You’ve saved for the down payment. You’ve run the payment numbers. Then the Loan Estimate lands in your inbox, and the cash due at closing is far higher than you expected.

That reaction is normal, especially in California, where buyers already juggle high prices, insurance costs, and tight timelines. The good news is that closing costs aren’t a mystery fee pile you have to accept without question. If you know which charges are flexible, which ones are worth shopping, and when to ask for help, you can lower what you bring to the table.

For many buyers I talk with, especially veterans, first responders, nurses, teachers, and other public service professionals, the right question isn’t just how to buy the home. It’s how to reduce closing costs without creating a worse deal later. That’s where strategy matters.

Understanding Where Your Closing Costs Come From

The first time most buyers scan a Loan Estimate, they focus on the bottom line and miss the structure. That’s where mistakes happen. If you want to know how to reduce closing costs, start by separating the charges into buckets instead of treating them like one giant number.

Closing costs typically run about 2% to 5% of the loan amount, and Bankrate notes that a 2025 Lodestar report found average closing costs for a U.S. borrower buying a single-family home were $4,661. On a $400,000 mortgage, that 2% to 5% range works out to roughly $8,000 to $20,000. Bankrate also notes that in high-cost states like California, borrowers often feel these costs more sharply, which is why smart comparison shopping matters so much in this state.

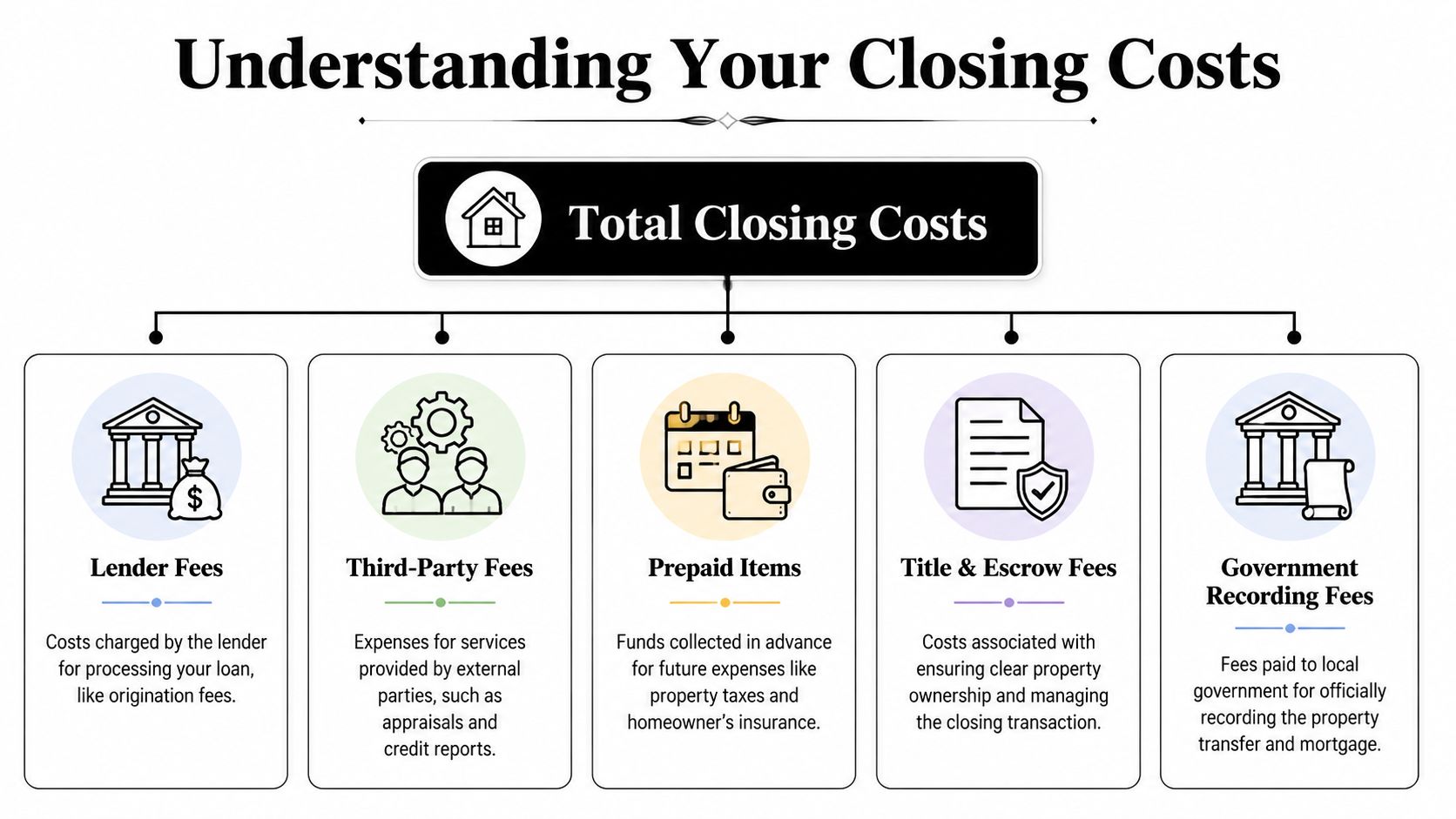

The three buckets that matter most

I like buyers to think about closing costs in three practical groups.

| Bucket | What it includes | Can you reduce it? |

|---|---|---|

| Lender fees | Charges created by the lender for making the loan | Often yes |

| Third-party fees | Charges from outside providers involved in the transaction | Sometimes |

| Prepaid items | Money collected upfront for future bills | Usually not in the same way |

Lender fees are the first place to look. These are the charges the lender controls directly. If one lender's costs look heavier than another's, this is usually where the difference shows up.

Third-party fees include services tied to the transaction. Some are selected through the lender's process, while others may give you room to shop depending on the file and provider rules.

Prepaid items are different. Buyers often think every dollar due at closing is a “fee,” but some of that cash is money being set aside for property taxes, homeowners insurance, and similar obligations. That distinction matters because you negotiate true fees differently than you manage prepaid cash needs.

Practical rule: Don't ask, “Why are closing costs so high?” Ask, “Which line items are lender-controlled, which are shoppable, and which are simply prepaid obligations?”

What deserves your attention on page one

When you review your estimate, slow down and mark anything that falls into one of these categories:

- Lender-controlled charges that may be reduced, waived, or offset.

- Vendor charges where you may have a choice of provider.

- Prepaids that are real cash needs, but not profit centers for the lender.

That's the difference between feeling trapped and seeing opportunities. If you want a more detailed walkthrough of each line item, this closing costs breakdown for California buyers is a useful reference point while you compare documents.

What usually works and what usually doesn't

Buyers save the most when they target the negotiable areas. They waste time when they challenge charges that are pass-through costs or prepaid obligations.

A better approach is to treat your estimate like a roadmap. Circle the lender fees first. Flag the service providers second. Then separate the unavoidable prepaids so you don't spend energy fighting the wrong battle.

Strategies for Shopping and Comparing Lenders

The cleanest way to reduce closing costs is simple. Get multiple Loan Estimates and compare them side by side. Most buyers shop rate. Savvy buyers shop the entire offer.

Freddie Mac and Experian both emphasize comparing estimates from multiple lenders and reviewing fees carefully rather than accepting the first quote. That advice sounds basic, but it's how you gain a true advantage. Once you have competing estimates, you're no longer asking a lender to “help.” You're giving them a concrete chance to earn your business.

Build a comparison set that gives you leverage

Don't collect random quotes over a long period. That creates noise because pricing changes.

Use a short window and compare different lender types:

- A major bank if you already have a relationship there.

- A local credit union if you want to compare fee structures and service style.

- A mortgage broker or specialized lender if you want a broader set of loan options.

Ask each one for a formal Loan Estimate close together in time so you're looking at offers under similar market conditions.

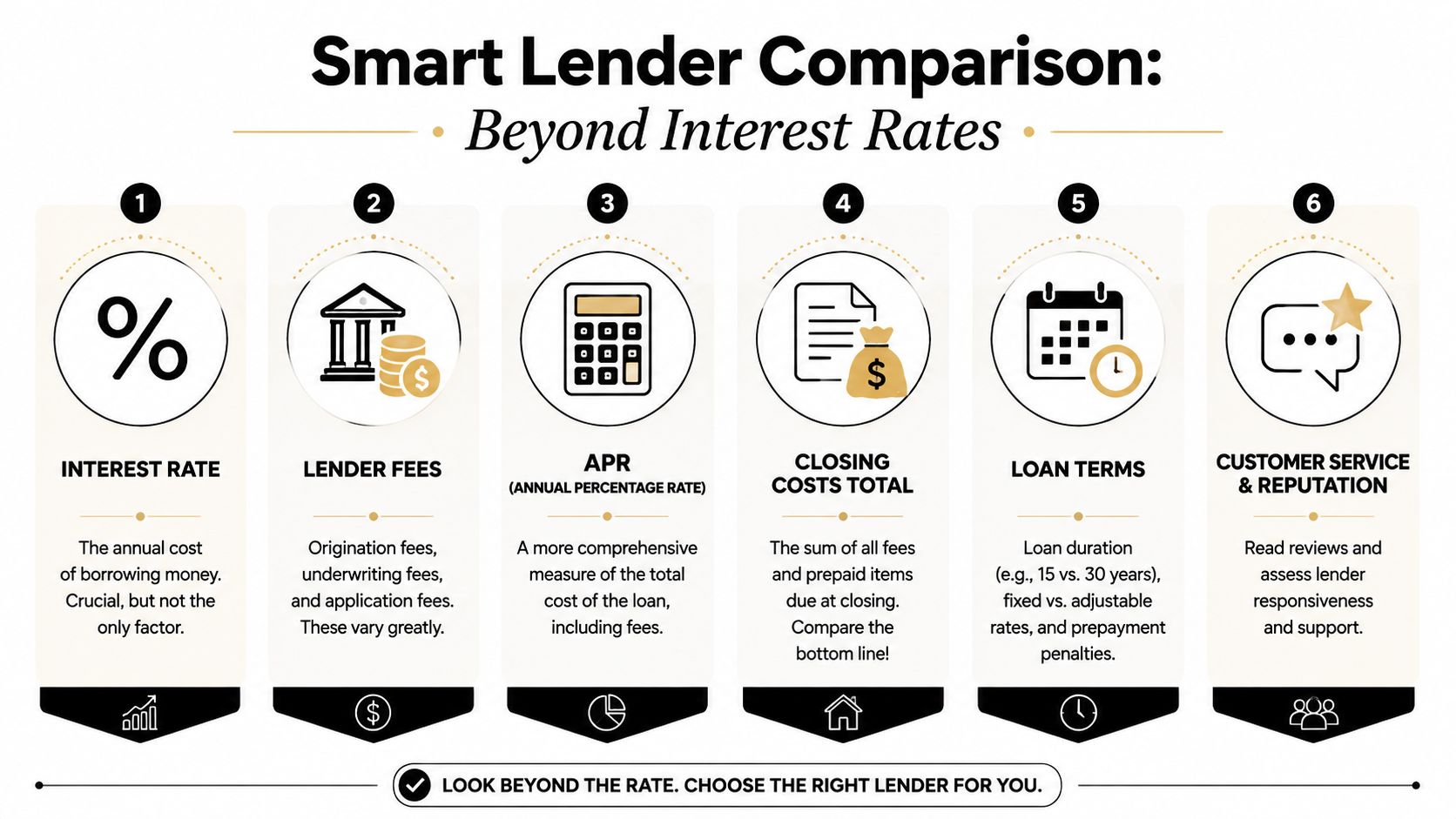

What to compare beyond the rate

A lower rate doesn't always mean a lower-cost loan. One lender may show a strong headline rate but load more fees into the transaction.

Focus on these parts first:

- Origination charges because lender pricing often differs most for these.

- Services you cannot shop for because some lenders structure these costs differently.

- Total cash needed at closing because that's what hits your bank account.

- APR because it helps show the broader cost picture, not just the note rate.

- Responsiveness because a cheap quote that misses timelines can become expensive fast in a California purchase.

If two lenders are close on rate, the better deal often shows up in the fee page, not the first page.

A fast review method

Use this quick screen before you go deep:

| Question | Why it matters |

|---|---|

| Is the rate lower because the fees are higher? | Prevents false savings |

| Are there lender credits involved? | Changes the long-term math |

| Is the cash to close manageable? | Helps with real budgeting |

| Are the fees easy to explain? | Confusion often hides cost |

Then ask each lender to explain anything that looks out of line. A good loan officer won't get defensive. They'll break the numbers down clearly.

If you want a side-by-side framework for evaluating pricing, fees, and structure, this guide on how to compare mortgage rates in California can help you organize the offers.

Effective Negotiation Tactics to Lower Your Fees

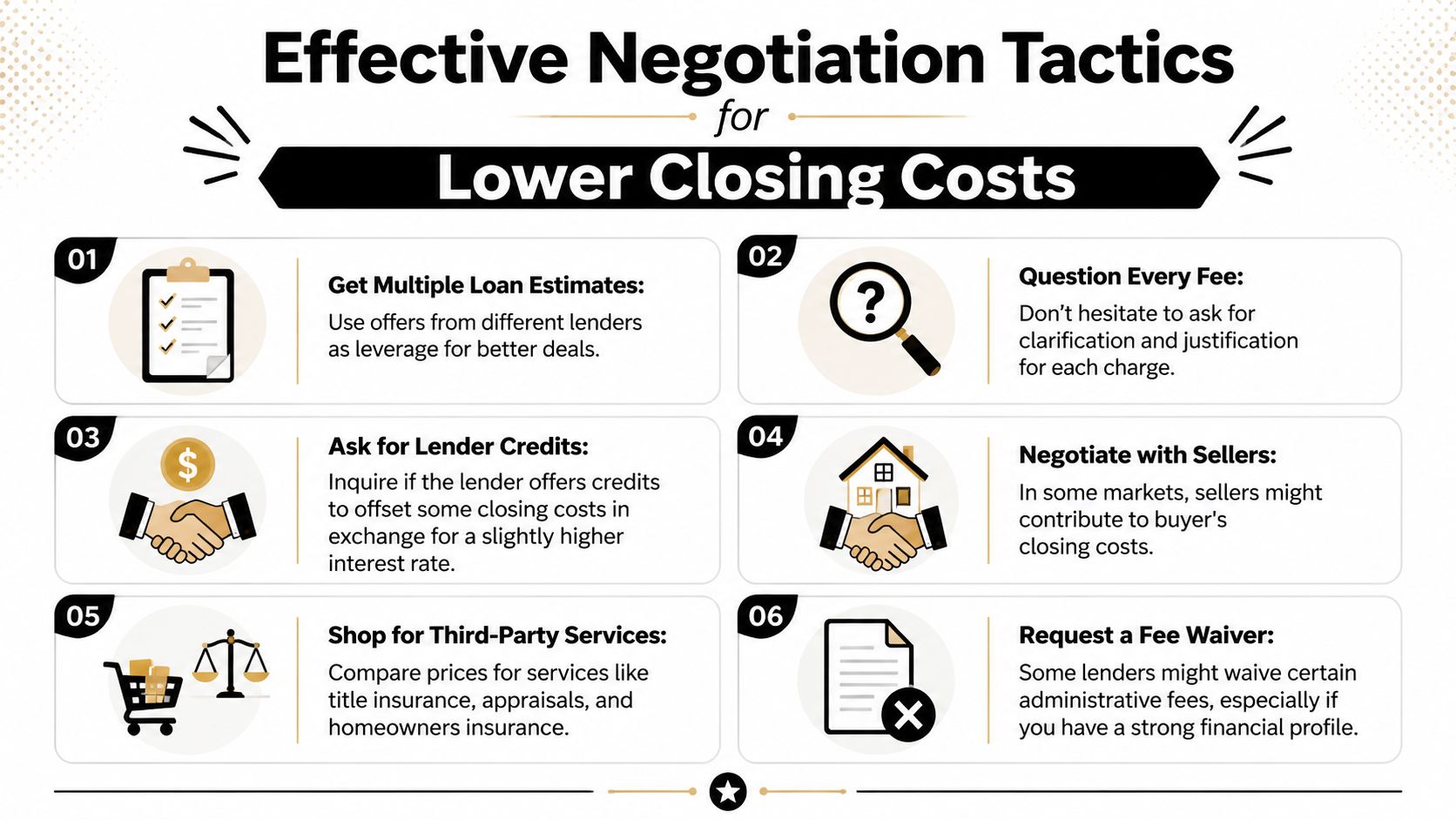

Many buyers assume mortgage fees are fixed because the paperwork looks official. They aren't all fixed. Some are absolutely standard. Some are negotiable. Some can be offset. The key is knowing how to ask without sounding uncertain.

Negotiation works best when it's specific. “Can you lower my costs?” is weak. “Another lender is showing lower origination charges. Can you match or improve this structure?” is better because it gives the lender something concrete to address.

Start with lender-controlled fees

If you only negotiate one area, negotiate the charges the lender controls. That's where movement is most likely.

Use language like this:

“I'm comparing two Loan Estimates. Your overall structure is competitive, but your origination charges are higher. If I move forward with you, can you reduce or waive any lender fees?”

That script works because it's direct and professional. You're not accusing anyone of overcharging. You're giving them a chance to sharpen the pencil.

Here are a few more scripts buyers can use:

-

For a phone call

“I like the way you've structured the loan, but another estimate came in with lower lender fees. What can you do on your side to make this more competitive?” -

For email

“Thanks for sending the estimate. I'm reviewing a competing offer with lower upfront costs. If you can reduce the lender fees or offer a credit, I'm happy to take another look.” -

For a targeted ask

“Can you walk me through which fees are fixed and which ones your team may be able to waive or reduce?”

Question fees without sounding combative

You don't need to challenge every line. You do need to ask for clarity. Buyers who stay quiet often pay more than they need to.

Use this checklist:

- Ask what each charge covers so you can spot duplicate or vague items.

- Ask which fees are lender-imposed because those are often the first candidates for adjustment.

- Ask whether any administrative charges can be waived if your file is strong and your closing timeline is clean.

- Ask whether service providers can be changed if a shoppable fee looks high.

One practical habit matters here. Keep your requests in writing after the call. That prevents confusion later and gives you a record of what was discussed.

Negotiating with the seller in the right market

Freddie Mac notes that seller concessions are more likely in a buyer's market. That matters because your negotiating power with a seller depends heavily on local conditions and how competitive the property is.

A clean way to frame the request is this:

“Instead of reducing the purchase price, would the seller consider a credit toward closing costs so I can preserve more cash for the transaction?”

That approach can be attractive because it helps you with upfront cash while still supporting the deal. In competitive California markets, seller credits may be harder to win. In softer pockets or on listings sitting longer, they become more realistic.

The mindset shift is simple. You're not asking for a favor. You're structuring terms in a business transaction.

Leveraging Credits and California Assistance Programs

A California nurse, firefighter, teacher, or veteran can look at the same Loan Estimate and have a very different goal than another buyer. The issue is often not the total fees alone. It is the cash due at closing and whether that cash squeeze is worth paying more over time.

Lender credits and assistance programs can both reduce what you bring to the table, but they work very differently. A lender credit usually lowers your upfront cash by accepting a higher interest rate. Assistance programs may help with closing funds without changing the core pricing of the first mortgage in the same way. That difference matters.

When lender credits make sense

Experian explains the trade-off clearly. Buyers can reduce upfront closing costs with lender credits, but the higher rate can increase the long-term cost of the loan (Experian on reducing closing costs).

In practice, I see lender credits make the most sense for California hero buyers in a few specific situations. A first responder may want to keep more reserves after closing because shift work can make overtime income inconsistent. A teacher buying before the school year starts may need cash for moving and setup costs. A veteran may prefer to preserve liquidity for repairs, furnishings, or a short-term transition between duty stations or jobs.

Lender credits tend to fit best when you:

- Need to preserve cash reserves after closing

- Expect to sell or refinance sooner rather than later

- Value lower cash-to-close more than the lowest possible payment

They usually fit poorly when you expect to keep the mortgage for many years and can comfortably cover the closing costs upfront.

A simple question cuts through the confusion: if the lender gives a credit today, how much extra will that rate cost each month, and how long will it take before the credit stops being a good deal? Ask your loan officer to show both numbers side by side.

A no-closing-cost loan usually means the cost was shifted into the rate, not removed.

Where California assistance programs can help hero buyers

California buyers in hero professions should also look beyond lender pricing. State, county, city, employer, and profession-based programs can reduce the amount of cash needed at closing, and in some cases they can work alongside the first mortgage rather than replacing it.

The strongest opportunities often show up for buyers connected to:

- Veteran or active-duty military status

- First responder roles

- Healthcare employment

- Education and public service

- Local affordability or workforce housing programs

The details matter. Some programs offer grants. Some use deferred-payment second loans. Some are forgivable after a set period. Others must be repaid when you sell, refinance, or finish the term. That is why I tell buyers not to stop at the headline benefit.

For profession-based options, start with this guide to closing cost assistance for veterans and eligible California hero buyers. California Loans for Heroes also offers hero-focused mortgage options and buyer rewards programs that may reduce certain lender fees or other closing-related costs for eligible buyers.

Questions that protect you from an expensive shortcut

Ask for plain answers to these three questions before you accept any credit or assistance:

- Does this reduce my cash due at closing, my total borrowing cost, or both?

- Does the help come with a higher rate, a second lien, or a repayment trigger later?

- If I keep this home and loan longer than planned, will this still look like a smart decision?

That is the test. The best option is not always the one with the smallest cash number on closing day. It is the one that fits your timeline, your profession, and how long you are likely to keep the loan.

Timing Your Close and Refinancing Considerations

Timing affects closing costs, but not always in the way people think. Buyers often hear that closing at the end of the month “saves money.” That idea needs context.

What usually changes with timing is prepaid interest, not the core fees charged to close the loan. So yes, the day you close can change how much cash you need at the table. No, it doesn't magically erase lender fees, title charges, or other transaction costs.

End of month versus mid-month

An end-of-month closing can reduce prepaid interest because fewer days remain before the next payment cycle begins. That can help if your main goal is lowering the immediate cash due at closing.

A mid-month close can still be the better choice when practical life matters more than shaving prepaid interest. You may get more breathing room for movers, utility transfers, work schedules, school logistics, and final walkthrough issues.

Use this decision guide:

| Closing timing | Often helps with | Possible downside |

|---|---|---|

| End of month | Lower prepaid interest due at closing | Tighter scheduling and less room for delays |

| Mid-month | Easier logistics and less closing pressure | More prepaid interest collected upfront |

That's why I tell buyers to avoid chasing a timing myth. Choose the date that fits both your cash plan and your life plan.

Market conditions matter more than calendar tricks

The stronger your negotiating position, the more likely you are to lower actual costs. In a buyer's market, a seller may be more open to concessions. In a seller's market, speed, certainty, and clean terms often matter more than pushing for every credit.

That matters for timing too. If a fast close helps you win the property, the value of the deal may outweigh a modest difference in prepaid interest. A delayed close that saves a little upfront can still cost you the house.

Choose the closing date that supports the transaction, not just the spreadsheet.

Think ahead if refinancing may be in your future

Refinancing has closing costs too. Buyers sometimes assume they'll “fix it later” by refinancing into a better loan, but the refinance itself comes with its own cost structure.

A no-closing-cost refinance follows the same logic as lender credits on a purchase. You may avoid bringing cash in, but the cost usually shows up elsewhere, such as a higher rate or a larger balance. If you refinance later, apply the same discipline you used on the purchase. Compare offers, isolate the true cost, and calculate whether the change pays for itself over your expected holding period.

That approach keeps you from making the same mistake twice. Once on the purchase, and again on the refinance.

Common Closing Cost Questions for California Heroes

A firefighter gets off a 24-hour shift, opens the Closing Disclosure on a phone in the station parking lot, and sees a higher cash-to-close number than expected. A nurse on rotating weekends asks whether a seller credit helps more than a lower price. A deputy with pension income and overtime wants to know which fees are negotiable in California, and which ones are just part of the file.

Those are the right questions to ask.

Is it better to ask for a price reduction or closing cost credit

Start with your real constraint. If down payment and reserves already stretch your budget, a seller credit usually does more for you than a small price cut because it reduces the cash you need at signing. If you have enough cash but want a lower payment and a little more equity on day one, a price reduction can be the better move.

In California, I often walk buyers through both versions before we write the counter. On paper, the price reduction can look cleaner. In real life, many hero buyers care more about keeping cash available for reserves, uniforms, tools, commuting, childcare, or a post-close repair fund. The right answer depends on what tightens your budget first.

A simple script helps: “We'd like the seller to contribute toward allowable closing costs rather than reduce the price, since preserving cash at closing matters more to us.”

Can I roll all my closing costs into my mortgage

Usually, no.

Some costs can be offset with lender credits. Some can be covered through seller credits if the contract allows. Prepaid items and certain settlement charges still have to be handled in the transaction, and the exact rules depend on the loan type and property.

The key point is simple. Costs do not disappear because they are financed indirectly. If the lender gives a credit, you are usually accepting a higher interest rate. If costs are added through the loan structure where permitted, you may carry that expense over time through your balance or payment. That can be the right call for a California hero buyer who wants to keep more cash in reserve, but it should be a deliberate trade, not a surprise.

What should I do if my Closing Disclosure is higher than my Loan Estimate

Stop and compare every changed line.

Ask the loan officer and escrow officer to identify each increase in writing. Separate lender fees from third-party charges and prepaids. Then ask a direct follow-up question: “Which of these changes came from rate lock timing, escrow and title updates, insurance, taxes, or a valid change in the file?”

That wording matters. It pushes the conversation away from vague explanations and toward line-item accountability.

If something looks off, raise it before signing. Once documents are signed and funds are moving, your options get narrower.

Should I shop for title, insurance, or other services

Yes, if your loan allows it and the savings justify the effort.

California buyers sometimes spend hours trying to trim a small admin fee while ignoring larger charges tied to title, escrow, homeowners insurance, or optional endorsements. A better approach is to ask for the written list of services you can shop, then compare the biggest items first.

Ask this directly: “Which fees are set by your company, which fees are set by the transaction, and which providers am I allowed to choose?”

That question saves time.

Are hero profession buyers treated differently in the process

Sometimes. The profession itself does not automatically reduce standard closing costs.

What it can do is open access to role-specific programs, underwriting flexibility for certain income types, or lender setups that fit your file better. For example, a California teacher, nurse, first responder, veteran, or public employee may qualify for a program the average buyer would never know to ask about. The benefit may show up as a credit, a more favorable structure, or a path around a cash bottleneck.

Ask early, not after disclosures are out. A good question is: “Do you have any California programs or pricing options for my profession, and how would that change my cash to close versus my rate?”

What's the smartest first step if I feel overwhelmed

Organize the estimate before you negotiate anything.

Use three buckets:

- lender-controlled fees

- services you may be able to shop

- prepaids and reserves

Once you sort the numbers that way, the file usually gets much easier to read. You can see which charges may move, which ones are normal for the transaction, and where to focus your questions first.

If you're a veteran, first responder, nurse, teacher, pilot, or public service employee buying in California, California Loans for Heroes can help you review your Loan Estimate, compare cost structures, and identify programs or credits that may reduce your upfront closing burden.