You've got your VA pre-approval. You found a house in California that finally feels right. Then the questions start hitting all at once.

Does the VA require a home inspection? Is the appraisal the same thing? Who pays for what? And if the property has termites, old paint, roof problems, or sketchy wiring, does the deal die or just get more complicated?

That confusion is normal. I see it all the time with veterans, law enforcement officers, firefighters, nurses, teachers, and other California HERO buyers. The good news is this process isn't mysterious once you separate the moving parts. The bad news is too many buyers think the VA is doing a full top-to-bottom inspection for them. It isn't.

If you're buying with a VA loan in California, you need to understand one simple truth early. The VA appraisal helps qualify the property for the loan. The independent home inspection helps protect you. That difference affects your risk, your negotiating power, your timeline, and your confidence going into closing.

The VA Home Loan Inspection Puzzle

A common California purchase goes like this. A Marine veteran gets into contract on a Inland Empire house. A firefighter in Orange County gets an offer accepted on a fixer with “good bones.” A nurse in Sacramento lands a home that checked every box online, then hears three new terms in one phone call: appraisal, inspection, and termite report.

That's when people start blending everything together.

They assume the VA inspection is part of the loan, that it covers the whole house, and that if the lender keeps moving forward, the property must be in great shape. That assumption causes expensive mistakes.

Why buyers get tripped up

The phrase VA home loan home inspection sounds like one thing. In real life, it's usually several separate steps that serve different purposes.

One part is for the loan. Another part is for your protection. In California, there may also be a pest-related step that affects timing and negotiations.

Most buyer stress doesn't come from the inspection itself. It comes from not knowing which review is for the lender and which one is for the buyer.

That distinction matters most in a competitive market. If you're writing offers in California, you need to move fast without getting reckless. You can be aggressive on terms and still stay smart about property condition.

The practical mindset to bring into escrow

Treat the property review process like a layered defense system:

- Layer one: The lender and VA need the property to clear required loan standards.

- Layer two: You need an independent opinion on the home's actual condition.

- Layer three: In California, you need to account for pest-related requirements and common older-home issues before they blow up your closing timeline.

If you understand those layers, you stop guessing. You start making decisions.

That's the goal. Buy with confidence, not false comfort.

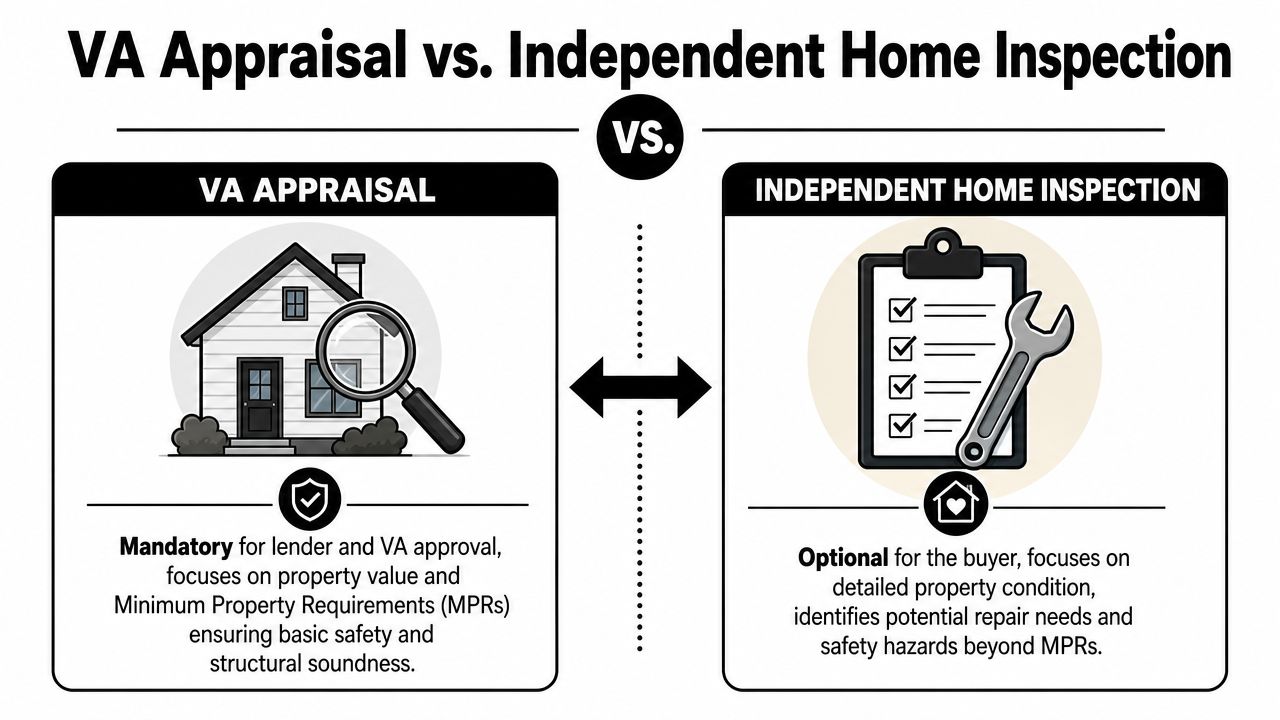

VA Appraisal vs Independent Home Inspection

The cleanest way to understand this is to stop using the words as if they mean the same thing. They don't.

A VA appraisal is required for the loan. A home inspection is optional, but skipping it is one of the worst shortcuts a buyer can take.

What the VA appraisal actually does

The VA home loan program does not require a standard home inspection, but it does require a VA appraisal on every purchase loan to confirm market value and check the property against the VA's Minimum Property Requirements, or MPRs. Those standards are built around whether the home is safe, sound, and sanitary, as explained by Rocket Mortgage's overview of VA loan inspection requirements.

That means the appraisal is doing two jobs:

- Value check: Is the property worth the price being financed?

- MPR check: Does the home meet the VA's basic livability standards?

That's important. But it still isn't a full-condition review.

What the independent inspection does

A private home inspector works for you, not the lender. That inspector is looking more broadly at the property's condition and trying to surface issues that could cost you money, create safety problems, or change your decision to move forward.

Think of it this way:

| Review | Primary purpose | Who it protects most | Typical focus |

|---|---|---|---|

| VA appraisal | Loan eligibility and value | Lender and loan program | Market value and minimum property standards |

| Independent home inspection | Buyer due diligence | You | Broader condition of systems, components, and visible defects |

The appraisal asks, “Can this property back the loan and meet baseline standards?”

The inspection asks, “What am I really buying?”

Who orders it and who pays

The lender orders the appraisal as part of the VA loan process. The independent inspection is typically something you arrange during your inspection contingency period.

Here's the blunt version:

- Appraisal: Required.

- Inspection: Optional on paper.

- Inspection in practice: Strongly recommended.

Practical rule: If you can't afford an inspection, you probably can't afford the surprise repair bill that an inspection might have uncovered.

Where buyers get into trouble

The biggest mistake I see is assuming the VA process itself protects you from hidden defects. It doesn't. The appraisal checks a narrower set of issues. It can flag serious problems, but it may not uncover everything a good independent inspection can reveal.

That's why the smart move for a California VA buyer is simple. Don't ask whether a home inspection is technically required. Ask whether you're comfortable buying a California property without your own detailed condition report.

For most buyers, the honest answer is no.

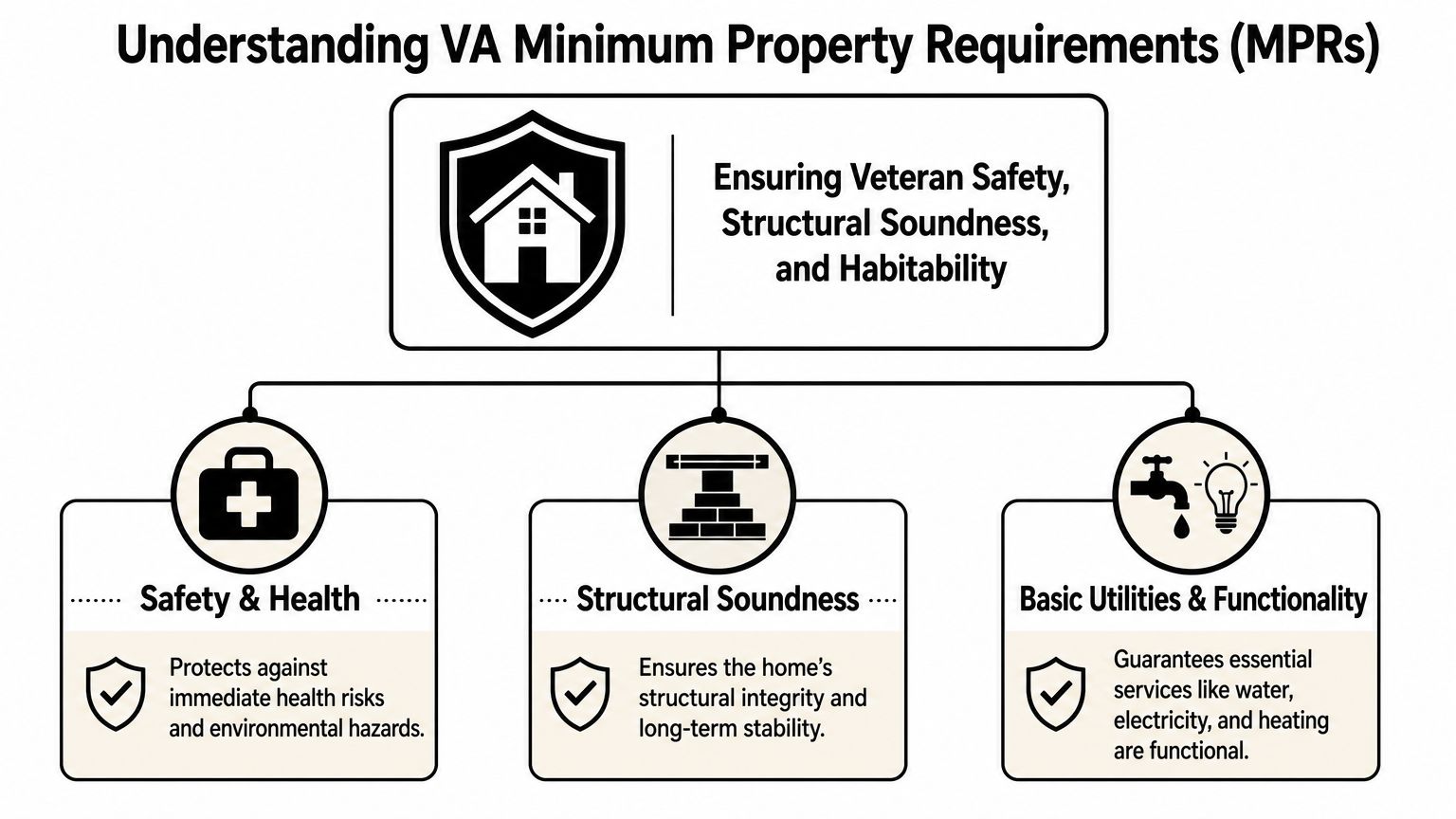

What Are VA Minimum Property Requirements

The VA uses Minimum Property Requirements, or MPRs, to decide whether a home is acceptable collateral for a VA loan. The philosophy is straightforward. The home should be safe, sound, and sanitary.

That sounds broad, so let's translate it into normal homebuyer language.

Safe

A property has to be free of conditions that create immediate hazards. If the appraiser sees obvious safety concerns, those can turn into repair conditions before closing.

Examples include:

- Electrical hazards: Major wiring issues can trigger concern.

- Unsafe access: Stairs and similar features need to be reasonably safe.

- Defective paint in older homes: For homes built before 1978, appraisers must report defective paint or lead-based paint hazards, and the issue must be remediated before the loan can close, according to Chase's explanation of VA loan inspection requirements.

If you're buying an older California home, take the paint issue seriously. A charming bungalow with peeling exterior paint can become a closing problem fast.

Sound

“Sound” is about whether the property is structurally stable and capable of serving as a durable residence.

Bigger red flags become evident:

- Roof failure

- Major structural issues

- Inadequate heating

- Unsafe or failing core components

The VA isn't demanding perfection. It is demanding basic habitability and structural reliability. A home can be dated and still qualify. A home with serious integrity problems may not.

Sanitary

The house also needs to support healthy occupancy.

That usually comes down to utilities and sanitation basics:

- Clean water

- Sanitary sewage disposal

- Functional systems tied to habitability

If there are water or septic problems, those can stop the loan from moving forward until the issue is addressed.

A VA appraiser is not scoring cosmetic quality. The appraiser is looking for conditions that make the home unsafe, unstable, or unhealthy to live in.

What MPRs mean for you in escrow

The key mistake is treating MPRs like a complete buyer protection system. They're not. They're a floor, not a ceiling.

Use this simple lens when a property comes on the market:

| MPR pillar | What it means in plain English |

|---|---|

| Safe | No obvious health or safety hazards |

| Sound | No major issues that threaten the home's basic structural reliability |

| Sanitary | Water, sewage, and core living conditions must support occupancy |

If a home barely clears that bar, your loan may survive, but that doesn't mean the home is a great purchase. That's where your own inspection judgment matters.

Navigating California Specific Inspection Hurdles

California adds its own wrinkles to the VA home loan home inspection process. If you're buying here, generic national advice won't cut it.

The biggest California-specific issue is pests. The VA requires information on wood-destroying insects in certain regions, and the entire state of California is one of those designated areas, according to Freedom Mortgage's summary of VA home loan inspection requirements. So even though a general home inspection is optional under VA rules, California buyers can still face an extra inspection step tied to pest concerns.

Why the termite issue matters in California

In California, older homes, raised foundations, crawl spaces, and long-term deferred maintenance can make pest findings a real negotiation issue.

A termite or wood-destroying insect report can affect:

- Repair demands

- Timeline to close

- Seller willingness to cooperate

- Your comfort with the actual condition of the home

If you're buying in a competitive area, don't wait until the pest report lands to think through your strategy. Have a plan before you remove contingencies.

Other California trouble spots buyers should watch closely

The VA's standards focus on basic habitability. California buyers still need to think like owners.

Some of the most common issues I'd tell a HERO buyer to scrutinize are:

- Older electrical systems: Many California homes have aging components that deserve careful review.

- Roof wear: Sun exposure and age can turn a “working roof” into an expensive medium-term problem.

- Water heater strapping and basic seismic safety items: California buyers should pay attention to practical earthquake-related safety details.

- Deferred maintenance on older properties: Cosmetic neglect often hides system neglect.

None of those automatically kill a VA deal. But they can change whether a property is still a smart buy at the agreed price.

In California, “optional inspection” doesn't mean “safe to skip.” It means the burden shifts to you to investigate the house properly.

A better negotiation posture in California

If you know termite information is likely part of the deal anyway, use that early. Don't frame every request like a personal attack on the seller. Frame it around documented property condition and closing certainty.

That approach works better in California because sellers care about speed and reduced fallout risk. If you present repair requests clearly and tie them to actual findings, you're easier to work with than the buyer who panics late and starts making broad demands.

The buyers who handle California properties best aren't the ones who fear inspection findings. They're the ones who expect them and prepare for them.

Timing Your Inspection and Understanding Costs

Timing matters. Buyers don't usually get hurt because they scheduled an inspection. They get hurt because they scheduled it too late, misunderstood what it covered, or failed to budget for it.

The simple timeline

A practical sequence looks like this after your offer is accepted:

- Open escrow and deposit funds as required by your contract

- Schedule your independent home inspection early

- Allow the lender to order the VA appraisal

- Review findings and decide what to request, accept, or walk away from

- Move toward final loan approval and closing

That order gives you room to make decisions before you're too deep emotionally or contractually.

What the inspection usually costs

The optional buyer-paid home inspection typically costs $300 to $500 for a standard single-family home, with some sources reporting an average near $343 and others citing broader ranges such as $350 to $600 depending on location and home size, based on Veterans United's discussion of VA Minimum Property Requirements.

That's money well spent.

A lot of buyers obsess over the inspection fee and ignore the much larger financial risk of buying blind. That's backwards thinking.

Keep the two cost buckets separate

Use this breakdown:

| Item | Required or optional | Who typically pays |

|---|---|---|

| VA appraisal | Required for the loan | Buyer as part of loan costs |

| Independent home inspection | Optional but recommended | Buyer at time of service |

Your appraisal is part of the loan process. Your inspection is part of your due diligence. Don't mix those buckets mentally or in your budget.

For a broader look at fees that show up near the end of the transaction, review this closing costs breakdown for California buyers.

My recommendation on timing

Book the inspection fast. Don't wait around for the appraisal first. If the house has major defects, you want to know early while your options are strongest.

And don't make the mistake of treating the inspection like a paperwork formality. Read the report. Ask follow-up questions. If the inspector flags concerns that deserve specialist review, take that seriously before you remove contingencies.

How to Negotiate Repairs After Your Inspection

The inspection report is not a shopping list for minor annoyances. It's a decision tool.

If you negotiate like every scratched outlet cover is a crisis, sellers stop taking you seriously. If you ignore serious defects because you're afraid to upset the deal, you hand yourself future repair bills.

The right approach is disciplined, not emotional.

Separate required repairs from negotiable requests

Some issues are effectively mandatory if the VA appraiser flags them as conditions tied to loan approval. Those aren't really debate topics if you want the transaction to close.

Other issues come from your independent inspection and fall into a different category. Those are negotiable.

Use this frame:

- Loan-closing issues: Problems that must be addressed for the VA loan to move forward

- Buyer-risk issues: Problems you're willing to accept, renegotiate, or reject based on cost and comfort

- Cosmetic items: Usually not worth using up negotiation capital

What to ask for

Focus on health, safety, structural, utility, and pest-related concerns. Those requests are easier to justify and more likely to get traction.

Good repair requests often target:

- Safety hazards

- Water intrusion or active leaks

- Major roof concerns

- Electrical defects

- Heating or utility failures

- Pest-related damage or treatment needs

Bad repair requests often revolve around wear, aging finishes, and aesthetic preferences.

Ask for fairness, not perfection. You're buying a resale home, not ordering a custom build.

Sample language that works

Keep your tone firm and clean. Something like this works well:

Based on the independent inspection findings, the buyer requests that the seller address the documented health, safety, and material property issues identified in the report, including any items that could affect financing or occupancy.

Or this:

In lieu of completing all requested work prior to closing, the buyer is open to discussing a credit or other mutually acceptable solution for the documented repair items.

That's professional. It leaves room to solve the problem.

Credits versus repairs

A seller repair sounds great until the work gets rushed. Sometimes a credit is better because you control who performs the work after closing.

But that choice depends on the issue. If the problem could interfere with loan approval or create immediate occupancy risk, repair before closing may be the better path.

If you're early in escrow and want to understand how your upfront deposit interacts with contract risk, review this guide to the good faith deposit in a California home purchase.

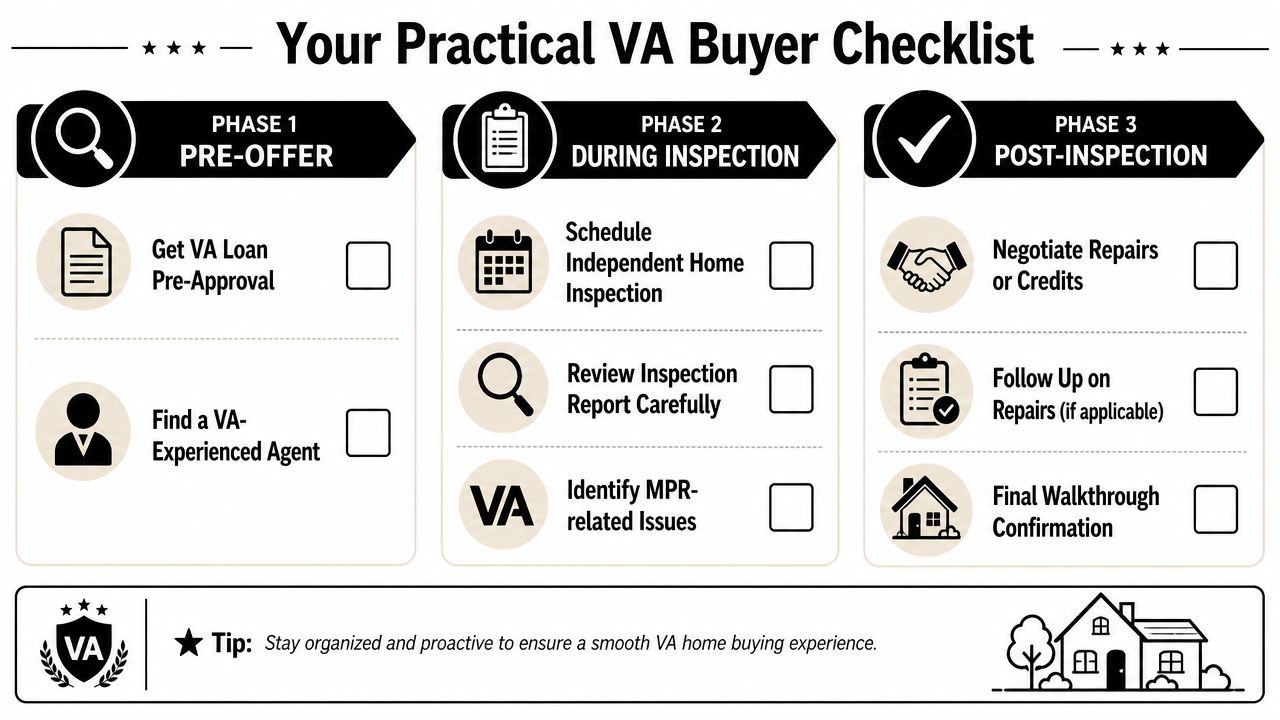

Your Practical VA Buyer Checklist

Use this checklist to keep the VA home loan home inspection process tight and organized.

Before you write or finalize the offer

- Confirm your budget: Include room for an independent inspection and possible follow-up evaluations.

- Know the property type: Older California homes usually deserve extra scrutiny.

- Set expectations with your agent: Decide how aggressive or cautious you want to be on inspection-related terms.

During your inspection window

- Schedule the home inspection quickly: Early information provides an advantage.

- Review the report carefully: Don't skim the summary and call it done.

- Pay close attention to California-specific issues: Pest findings, older systems, roof concerns, and obvious safety defects deserve real attention.

Before removing contingencies

- Separate loan issues from buyer issues: Not every defect is a VA issue, but it can still be your issue.

- Negotiate with focus: Ask for repairs or credits tied to meaningful findings.

- Decide with discipline: If the property condition no longer matches the price or your risk tolerance, step back.

For a broader roadmap of the full purchase process, this guide on the steps to buying your first home in California is a useful next read.

The takeaway is simple. The appraisal helps protect the loan. The inspection helps protect your family, your budget, and your future headache level. Smart buyers use both.

If you're a veteran, first responder, educator, healthcare worker, pilot, or public service professional buying in California, California Loans for Heroes can help guide you through the VA process with clarity and confidence. From pre-approval through closing, their team helps California HERO buyers understand the details, avoid common mistakes, and move forward with a strategy that fits the market they're buying in.