Rent keeps clearing your bank account. Your savings keep growing too slowly. You serve your community every day, but buying a home in California still feels like it belongs to somebody else.

I talk to teachers, nurses, firefighters, law enforcement officers, veterans, and county employees who feel stuck in exactly that spot. They're responsible with money. They can handle a monthly payment. What stops them is the upfront cash. That's where many get discouraged, and it's also where most bad advice starts.

It's simple. Down payment assistance in California can absolutely change the math. But a lot of buyers get misled because they only hear the headline number and not the structure behind it. That's a mistake. In California, the details matter more than the marketing.

Is the California Dream of Homeownership Still Possible

A public school teacher in Southern California spends years doing everything right. She pays rent on time, keeps her credit clean, avoids big debt, and still feels like buying a home is impossible because the down payment looks too high. A nurse in the Bay Area has the same problem. A firefighter in Riverside County can afford the monthly payment on a modest home, but the cash needed to get through closing keeps pushing the goalpost back.

That's the truth for a lot of California buyers. The issue isn't always whether you can own. It's whether you can get through the front door.

The real barrier is upfront cash

Most buyers I meet don't need a miracle. They need a strategy. That strategy often includes down payment assistance California programs that help cover part of the money due at closing.

California has an unusually extensive range of assistance options. Instead of one simple statewide grant, buyers often have to sort through state, county, city, and nonprofit options. That sounds messy, but it also means there may be more opportunity than you think.

Buying in California often fails at the savings stage, not the income stage.

That matters for hero professions in particular. Teachers, healthcare workers, first responders, military families, and public employees often have stable income and strong long-term homeownership potential. They just need help bridging the gap between renting and owning.

Why so many buyers give up too early

A lot of people assume assistance is only for first-time buyers with very low income. That's not always true. Others assume all assistance is basically free money. That's also not true.

Both assumptions cost buyers opportunities.

If you've talked yourself out of applying because you owned a home before, or because you think the programs are too small to matter, or because the fine print seems confusing, you're probably leaving real options on the table. California's market is hard. But hard doesn't mean impossible. It means you need the right map.

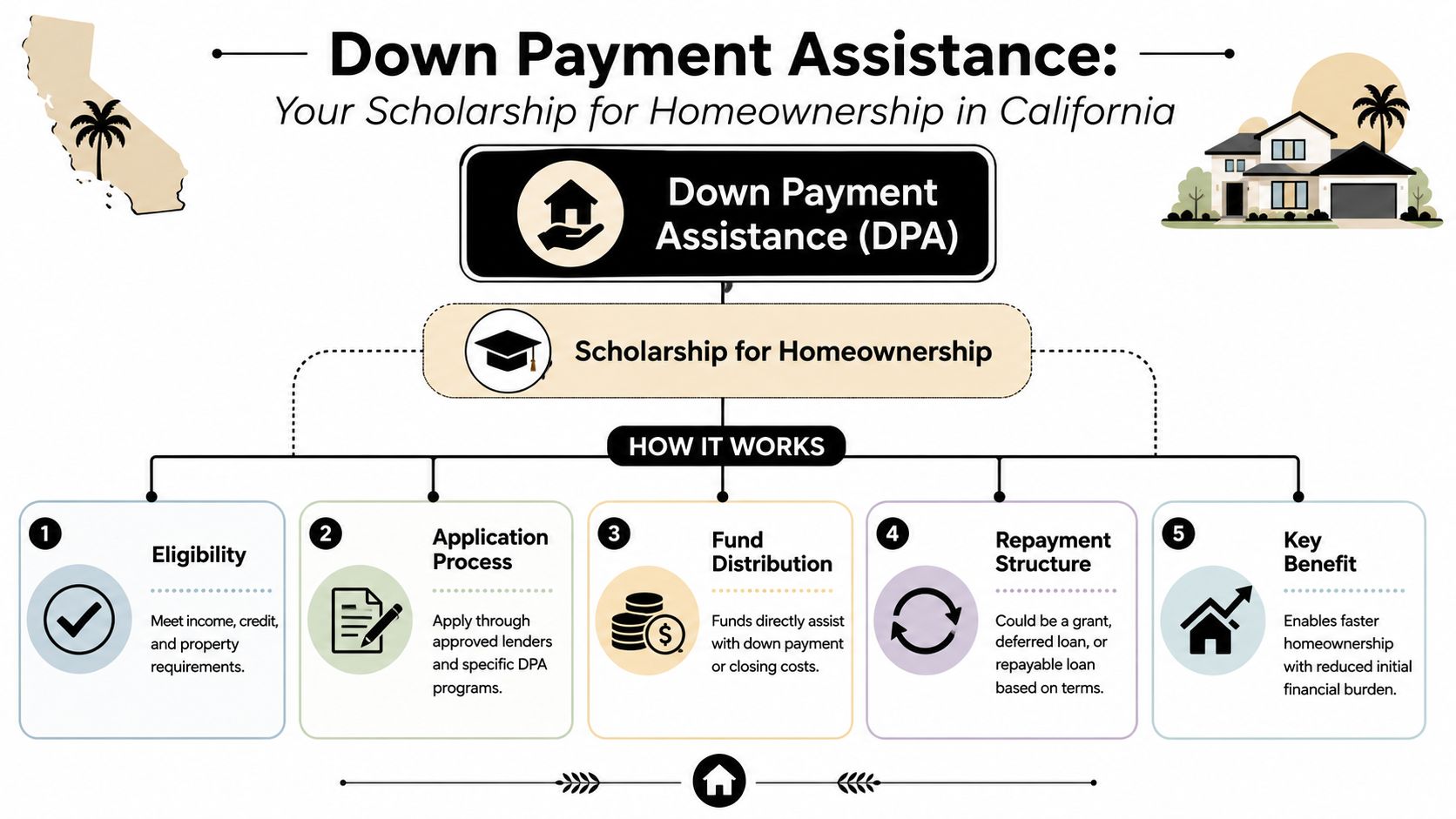

How Down Payment Assistance Actually Works in California

You find a home. Your income supports the payment. Your credit is good enough. Then the deal stalls because closing takes more cash than you can pull together.

That is where down payment assistance helps. It covers part of the upfront money needed to buy, but the structure matters more than the headline amount. In California, the wrong assistance program can solve today's cash problem and create tomorrow's equity problem.

The three structures that matter

California buyers usually see three types of assistance, and they do not behave the same way.

- Grant-style help. Funds go toward your down payment or closing costs. If you meet the program rules, repayment may not be required.

- Deferred-payment second loans. These are often called silent seconds. You usually do not make a monthly payment, but the balance still exists and commonly comes due when you sell, refinance, or pay off the first mortgage.

- Shared appreciation loans. These offer larger upfront help in exchange for a share of your future gain when the home is sold or refinanced.

The trade-off is simple. Grants are the cleanest. Deferred seconds are often manageable. Shared appreciation can be useful, but only if you understand what you are giving up later.

Why program structure matters so much in California

California uses layered assistance because home prices are high and public funds are limited. So the state and local agencies often use deferred repayment or equity-sharing models instead of handing out simple grants across the board.

That makes buyers focus on the wrong question. The first question is not, "How much can I get?" The first question is, "What does this cost me later, and when?"

I tell Hero buyers this all the time. A firefighter, nurse, teacher, or public employee with stable income can qualify for more than one option, but the best fit depends on how long you plan to keep the home, whether you expect to refinance, and how important future equity is to you.

What to review before you choose a program

Use this filter before you get attached to any assistance option:

- How is the money delivered? Grant, deferred second, or shared appreciation.

- When does repayment happen? Never, at sale, at refinance, or under another trigger.

- What happens to your equity later? Some programs reduce your net proceeds when you sell.

- Will it limit your flexibility? Certain programs make refinancing or combining assistance harder.

- Can you stack it with your first mortgage and any local help? Many good options fail here.

If you want a clearer picture of the numbers, review this breakdown of how much down payment assistance can cover in California.

My advice: Do not compare assistance amounts until you compare the repayment terms, equity impact, and refinance restrictions.

Major California DPA Programs You Should Know

You find a home in Riverside or Sacramento. Your income is solid. Your credit is workable. The deal still falls apart because your cash to close is short by an amount that feels impossible to save fast enough.

Buyers often pick the wrong program.

The right move is not chasing the biggest advertised assistance number. The right move is choosing the program whose repayment rules still make sense three, five, or ten years from now. In California, the major options look similar on the surface and behave very differently after closing.

The main program types do very different jobs

| Assistance Type | How It Works | When Is It Repaid? | Best For… |

|---|---|---|---|

| Grant | Funds help with upfront costs and may not require repayment if program rules are met | Depends on program terms | Buyers who want simpler long-term math |

| Deferred-payment loan | A junior loan helps with upfront funds and sits quietly in the background | Commonly due on sale, refinance, or payoff | Buyers who need help now and expect to manage repayment later |

| Shared appreciation loan | Program helps with a larger upfront amount in exchange for part of future appreciation | Commonly repaid on sale or refinance with appreciation share | Buyers who need significant entry support and understand the equity tradeoff |

That distinction matters more than the program name.

CalHFA MyHome

CalHFA MyHome is a deferred-payment junior loan. CalHFA states that it can provide up to the lesser of 3.5% of the purchase price or appraised value for FHA loans, and up to 3% for conventional loans, based on the official MyHome program details.

MyHome fits buyers who are close to qualifying and mainly need help getting over the upfront cash hurdle. I usually like it better for borrowers who want a cleaner exit strategy than a shared-appreciation program. You still need to plan for repayment later, but you are not giving away a piece of future appreciation.

GSFA Platinum

GSFA Platinum is often one of the more practical programs to compare early, especially for Hero buyers and repeat buyers who assume state-style assistance is off the table. The structure can be useful when the gap is meaningful but not massive, and when the buyer wants options beyond first-time-buyer-only programs.

It also pairs well with borrowers who want to keep their financing conventional if possible. If that is the route you are considering, review how a conventional loan with down payment assistance works before you choose a first mortgage.

Dream For All

Dream For All gets attention for one reason. The assistance amount can be far larger than what buyers see in more traditional deferred-second programs.

That size comes at a price. This is a shared-appreciation structure, which means the program can claim part of your future gain when you sell or refinance. For some buyers, especially in expensive California markets, that trade is worth it because it gets them into a home sooner. For others, it becomes expensive later and limits how they feel about building equity.

My advice is simple. Use Dream For All only if the larger assistance amount changes the outcome enough to justify giving up future upside. If a smaller deferred-payment option gets you into the home, I would compare that path very seriously before accepting equity sharing.

Bigger assistance can create a worse long-term deal.

Local programs can beat the statewide options

A lot of buyers spend too much time comparing only the headline statewide programs. That is a mistake.

County and city programs can be stronger, more targeted, or easier to combine with the right first mortgage. Some focus on local workforce buyers. Some put more weight on income limits, location, or household size. Others are better for teachers, nurses, public employees, and first responders buying in the communities they serve.

The catch is consistency. Local programs vary a lot by county, funding cycle, and property location. One city may offer meaningful help while the next city over offers nothing useful. This is why broad online lists only get you halfway there.

My recommendation

Start your comparison with these three questions:

- Which program gives you enough cash to close without overpaying later?

- Which program leaves you the most flexibility to refinance or sell?

- Which program still works if you are a repeat buyer or buying under a Hero profession guideline?

If you are choosing between MyHome, GSFA Platinum, and Dream For All, do not treat them as interchangeable. They solve different problems. The best choice is usually the one with the least expensive trade-off, not the one with the biggest headline.

Eligibility for California Heroes and Repeat Buyers

The biggest myth in this space is that down payment assistance is only for first-time buyers. That myth knocks out a lot of strong borrowers before they even apply.

It's wrong.

Repeat buyers are often still in play

Some of the most relevant California programs aren't limited to first-time buyers. GSFA Platinum is available to both first-time and repeat buyers, and its Assist-to-Own feature serves specific occupations, as outlined in Bankrate's California first-time homebuyer assistance overview.

That matters if you're a teacher who owned years ago, a firefighter relocating for work, or a county employee buying again after a life change. Prior ownership doesn't automatically disqualify you.

Hero professions can have meaningful advantages

I work with borrowers who often assume their profession doesn't change anything. Sometimes it does.

Programs can include occupation-based features, local workforce priorities, or special access tied to county employment and public service roles. The catch is that these opportunities are rarely obvious when you're scanning generic mortgage articles.

Here's what hero buyers should assume from the start:

- Your profession may matter. Teachers, county workers, first responders, healthcare professionals, veterans, and public employees should ask about occupation-specific overlays.

- Your geography absolutely matters. A city or county boundary can determine whether a program is available.

- Your occupancy matters too. Most programs expect the property to be your primary residence.

- Your old assumptions may be outdated. Owning before doesn't mean you're done with assistance.

Eligibility is layered, not simple

The situation frequently causes buyers to get tripped up. You're usually dealing with more than one rulebook at the same time.

A borrower may need to satisfy the first mortgage guidelines, the assistance program rules, and any city or county overlays. One program might work for your income but not your target property. Another might fit your property but not allow the stacking strategy you hoped to use.

The hardest part isn't always finding a program. It's lining up all the rules at the same time.

What I tell hero buyers first

Don't self-reject.

If you're in law enforcement, EMS, military service, healthcare, education, aviation, or public employment, assume there may be a path until a lender who understands these programs tells you otherwise. Too many buyers hear “first-time homebuyer program” and immediately leave the table when they shouldn't.

And if you're a repeat buyer, ask direct questions. Don't ask, “Do you have assistance?” Ask, “Which programs can work for repeat buyers in my county, with my occupation, and my loan type?” That question gets better answers.

Your Step-by-Step Guide to Applying for DPA

Most buyers make this harder than it needs to be because they start with listings instead of strategy. Don't shop for homes first. Build the financing plan first.

That order saves time, stress, and failed escrow.

Start with a real financial review

Look at your income, debts, savings, and credit profile as they are, not as you hope they are. The goal isn't perfection. The goal is to understand which lane you belong in before you apply.

If something needs work, fix it early. Small issues become expensive delays when they show up after you're under contract.

Choose a lender who understands program stacking

Not every lender handles California assistance programs well. That matters because many deals involve layering the first mortgage with a second lien, local rules, education requirements, and timing issues.

A DPA-savvy lender should be able to tell you:

- which programs may fit your occupation and county

- whether the assistance works with your likely loan type

- what repayment structure you're accepting

- what cash you still need at closing

If you need a clean overview of the buying sequence, this guide on the steps to buying your first home gives a helpful roadmap.

Complete required education early

Many assistance programs require a homebuyer education course. Buyers often treat this like a minor task and leave it to the last minute. That's a mistake.

Handle it early, save the certificate, and keep your file organized. It's one of the simplest parts of the process, but it can still slow you down if you ignore it.

Build your document file before you shop

Don't wait until you have a purchase contract to hunt down paperwork.

Gather your key documents in advance:

- Income records. Pay stubs, W-2s, or other proof your lender requests.

- Asset statements. Bank and investment statements that show available funds.

- Identification documents. Government-issued ID and anything program-specific.

- Housing history. Landlord information or mortgage history if needed.

- Education certificate. Keep proof of course completion ready.

Apply for the mortgage and the assistance together

This is the part many buyers misunderstand. The DPA application usually isn't some totally separate side project. It often needs to be integrated with your mortgage approval and closing timeline.

That means your lender should be managing the full picture, not just the first mortgage. If the lender treats assistance like an afterthought, expect delays.

Buyers who prepare their DPA file early usually have more options and fewer surprises.

Don't lock onto one program too soon

You might qualify for more than one route. That's good news, but only if you compare them properly.

One option may offer less cash and better long-term economics. Another may provide a larger upfront benefit but reduce future equity or flexibility. The right answer depends on whether your priority is entry, lower cash to close, refinance freedom, or long-term wealth building.

Common Pitfalls and How to Avoid Them

You find a program that gives you more cash upfront, your offer gets accepted, and you feel relieved. Then you learn that selling later could mean giving up a slice of your appreciation, or refinancing is harder than you expected. I see this all the time. Buyers focus on getting in the door and miss the trade-offs that affect their equity later.

The biggest mistake is treating all assistance as if it works the same way. It does not.

Pitfall one: picking the program with the biggest benefit instead of the best structure

A deferred-payment second mortgage and a shared-appreciation loan solve different problems. One may preserve more of your future wealth. Another may reduce your cash needed today but cost more when you sell. If you are a teacher, nurse, firefighter, law enforcement officer, or other California hero buyer trying to stretch into a high-cost market, that difference matters more than the headline amount.

Here's the rule I give clients. Compare the exit, not just the entry.

How to avoid it:

- Ask what you owe at sale, refinance, and payoff. Get the exact repayment trigger.

- Request side-by-side loan estimates. Compare monthly payment, cash to close, and likely payoff later.

- Choose based on your plan. If you expect to keep the home for a long time, shared appreciation deserves extra scrutiny. If you may refinance sooner, flexibility matters more.

Pitfall two: misunderstanding who actually qualifies

California eligibility rules confuse buyers because they are layered. State rules are one layer. Local program limits are another. Lender overlays can add one more filter. Hero profession eligibility can be especially misunderstood because some programs define public service narrowly, while others are broader. Repeat buyers also get tripped up here. Some assistance options are limited to first-time buyers, but not all of them are.

Do not assume an online summary applies to your exact file.

How to avoid it:

- Verify profession-specific rules in writing. “Hero” is not a universal legal category across programs.

- Check county income limits and property location rules early. One ZIP code can change the answer.

- Confirm whether first-time buyer status is required. Repeat buyers often rule themselves out too early.

- Make sure the home will be your primary residence. Many denials start with occupancy issues.

Pitfall three: using a lender who knows mortgages but not California assistance

This one kills good deals. A lender can quote rates all day and still mishandle down payment assistance. If they do not understand reservation deadlines, subordinate financing rules, program sequencing, or how assistance affects underwriting, your escrow gets harder fast.

You need a lender who can explain the full structure clearly and catch conflicts before you spend money on inspections and appraisal.

How to avoid it:

- Ask how many California DPA transactions they have closed recently.

- Ask which programs can be combined and which cannot.

- Ask what could delay approval on the assistance side, not just the first mortgage.

- Walk away from vague answers. “We'll sort it out later” is a warning sign, not a plan.

Pitfall four: underestimating how much cash you still need

Down payment assistance does not automatically erase closing costs, reserves, prepaid items, or repair negotiations. Buyers often hear “assistance available” and assume they can show up with almost nothing. That is how deals fall apart late.

The fix is simple. Get a realistic cash-to-close estimate early, ask what the assistance does and does not cover, and keep a reserve cushion so one surprise does not knock you out of contract.

Partnering with an Expert for Your California Home Loan

You find a home you can afford on paper. Then the financing gets messy. One assistance option lowers your upfront cash but raises your monthly payment. Another keeps the payment lower but creates a second lien that matters when you sell or refinance. A third looks perfect until someone checks your profession, county limits, or ownership history more carefully.

That is why the right mortgage advisor matters.

You do not need someone who can recite program names. You need someone who can compare structures, explain the trade-offs in plain English, and tell you which option fits your budget, timeline, and long-term plans.

A strong advisor should help you answer a few specific questions:

- Should you use a grant, a deferred second, or a forgivable assistance option

- Does your profession qualify you for hero-focused help, and does it change your best strategy

- Are you ineligible as a repeat buyer, or are you ruling yourself out too early

- What will this assistance cost you later if you refinance, move, or sell

- How much cash should you keep available even after assistance is applied

That last point gets missed all the time. The best program is not the one with the biggest headline benefit. It is the one that still makes sense two years from now.

Hero professions need this level of review even more. Teachers, nurses, firefighters, EMS workers, law enforcement officers, military families, pilots, healthcare workers, and public employees can have access to specialized paths that a general mortgage quote will miss. The rules are not always intuitive, and the labels can be misleading. Some buyers qualify through their profession. Others qualify through income, location, or a first-generation or first-time definition that needs a closer look.

California Loans for Heroes is one example of a hero-focused mortgage resource. It offers California homebuyers in eligible professions guidance on assistance options, mortgage programs, lender credits, and one-on-one support suited for hero households.

My advice is simple. Pick the advisor before you pick the program.

A good California mortgage expert will show you the trade-offs, not just the marketing. They will explain why one buyer should preserve cash, why another should avoid a repayment-triggered second lien, and why a repeat buyer may still have a path to assistance. That clarity is what keeps a good home purchase from turning into an expensive mistake.