haven't ruled yourself out based on assumptions alone, it's worth getting screened.

The biggest mistake is self-denial. Many eligible buyers never apply because they rely on outdated definitions or generic advice that doesn't reflect California's actual program rules.

Special Home Loan Options for California HEROES

Generic homebuyer articles usually stop at “check CalHFA and your local city program.” That's not enough for HERO households. Veterans, active-duty buyers, teachers, first responders, nurses, and public employees often qualify for combinations and exceptions that broad consumer guides barely mention.

Where HERO buyers gain an edge

Some of the strongest opportunities come from layering mainstream financing with assistance instead of viewing them as separate lanes. As noted earlier in the article, California assistance can pair with common mortgage options, including conventional, FHA, VA, and USDA structures.

For HERO buyers, that creates a practical advantage:

- Veterans and active-duty buyers may be able to combine a VA-friendly approach with assistance planning.

- Teachers and healthcare professionals often have reliable employment profiles that support structured approval.

- First responders and law enforcement officers may benefit from planning around schedule complexity and income documentation early.

- Public service employees often fit the moderate-income profile that these programs were built to serve.

One practical option in this space is California home loans for heroes, which is focused on financing paths for public service professionals and can be evaluated alongside other statewide and local assistance routes.

The Dream For All misunderstanding that trips people up

A major area of confusion for HERO buyers is the relaunched CalHFA Dream For All program. The issue isn't only whether someone wants the program. It's whether they mistakenly assume they don't qualify.

A video discussing CalHFA Dream For All eligibility for HERO buyers notes that the program can offer up to 20% of the purchase price, capped at $150,000, and that the strict “first-generation” definition can confuse veterans and public servants. Some people who previously owned a home but lost it because of service-related relocation or similar circumstances may incorrectly assume they're disqualified.

That matters because HERO families often have housing histories that don't fit the neat examples shown in mainstream articles.

What to ask before you rule yourself out

Don't make a snap decision based on one phrase in a headline. Ask questions that fit your actual history.

- Have you owned recently, or are you relying on old assumptions? Time and program definitions matter.

- Was a prior home lost or left because of service obligations? That history deserves a closer review.

- Are your parents' ownership circumstances relevant to the specific program? For first-generation programs, family history may matter in ways buyers don't expect.

- Are you mixing up VA eligibility with assistance eligibility? They're different tests.

A lot of HERO buyers aren't denied by the program. They deny themselves before anyone reviews the file.

That's why specialized guidance matters. The California first time home buyer assistance world is complicated enough on its own. Add military service, transfer history, or public-sector income structure, and details become decisive.

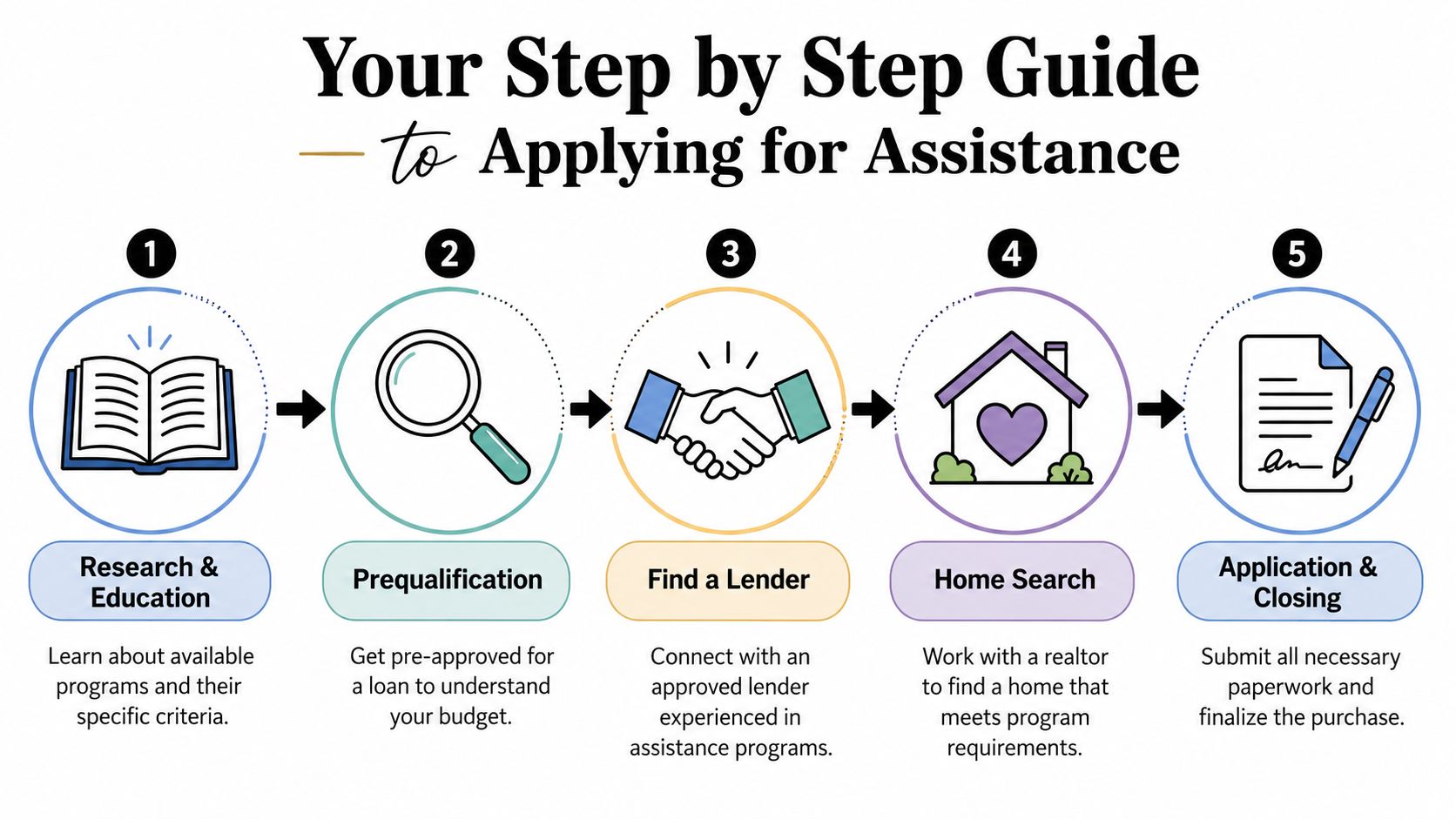

Your Step by Step Guide to Applying for Assistance

The application process feels heavy when buyers think of it as one giant approval. It goes better when you treat it as a sequence. Each step solves one problem, and each solved problem makes the next one easier.

The sequence that keeps deals on track

Get your financing picture organized first.

Before looking seriously at homes, gather income documents, asset statements, and employment details. With these steps, assistance planning begins, not ends.Get preapproved with a lender who understands layered financing.

A basic preapproval isn't enough if the lender doesn't know how the assistance piece interacts with the first mortgage. You want a realistic buying range, not an optimistic one.Confirm program fit before writing offers.

This includes buyer status, occupancy intent, area limits, property type, and timing. A home can be a great house and still be a poor fit for the program structure.Complete required education if the program calls for it.

Some assistance paths include a homebuyer education requirement. Finish it early so it doesn't become a closing-condition surprise.Coordinate the first mortgage and the assistance loan together.

The two pieces should move in sync. If one side is late, the whole transaction feels it.

Documents that usually deserve extra attention

Certain documents cause repeated slowdowns, especially for HERO households:

- Income records with variable pay. Overtime, differentials, and nonstandard schedules need clean review.

- Bank statements. Large deposits can trigger questions that are easier to answer early.

- Housing history. If a prior ownership situation is relevant, document it clearly.

- Service-related paperwork. Military or public service transitions may explain issues that don't make sense on a standard checklist.

A useful early resource is this guide on how to get down payment assistance, especially if you're trying to understand how the funding layer fits into a standard purchase timeline.

What buyers can control

You can't control underwriting speed or local program availability. You can control readiness.

| What helps | What causes delays |

|---|---|

| Complete documents upfront | Missing pages and outdated statements |

| Early eligibility review | Waiting until you're already in escrow |

| Clear explanation of special circumstances | Assuming underwriters will “figure it out” |

| Program-aware preapproval | Generic preapproval with no assistance planning |

Field note: The smoothest assistance closings usually come from buyers who choose their financing path before they fall in love with a specific house.

That approach doesn't remove the work. It removes avoidable friction.

Common Pitfalls and How to Avoid Them

Most failed assistance strategies don't fail because the buyer was unqualified. They fail because the buyer used the wrong process. The most common problem is waiting too long to match the assistance program to the first mortgage and purchase timeline.

Another major issue is misunderstanding repayment. The CalHFA MyHome program page explains that MyHome can provide up to 3.5% of the purchase price or appraised value for FHA loans and up to 3% for conventional, VA, or USDA loans, and that it is a deferred-payment second mortgage repaid when the home is sold, refinanced, or the primary mortgage is paid off. Buyers like the no-monthly-payment feature, but some don't fully absorb the repayment trigger until much later.

The mistakes I see most often

- Choosing a lender who treats assistance as an add-on. Assistance isn't decoration on the file. It changes structure, timing, and documentation.

- Shopping for homes before running eligibility. That creates emotional pressure and rushed decision-making.

- Assuming deferred means forgiven. Deferred payment usually means postponed repayment, not free money.

- Ignoring the exit strategy. Refinance plans, likely move timelines, and future equity goals should shape which assistance structure you choose.

Better habits for a cleaner transaction

A stronger approach is simple:

- Ask how repayment works in plain language. If you sell, refinance, or keep the property long term, you should already know what happens.

- Review the second-lien terms before making offers. Don't wait until closing disclosures to understand the assistance.

- Build your team around program knowledge. The lender, agent, and buyer need the same plan.

- Leave room in the timeline. Assistance transactions often require more coordination than a plain vanilla purchase.

The biggest misconception is that the best program is the one with the biggest headline benefit. Often, the best program is the one you can execute cleanly and still feel good about years later.

Take the Next Step Toward Your California Home

California homeownership is hard. That part is real. But difficult doesn't mean impossible, and it definitely doesn't mean you have to solve the down payment challenge alone.

For HERO buyers, the right path usually isn't random house hunting or generic mortgage advice. It's a financing strategy built around your job, your timeline, your prior housing history, and the assistance programs that fit your file. Some buyers need statewide support. Others do better with a local program. Some need to think carefully about shared equity. Others need to revisit whether they're more eligible than they thought.

What matters most right now

If you take one thing from this guide, let it be this: California first time home buyer assistance works best when you plan around it early. Not after you find a house. Not after you've been told no somewhere else. Early.

A practical next step looks like this:

- Check your buyer status carefully. Don't rely on assumptions from years ago.

- Review your county and program fit. Moderate-income buyers often belong in this conversation.

- Choose a lender who understands layered financing. That decision affects everything that follows.

- Think beyond the closing table. The right assistance plan should still make sense when life changes later.

Homeownership in California still rewards preparation. HERO households already know how to work under pressure, follow a process, and stay focused on the mission. Buying a home is different from your day job, but the mindset is the same. Get the right information, use the right team, and move with a plan.

If you want help evaluating your options, California Loans for Heroes works with California veterans, military families, first responders, teachers, healthcare professionals, and other public service buyers to review home loan paths and assistance scenarios based on your situation. A personalized consultation can help you identify which programs fit, where the tradeoffs are, and what to do next.