You found a home you can picture yourself in. Maybe you're a firefighter coming off shift, a teacher scrolling listings after school, a nurse checking your phone between long days, or a veteran finally ready to buy in California. Then the offer paperwork lands in front of you and one phrase jumps out: good faith deposit.

That moment throws a lot of buyers off. You may wonder whether it's a fee, whether it's refundable, whether the seller gets your money right away, or whether putting down too little hurts your offer. Those are smart questions, especially if you're trying to buy with a VA loan, FHA financing, or a homebuyer assistance program where cash on hand matters.

The good news is that this part of the process is far less mysterious once you break it into pieces. If you're early in the journey, this guide to the steps to buying your first home in California helps put the deposit into the bigger picture. For now, the short version is simple: a good faith deposit is one of the first ways you show a seller you're serious, but it should also be handled in a way that protects you.

Your First Step Toward California Homeownership

A lot of California buyers first hear about a good faith deposit at the exact moment they feel pressure to move fast. The house is right. The neighborhood works. The payment looks manageable. Then your agent says the seller will expect a deposit with the offer or right after acceptance.

That can feel risky when you're already budgeting for appraisal fees, inspections, closing costs, moving expenses, and the normal surprises that show up during escrow. HERO buyers often feel that tension even more. Many have strong income, stable employment, and solid loan options, but they don't want to drain savings just to make an offer look stronger on paper.

Buying a home isn't just about getting accepted. It's about getting accepted without taking unnecessary risk.

In California, that balance matters. A deposit can help your offer stand out, but the number itself isn't the whole story. The contract terms, your financing, your timelines, and your contingency protections all matter too.

Why buyers get nervous about this step

Individuals aren't concerned about writing a deposit because they don't want the house. They're worried because they don't fully know:

- Where the money goes: Many buyers assume the seller receives it immediately.

- What happens if the deal falls apart: They want to know when they can get it back.

- How much is enough: Too low may weaken the offer, but too high can strain cash reserves.

- Whether loan type changes the strategy: VA, FHA, and assistance-backed buyers often need to preserve liquidity.

If that's where you are, you're not behind. You're doing what careful buyers do. You're asking the right questions before signing something that affects your money.

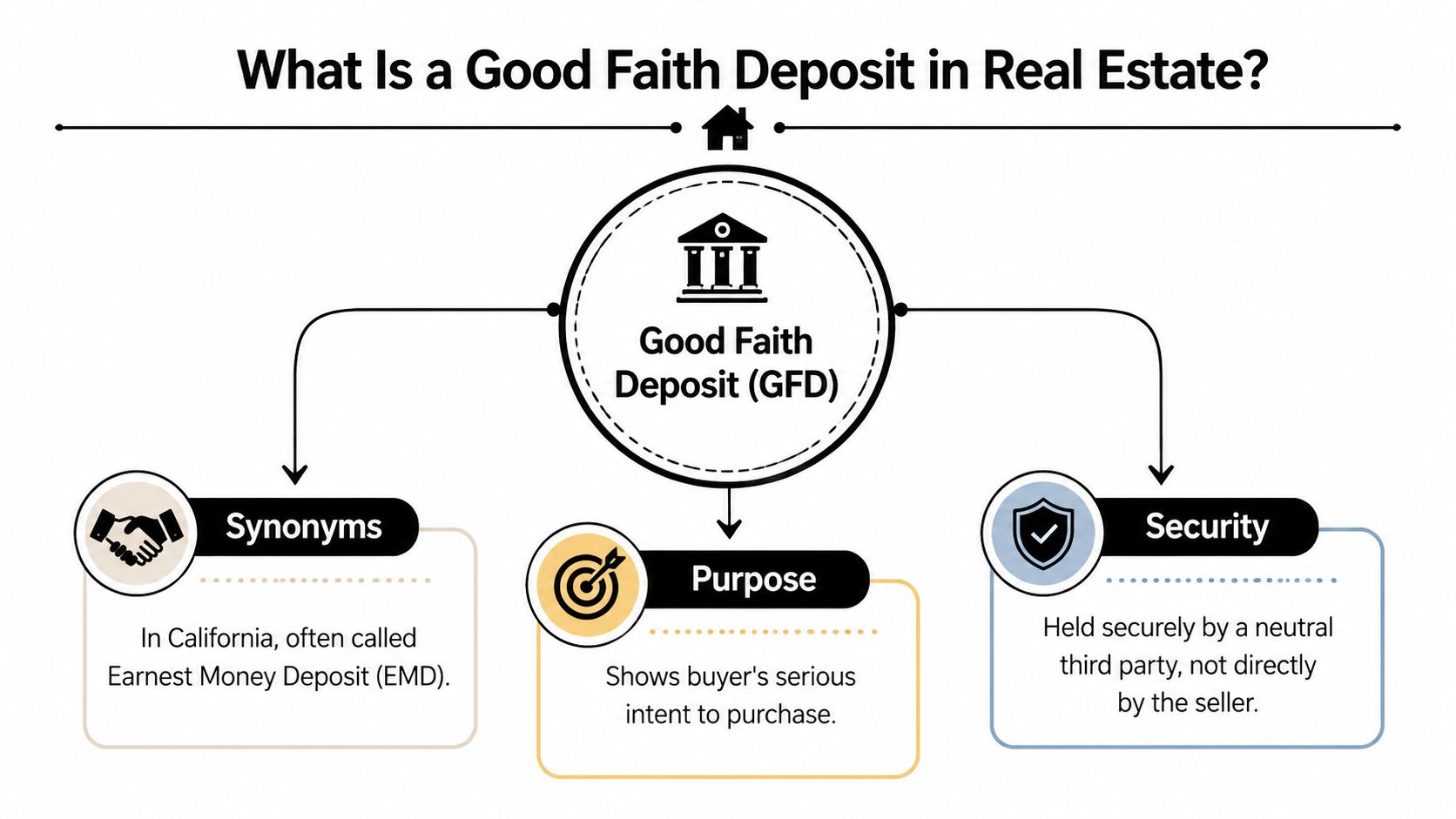

What Is a Good Faith Deposit in Real Estate

A good faith deposit in real estate is money a buyer puts forward to show serious intent to purchase a home. In California transactions, people often use this term to mean earnest money deposit.

It serves as a commitment deposit, not a penalty and not an extra charge layered on top of your purchase. If the sale closes, that money is generally credited back into the transaction instead of disappearing.

The simple version

If you rent, a security deposit is a familiar idea. You put money down to show commitment and create accountability. A home purchase deposit works differently in the details, but the basic purpose is similar. It tells the seller, “I'm committed enough to put real money behind this offer.”

That matters because once a seller accepts your offer, they usually stop marketing the home to other buyers. Your deposit helps them feel more comfortable taking that step.

Where people get confused

This is one of the biggest misunderstandings in homebuying. Good faith deposit and earnest money are often treated like the same thing, but they aren't always identical in every context.

Some lenders use “good faith deposit” to describe upfront lender fees, while earnest money is typically held in escrow and credited toward closing, as explained in this overview of earnest money versus good faith deposit distinctions. That difference matters because refund rules and risk can be different depending on which payment you're talking about.

What it means in a California purchase

In a home purchase contract, the practical meaning is usually this:

| Term | What buyers usually mean |

|---|---|

| Good faith deposit | Money showing you're serious about buying the home |

| Earnest money deposit | The purchase-related deposit tied to the contract |

| Escrow deposit | The same money once it is being held by escrow |

Practical rule: If someone mentions a good faith deposit in your offer paperwork, ask one direct question. “Is this earnest money tied to the purchase contract, or a lender fee?”

That one question clears up a lot of confusion fast.

For most California buyers, the deposit discussed during the offer stage is earnest money. Its job is to support your offer, help secure the property, and later get credited in the transaction if closing happens.

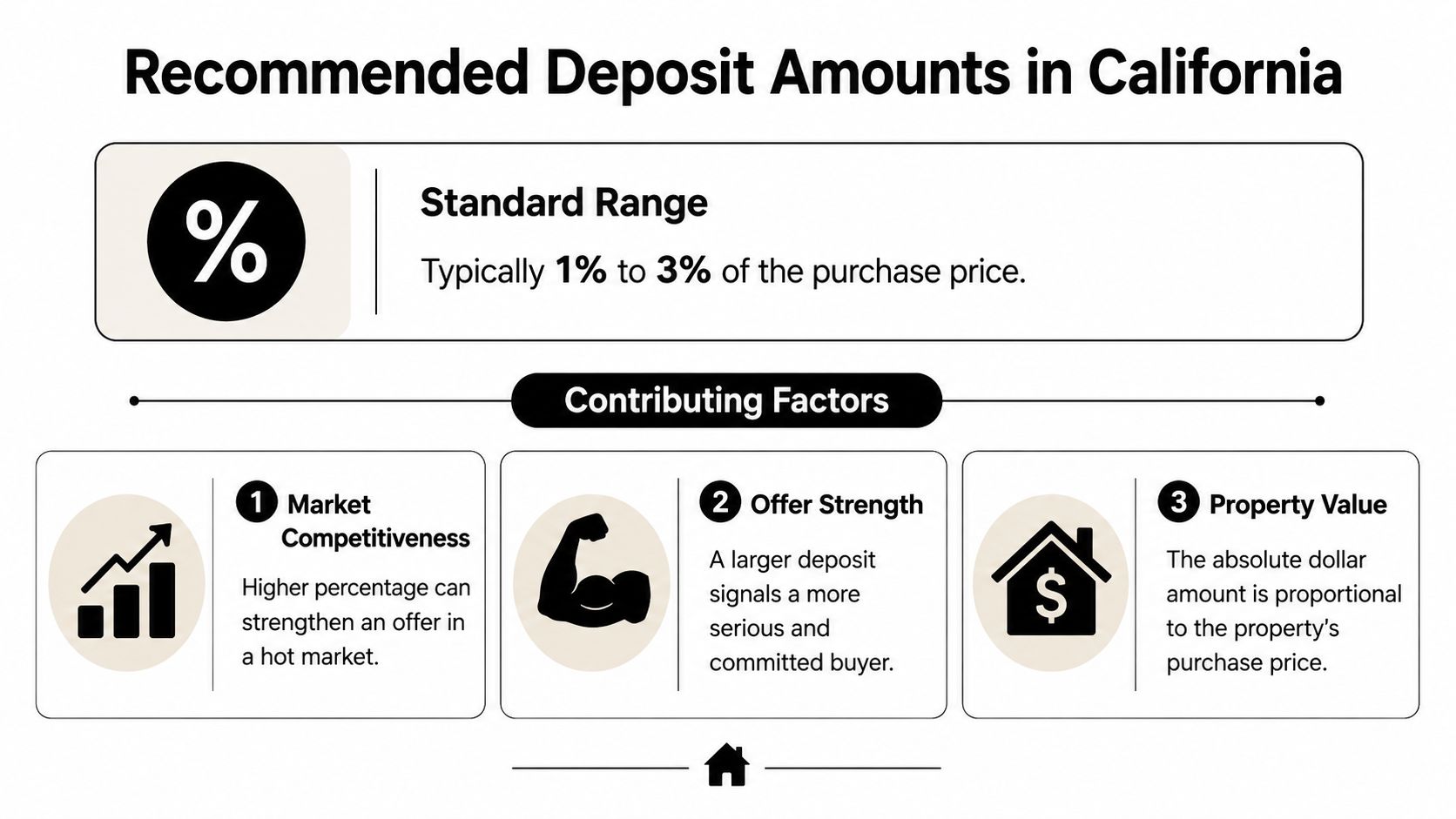

How Much Should Your Deposit Be in California

Most buyers want one clean answer. The actual situation is more strategic than that.

A good faith deposit is typically 1% to 3% of the purchase price, though broader market guidance shows a range of 1% to 10% depending on competition, according to Zillow's guide to earnest money deposit amounts. On a $400,000 home, that means $4,000 at 1% and $12,000 at 3%. In a tighter market, 10% would be $40,000.

Why California buyers shouldn't treat it like a fixed rule

California isn't one uniform market. A deposit that looks strong in one city may look ordinary in another. Seller expectations can also change from one neighborhood to the next, especially if a home is well priced and attracts multiple offers.

A larger deposit can make a seller more comfortable because it signals commitment. But bigger isn't automatically better for every buyer. If putting more money into the deposit leaves you stretched for inspections, reserves, or closing funds, the “stronger” offer may put you in a weaker financial position.

A practical way to think about the number

Use the deposit as a negotiation tool, not a badge of courage. Ask yourself:

- How competitive is the property: If the seller has strong interest, a higher deposit may help.

- How much cash do you need to keep available: Preserving flexibility matters if you're using financing with tight cash planning.

- How strong are the rest of your terms: A solid preapproval, clean timelines, and realistic contingencies can offset a smaller deposit.

- How comfortable are you with the contract deadlines: A larger deposit only makes sense if you can manage the process carefully.

A balanced approach for HERO buyers

For many HERO buyers, the smartest deposit isn't the largest one possible. It's the amount that communicates seriousness without undercutting the rest of your plan.

That matters if you're a buyer using VA or FHA financing, or combining your mortgage strategy with assistance options. Cash used for the deposit is cash you can't use somewhere else in the transaction. The goal is to stay credible with the seller while keeping enough room to handle the purchase smoothly.

Sellers don't only compare price. They compare confidence. Your deposit is part of that confidence, but so are your financing strength, timeline, and contract terms.

The Escrow Process From Deposit to Closing

One of the most common fears buyers have is that the seller gets the deposit right away and can keep it. That's not how this usually works.

The deposit is generally held by an escrow holder in a trust account, and release of the funds usually requires either closing or mutual consent if the deal falls apart, according to this explanation of how earnest money is held in escrow. That setup protects both sides.

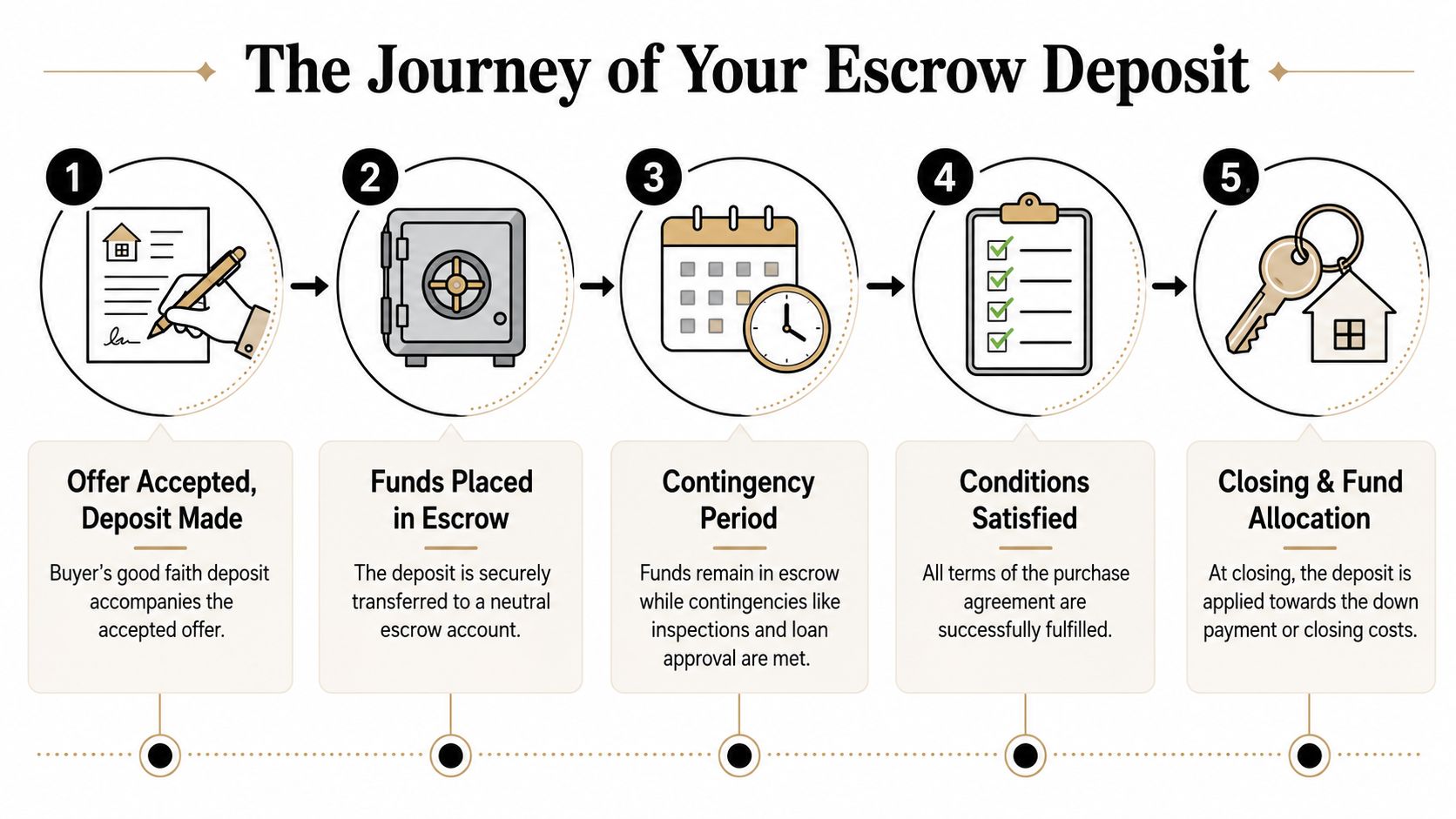

What happens after your offer is accepted

The process is more orderly than many first-time buyers expect.

Your contract is signed

Buyer and seller agree to the purchase terms.You submit the deposit

The money goes to the escrow holder, not directly to the seller.Escrow holds the funds

The deposit stays in a trust account while the transaction moves forward.The contract terms are worked through

Inspections happen. The lender does its review. The title and closing process continue.Closing happens or the contract is canceled

At closing, the deposit is applied in the transaction. If the deal is canceled under the contract terms, the release process follows the agreement.

Why this setup helps buyers

Escrow acts like a neutral middle. That matters because homebuying involves money, documents, deadlines, and competing interests. A neutral third party reduces the chance that one side controls everything.

For buyers, this means your deposit isn't just floating around unprotected. It's being handled under the purchase agreement and escrow instructions.

Where the money goes at the end

If the transaction closes, the deposit is typically credited toward your purchase costs. Depending on the structure of your deal, it may help cover part of what you would otherwise need to bring in at closing. If you want a better handle on that side of the transaction, this guide to California closing costs and who pays what is useful before you get deep into escrow.

The safest way to think about escrow is this. Your deposit is being held for the transaction, not handed over as a gift to the seller.

That distinction gives buyers more peace of mind, especially when the numbers feel large for the first time.

Protecting Your Deposit with Contingencies

The deposit itself doesn't protect you. The contract protects you.

That's where contingencies come in. A contingency is a condition built into the purchase agreement that gives you a defined path to cancel the contract under certain circumstances. If a covered contingency applies and the contract procedures are followed, buyers can often recover the deposit. If protections expire and a buyer defaults later, the risk of losing the deposit rises.

The three protections buyers ask about most

Most of the worry around a good faith deposit comes down to one question: “How do I avoid losing it?” In many transactions, these are the clauses buyers focus on.

Inspection contingency

This protects you if the property condition turns out to be different from what you reasonably expected.

Maybe the inspection reveals roof issues, plumbing trouble, electrical concerns, or other material defects. The point isn't that every home needs to be perfect. The point is that you need a contractual option if the house has problems you didn't knowingly agree to accept.

Appraisal contingency

This matters when the home's appraised value comes in below the contract price.

That can create a gap between what you agreed to pay and what the lender is willing to support. Without this contingency, a buyer may feel pressure to bring in more cash, renegotiate quickly, or move forward on terms that no longer make sense.

Loan contingency

This protects you if financing can't be secured as expected.

Even strong buyers can hit loan issues because of underwriting conditions, documentation questions, property concerns, or shifts in qualification. The loan contingency is one of the clearest examples of why a deposit should never be viewed in isolation from the rest of the contract.

Why deadlines matter as much as the contingency itself

Buyers sometimes hear “you have contingencies” and assume that means automatic protection from start to finish. It doesn't work that way.

A contingency is only as useful as your follow-through. You need to track deadlines, complete inspections, respond to lender requests, and understand when protections are active, removed, or expired.

| Contingency | What it protects against | Why it matters |

|---|---|---|

| Inspection | Unacceptable property condition | Helps you avoid buying hidden problems |

| Appraisal | Value coming in below expectations | Helps prevent paying more than the financing supports |

| Loan | Financing not being approved as planned | Helps protect your deposit if the loan falls through |

A strong offer isn't just aggressive. It's clear, disciplined, and protective where it needs to be.

For California buyers, especially first-time buyers and HERO households trying to preserve cash, the smartest move is usually not waiving protections casually. If a seller wants a cleaner offer, there may be other ways to make it attractive without exposing your deposit unnecessarily.

Deposit Strategies for California HERO Buyers

California HERO buyers often need a different deposit strategy than generic homebuying articles suggest. Veterans, first responders, teachers, nurses, and public employees may have strong employment and strong financing, but they still need to manage cash carefully.

That's especially true if you're trying to buy while preserving reserves, using assistance options, or avoiding an overextended monthly budget.

Why VA buyers have a different angle

For VA loans, the good faith deposit may be redirected to closing costs because no down payment is required, and deposits are typically due within three days of agreement on a written contract, according to PenFed's explanation of good faith deposits and VA loan timing.

That creates an important strategic point. If your loan doesn't require a down payment, the deposit may still play a valuable role in the transaction without functioning the same way it would for a buyer expecting to bring a traditional down payment.

How to make a smaller deposit feel stronger

A smaller deposit doesn't automatically equal a weak offer. Sellers look at the full package.

You can often strengthen a moderate deposit by tightening the rest of the deal:

- Show clean financing: A fully reviewed preapproval can reassure the seller that your loan is realistic.

- Keep documents ready: Fast responses during underwriting and escrow reduce friction.

- Use realistic timelines: If you can close smoothly and on schedule, that can matter as much as a larger deposit.

- Protect liquidity on purpose: Keeping funds available for inspections, closing, and reserves can make the transaction more stable.

When a larger deposit may still make sense

There are situations where increasing the deposit is reasonable. If you're competing for a property with strong demand, and you have enough cash to do it without jeopardizing the rest of your purchase, a larger deposit may help the seller feel more secure.

But the key is intentionality. You don't want to offer a number that looks bold on day one and feels painful by day five.

A smart HERO mindset

Many buyers in service professions are used to being dependable under pressure. That's an advantage in homebuying too. The best deposit strategy often reflects discipline, not bravado.

If you're comparing lenders or program options, it helps to work with teams that understand service-based buyers and assistance-focused planning. California Loans for Heroes is one example of a California-focused program built around veterans, first responders, educators, healthcare workers, and other public-serving buyers.

The strongest offer is the one you can actually finish. A deposit should help you win the house without making the rest of the purchase harder to complete.

Frequently Asked Questions About Good Faith Deposits

Is the good faith deposit the same as the down payment

No. They are not the same thing.

The deposit is an early contract payment that shows commitment. If the deal closes, it is usually applied within the transaction rather than treated as a separate extra charge. Buyers often confuse the two because both involve bringing money into the purchase, but they happen at different stages and serve different purposes.

Is the good faith deposit always refundable

Not automatically.

Whether you get it back depends on the contract terms, your contingencies, and whether deadlines were followed properly. If the transaction fails under a covered contingency, buyers can often recover the deposit. If a buyer backs out without a contractual basis after protections are removed or expired, the risk is much higher.

Does the seller hold my deposit

Usually, no.

In most residential transactions, the deposit is held by a neutral escrow holder rather than handed directly to the seller. That gives both sides a more controlled process and helps reduce disputes over who gets the funds and when.

What happens if the seller backs out

The answer depends on the contract and the specific facts of the transaction.

In practical terms, buyers should immediately review the agreement with their agent, escrow officer, and if needed a qualified real estate attorney. The key issue is what the contract says about cancellation, release of funds, and each party's rights when the seller fails to perform.

Can I use any payment method for the deposit

Payment methods vary by transaction and by escrow instructions.

Many buyers use secure forms of payment such as a wire transfer or cashier's check because escrow companies want clear, verifiable funds. The right move is to follow the exact written instructions from the escrow holder and verify them carefully before sending money.

Can I lose my deposit even if I thought I had contingencies

Yes, that can happen.

The most common problem isn't that buyers never had protections. It's that they assumed the protections lasted longer than they did, or they missed a notice, deadline, or response requirement. A contingency is only useful when the buyer understands how and when to use it.

Is a bigger deposit always better in California

No.

A larger deposit can strengthen an offer, but it can also tie up cash you may need elsewhere in the purchase. For many California buyers, especially HERO households using VA, FHA, or assistance-based strategies, a balanced offer with solid financing and well-managed contingencies may be smarter than putting up the biggest deposit possible.

If you're buying in California and want help structuring an offer without overextending your cash, California Loans for Heroes works with veterans, active-duty military, first responders, educators, healthcare professionals, and other public service buyers across the state. Their team can help you understand how your loan type, closing costs, and good faith deposit fit together so you can move forward with more clarity and less guesswork.